Advertisement

- United States

- /

- Electrical

- /

- NasdaqCM:BEEM

Need To Know: Analysts Are Much More Bullish On Beam Global (NASDAQ:BEEM) Revenues

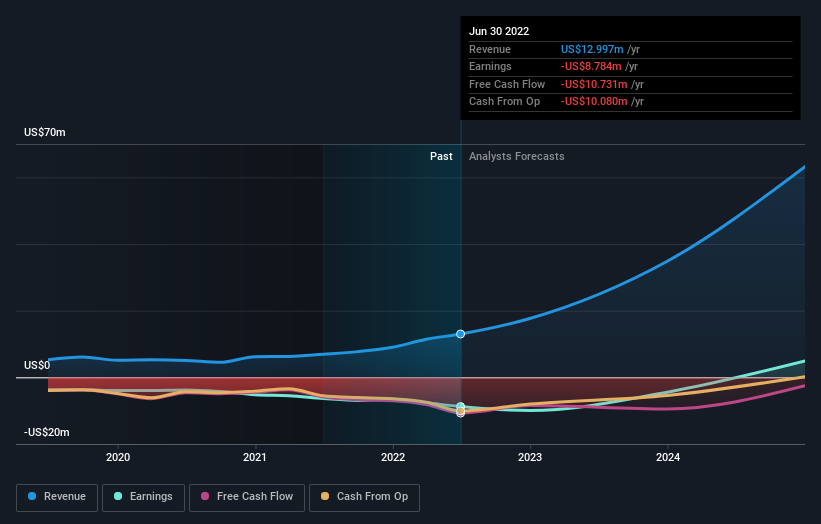

Shareholders in Beam Global (NASDAQ:BEEM) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

Following the upgrade, the most recent consensus for Beam Global from its seven analysts is for revenues of US$18m in 2022 which, if met, would be a sizeable 36% increase on its sales over the past 12 months. Per-share losses are expected to see a sharp uptick, reaching US$1.02. Yet before this consensus update, the analysts had been forecasting revenues of US$16m and losses of US$1.03 per share in 2022. So there's definitely been a change in sentiment in this update, with the analysts upgrading this year's revenue estimates, while at the same time holding losses per share steady.

Our analysis indicates that BEEM is potentially overvalued!

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The analysts are definitely expecting Beam Global's growth to accelerate, with the forecast 84% annualised growth to the end of 2022 ranking favourably alongside historical growth of 26% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 9.9% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Beam Global to grow faster than the wider industry.

The Bottom Line

The most important thing here is that analysts reduced their loss per share estimates for this year, reflecting increased optimism around Beam Global's prospects. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Beam Global.

That's a pretty serious upgrade, but shareholders might be even more pleased to know that forecasts expect Beam Global to be able to reach break-even within the next few years. You can learn more about these forecasts, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Beam Global might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:BEEM

Beam Global

A clean-technology innovation company, engages in the design, development, engineering, manufacture, and sale of renewably energized infrastructure products and battery solutions in the United States and Romania.

Moderate risk with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor