Advertisement

Analysts Just Made A Major Revision To Their Aegion Corporation (NASDAQ:AEGN) Revenue Forecasts

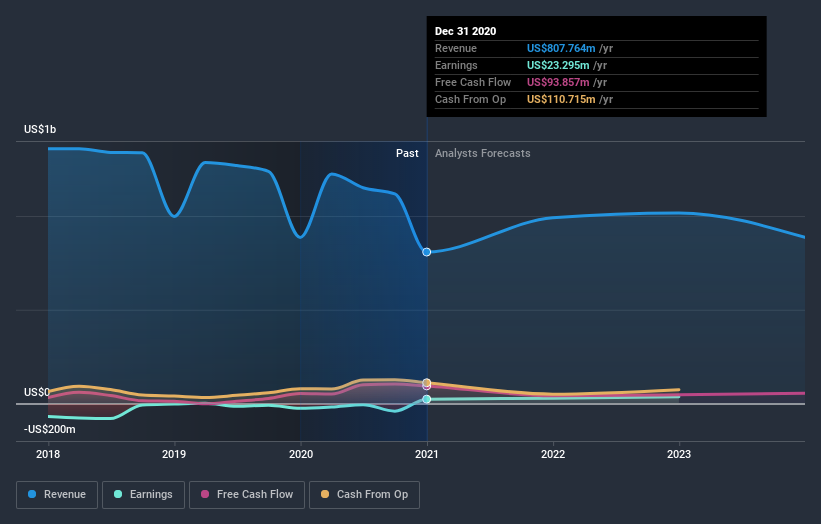

The analysts covering Aegion Corporation (NASDAQ:AEGN) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue estimates were cut sharply as the analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well.

After this downgrade, Aegion's four analysts are now forecasting revenues of US$991m in 2021. This would be a sizeable 23% improvement in sales compared to the last 12 months. Prior to the latest estimates, the analysts were forecasting revenues of US$1.1b in 2021. The consensus view seems to have become more pessimistic on Aegion, noting the measurable cut to revenue estimates in this update.

Check out our latest analysis for Aegion

We'd point out that there was no major changes to their price target of US$26.67, suggesting the latest estimates were not enough to shift their view on the value of the business. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Aegion, with the most bullish analyst valuing it at US$27.00 and the most bearish at US$26.00 per share. This is a very narrow spread of estimates, implying either that Aegion is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Aegion's past performance and to peers in the same industry. For example, we noticed that Aegion's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 23% growth to the end of 2021 on an annualised basis. That is well above its historical decline of 4.8% a year over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 7.3% annually. So it looks like Aegion is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The clear low-light was that analysts slashing their revenue forecasts for Aegion this year. Analysts also expect revenues to grow faster than the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of Aegion going forwards.

Worse, Aegion is labouring under a substantial debt burden, which - if today's forecasts prove accurate - the forecast downgrade could potentially exacerbate. To see more of our financial analysis, you can click through to our free platform to learn more about its balance sheet and specific concerns we've identified.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

If you’re looking to trade Aegion, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor