Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:WAFD

WaFd (WAFD) Valuation in Focus After Full-Year Results and Share Buyback Update

Simply Wall St

Reviewed by Simply Wall St

WaFd (WAFD) just released its results for the fourth quarter and the full year, giving investors an updated look at profitability, earnings, and the company’s ongoing buyback activity as of September 30, 2025.

See our latest analysis for WaFd.

WaFd’s stock has been in the spotlight after releasing its quarterly results and updating on buybacks, but the numbers tell a more nuanced story. While the share price has slipped 7.3% year-to-date and delivered a 1-year total shareholder return of -11.6%, long-term investors have still enjoyed a 56.6% total return over the past five years. This suggests resilience even as momentum has recently faded.

If this latest update has you thinking about where strong upside could be found next, now's a good time to broaden your perspective and discover fast growing stocks with high insider ownership

Against this backdrop of steady earnings and robust buybacks, investors may wonder whether WaFd remains a bargain with more value yet to be unlocked, or if the market has already factored in its future growth prospects for those considering their next move.

Price-to-Earnings of 11x: Is it justified?

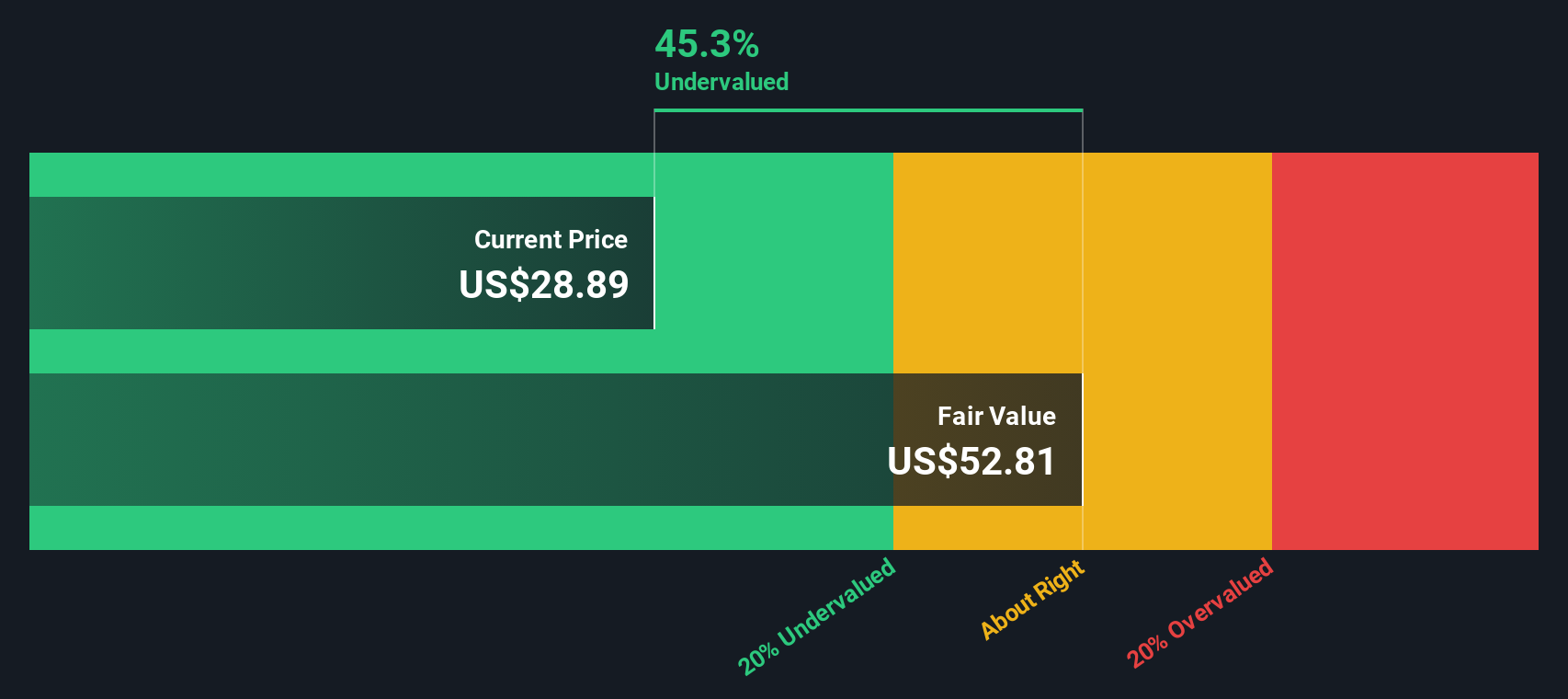

At a recent close of $29.62 per share, WaFd trades at a price-to-earnings multiple of 11x, positioned slightly below the broader US banks industry average and aligned with its peer group. This suggests the stock is currently trading at an attractive valuation relative to both its earnings profile and its sector.

The price-to-earnings (P/E) ratio represents how much investors are willing to pay per dollar of annual earnings. For banks like WaFd, the P/E is often used as a barometer of confidence in profitability, stability, and growth prospects. A lower P/E may indicate a value opportunity, while a higher P/E can suggest robust expectations for future growth.

WaFd’s 11x multiple sits just below the industry average of 11.2x and matches the peer group, hinting that the market does not appear to be overestimating the company’s near-term profit potential. Compared to the estimated fair P/E ratio of 12.2x, WaFd trades at a notable discount. The market could quickly re-rate towards this level if confidence strengthens in its growth story.

Explore the SWS fair ratio for WaFd

Result: Price-to-Earnings of 11x (UNDERVALUED)

However, continued negative short-term returns or unexpected slowdowns in revenue and net income growth could challenge the view that WaFd is undervalued.

Find out about the key risks to this WaFd narrative.

Another View: SWS DCF Model Offers a Higher Estimate

Taking a different approach, our DCF model values WaFd at $43.06 per share, which is 31.2% above the current price. This method focuses on future cash flows rather than earnings alone and suggests an even greater margin of undervaluation. Which signal should investors put more stock in?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out WaFd for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own WaFd Narrative

If you have a different perspective or want to dive deeper into WaFd’s fundamentals, you can easily craft your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding WaFd.

Looking for your next smart investing move?

Don’t wait for opportunities to pass you by. Widen your scope and tap into fresh market trends and under-the-radar potential with the Simply Wall Street Screener today.

- Tap into untapped market potential by checking out these 3554 penny stocks with strong financials, which are capturing attention for strong financials and high growth prospects.

- Capitalize on sector innovation by zeroing in on these 34 healthcare AI stocks, where advanced analytics and medical breakthroughs are reshaping healthcare investing opportunities.

- Boost your portfolio's long-term returns by targeting these 19 dividend stocks with yields > 3% offering above-average yields and consistent payouts for steady income.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WaFd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WAFD

WaFd

Operates as the bank holding company for Washington Federal Bank that provides lending, depository, insurance, and other banking services in the United States.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|6.3% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.8% undervalued

GM

Community Contributor