Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:TCBK

Does TriCo Bancshares' (TCBK) Asset Growth Outpace Profitability Challenges in a Shifting Sector?

Simply Wall St

Reviewed by Sasha Jovanovic

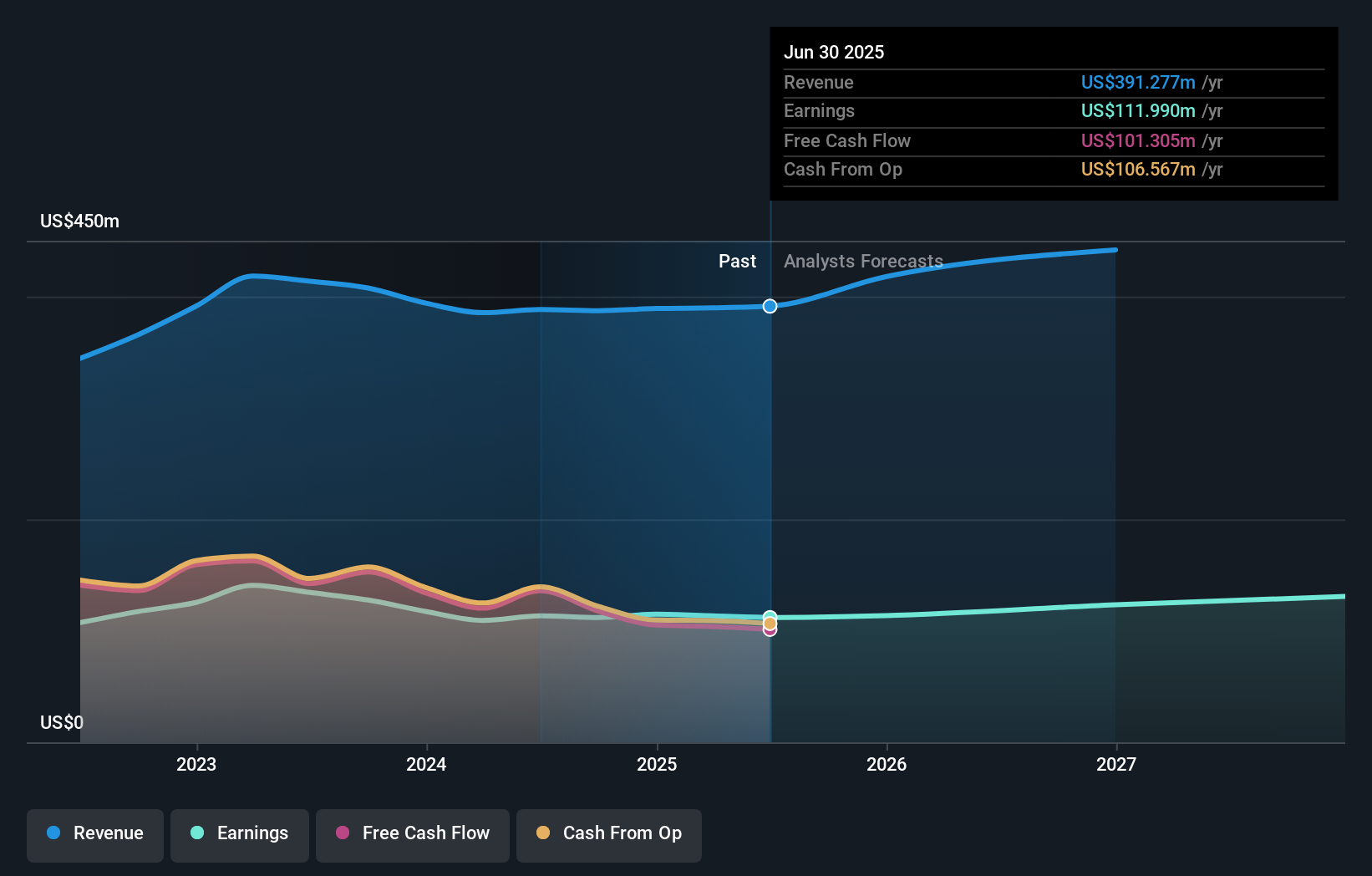

- TriCo Bancshares recently reported that its earnings per share grew at an annualized rate of 11% over the past five years, while tangible book value per share increased by 6.6% annually and 16.2% in the past two years.

- This performance points to improved profitability and a stronger asset base, though net interest income growth has trailed that of the broader banking sector.

- With multi-year growth in profitability and tangible assets, we'll explore how this shapes TriCo Bancshares' investment narrative going forward.

Find companies with promising cash flow potential yet trading below their fair value.

What Is TriCo Bancshares' Investment Narrative?

For anyone considering TriCo Bancshares, the big picture centers on steady long-term growth in profitability, book value and dividends, with evidence of management's confidence in the company's trajectory. The recent news, highlighting multi-year compounded growth in earnings per share and tangible book value, adds weight to an already solid track record. However, recent financials suggest that earnings and net interest income growth remain below broader sector trends, highlighting some short-term pressure on core revenue streams. While the 9% dividend hike signals continued strength, these results may prompt investors to reassess short-term catalysts like loan demand and margin expansion versus headline book value growth. Crucially, any change in risks or drivers from this update appears contained at this point, based on muted stock price moves and the ongoing share buyback and dividend story.

But remember, charge-offs and slow net income growth remain information investors should watch. TriCo Bancshares' shares have been on the rise but are still potentially undervalued by 37%. Find out what it's worth.Exploring Other Perspectives

Explore 2 other fair value estimates on TriCo Bancshares - why the stock might be worth as much as 10% more than the current price!

Build Your Own TriCo Bancshares Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your TriCo Bancshares research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free TriCo Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TriCo Bancshares' overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 35 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TriCo Bancshares might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TCBK

TriCo Bancshares

Operates as a bank holding company for Tri Counties Bank that provides commercial banking services to individual and corporate customers.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor