Bancorp (TBBK) shares have climbed over the past week, gaining 5% even though its revenue growth last year dipped slightly. Investors seem interested in how the bank’s improved net income could impact valuation in the future.

Bancorp’s rally this year has been impressive, with the latest 7-day share price return of 5.4% adding to year-to-date gains of over 46%. The momentum is supported by a 1-year total shareholder return of 37.5% and a remarkable 741% total return over five years, signaling that investors are increasingly optimistic about the bank’s ability to grow earnings over the long term.

With shares surging and a solid track record of returns, the pressing question is whether Bancorp is still undervalued or if the market has already fully priced in all its future growth potential, which could leave little room for upside.

Advertisement

Price-to-Earnings of 15.5x: Is it justified?

Bancorp currently trades at a price-to-earnings (P/E) ratio of 15.5, noticeably higher than both its peer average of 12.5 and the US Banks industry average of 11.3. The last close price of $75.58 suggests that investors might be paying a premium for growth or quality.

The P/E ratio measures how much investors are willing to pay per dollar of earnings. For banks, this multiple is a key signal of expected profitability, growth, and risk appetite in the sector. An elevated P/E can reflect confidence in future earnings expansion or a perceived competitive advantage.

However, Bancorp’s premium valuation stands out because it surpasses industry benchmarks and also edges above the estimated fair P/E ratio of 15x. This indicates that enthusiasm for the stock’s outlook is running stronger than sector expectations, but there is a chance for the market to re-align if growth does not continue to impress.

However, ongoing revenue declines and a limited discount to analyst price targets could challenge continued optimism if profitability growth slows or if expectations shift.

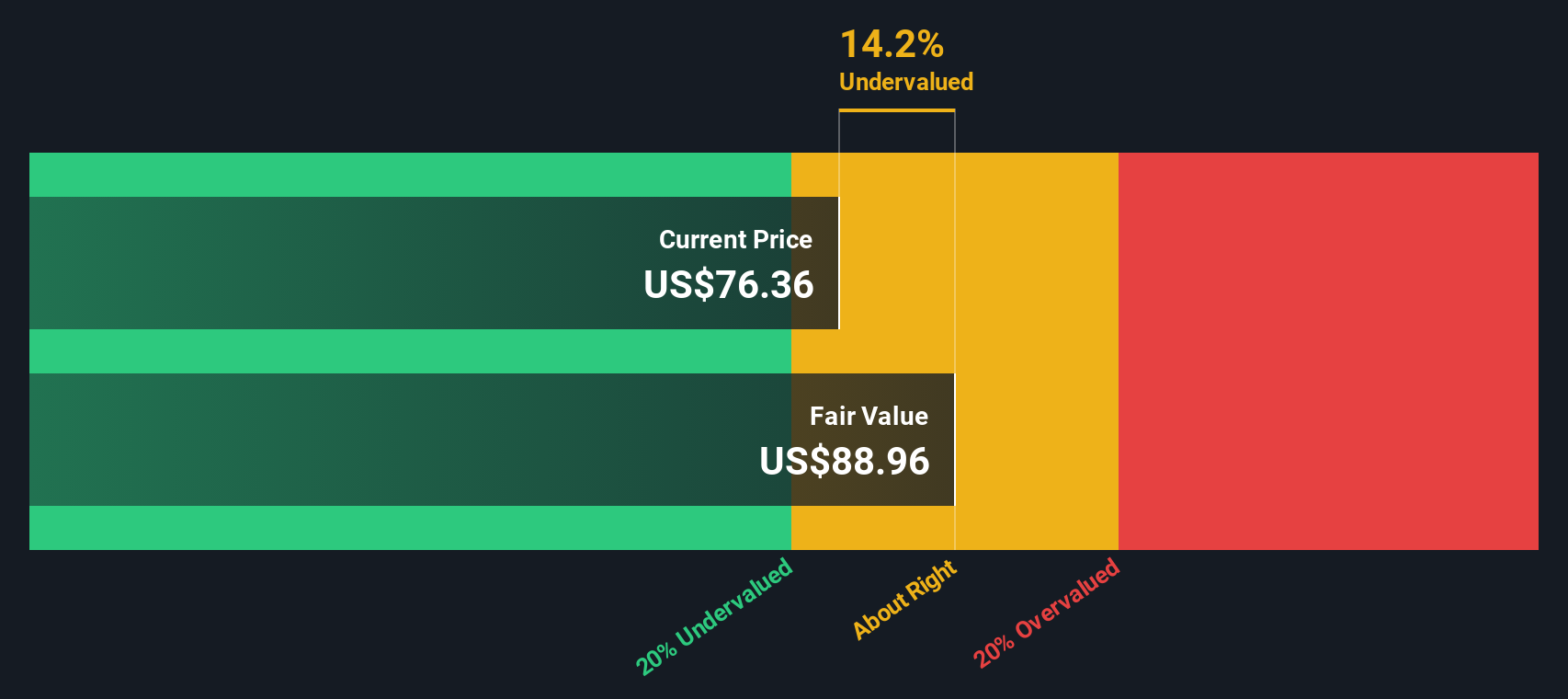

Looking at Bancorp through the lens of our DCF model paints a different picture. While the market has priced the stock as expensive using its P/E ratio, the SWS DCF model estimates fair value at $88.96, about 15% above the current share price. Could the market be overlooking long-term value here?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bancorp for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bancorp Narrative

If you see the story differently or want to investigate the numbers for yourself, you can easily build your own narrative in just a few minutes with Do it your way.

Take the lead on tomorrow’s market movers by putting the power of the Simply Wall Street Screener to work. These opportunities are far too good to pass up.

Tap opportunities in digital finance by scanning these 80 cryptocurrency and blockchain stocks that are changing the game with secure blockchain solutions and innovative payment platforms.

Jump into the next wave of technology by reviewing these 27 AI penny stocks that are transforming industries with real-world applications in automation and intelligent systems.

Lock in potential long-term wealth by reviewing these 17 dividend stocks with yields > 3% offering attractive yields for investors seeking reliable income streams and strong fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bancorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.