Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:PFBC

How Rate Cut Hopes Have Shifted the Investment Narrative for Preferred Bank (PFBC)

Simply Wall St

Reviewed by Sasha Jovanovic

- Shares of Preferred Bank saw a noticeable lift after comments from New York Federal Reserve President John Williams about potential interest rate cuts raised the perceived likelihood of monetary policy easing.

- This shift in outlook provided a boost for regional banks like Preferred Bank, which have been under pressure from high interest rates and concerns related to commercial real estate exposure.

- With interest rate expectations shifting, we'll examine how improved sentiment for regional banks may influence Preferred Bank's investment narrative.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Preferred Bank Investment Narrative Recap

To be a shareholder in Preferred Bank, you have to believe that the bank’s disciplined cost controls and targeted expansion in growth markets can deliver sustainable returns, despite credit cycle risks linked to commercial real estate and its regional loan book. The recent shift in interest rate expectations has improved sentiment, and while it may ease some funding pressures in the short term, it does not fundamentally change the ongoing risk of loan quality shocks tied to the bank's concentrated exposure in California and real estate.

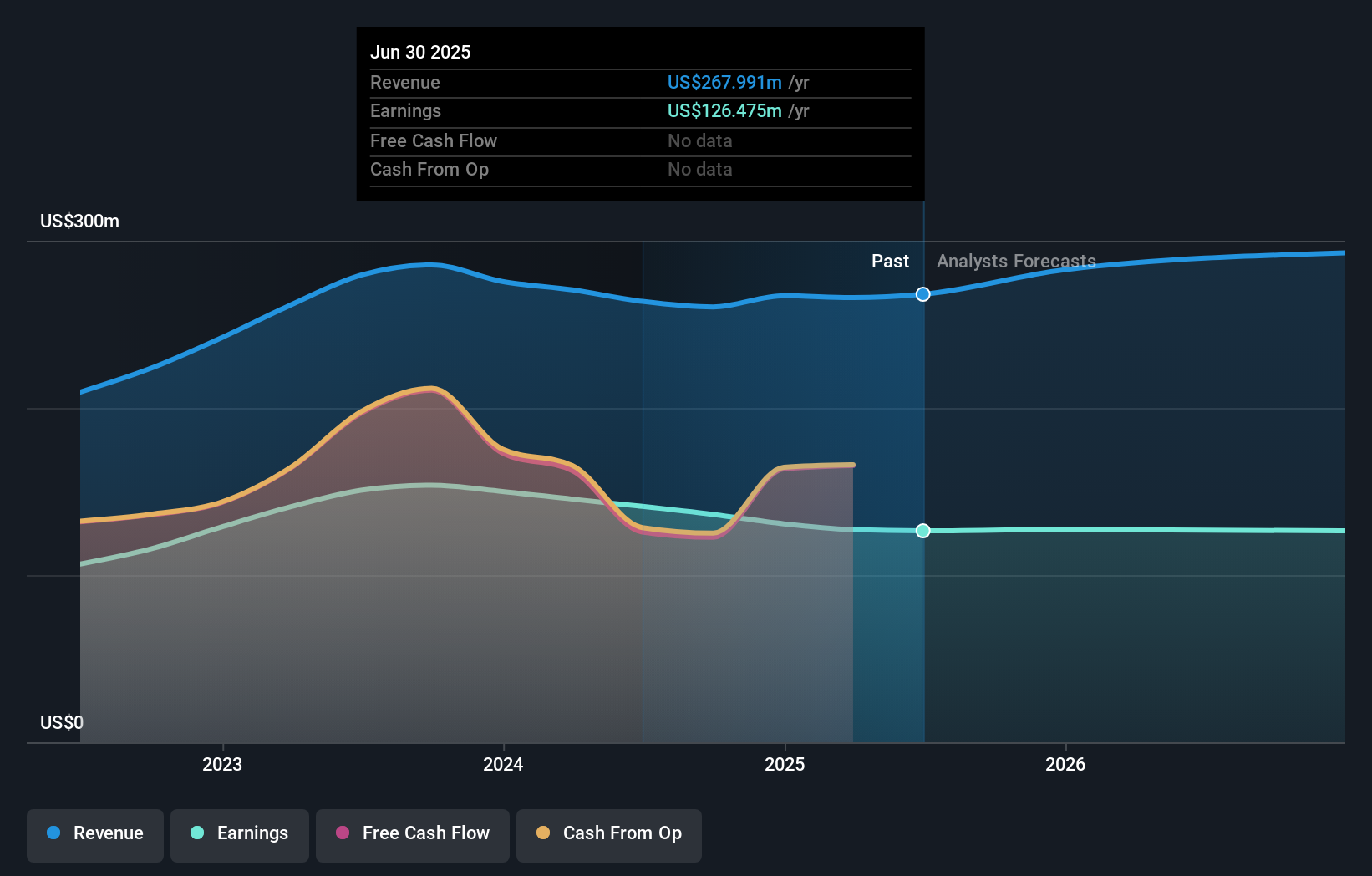

Against the backdrop of interest rate optimism, Preferred Bank’s third-quarter earnings show net interest income of US$71.31 million and basic EPS of US$2.90, an annual increase. This financial resilience ties directly to a key catalyst: the potential benefit from economic recovery and steady loan demand in its core client segments, especially if lower rates spark further lending activity and help offset rising credit costs.

Yet, should local economic or sector-specific stress emerge, especially in California commercial real estate, investors should pay close attention to...

Read the full narrative on Preferred Bank (it's free!)

Preferred Bank's narrative projects $320.4 million revenue and $126.6 million earnings by 2028. This requires 6.1% yearly revenue growth and virtually no change in earnings (an increase of just $0.1 million) from current earnings of $126.5 million.

Uncover how Preferred Bank's forecasts yield a $107.00 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members’ fair value estimates for Preferred Bank span from US$107 to US$244, with just two submissions. Many expect ongoing loan and deposit concentration risks to shape future outcomes, showing how opinions on the outlook for asset quality and growth can differ significantly. Discover several viewpoints on what drives share price potential.

Explore 2 other fair value estimates on Preferred Bank - why the stock might be worth just $107.00!

Build Your Own Preferred Bank Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Preferred Bank research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Preferred Bank research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Preferred Bank's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PFBC

Preferred Bank

Provides various banking products and services to small and mid-sized businesses, entrepreneurs, real estate developers, professionals, and high net worth individuals.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor