Advertisement

- United States

- /

- Auto

- /

- NYSE:HOG

Harley-Davidson (HOG) Is Down 5.2% After Q3 Earnings Surge and 2026 Model Reveal—Has the Bull Case Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Harley-Davidson reported third-quarter net income of US$377.37 million, up from US$119.04 million a year earlier, alongside the reveal of select 2026 motorcycle models and updates on its ongoing share buyback program.

- This combination of stronger-than-expected earnings, expanded product offerings, and continued capital returns highlights Harley-Davidson’s focus on both financial performance and long-term brand evolution.

- Now, we’ll explore how Harley-Davidson’s robust third-quarter earnings performance could reshape its investment narrative going forward.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Harley-Davidson Investment Narrative Recap

For shareholders, Harley-Davidson demands belief in the company's ability to drive earnings growth and reinvigorate its brand, even as motorcycle retail sales face ongoing pressure from macroeconomic headwinds. Although the latest financial results provide a short-term boost, they do not meaningfully reduce the risk that weak consumer demand and volatile tariffs could hinder near-term revenue growth, the most important catalyst and risk remain unchanged for now.

Among recent developments, the expansion of Harley-Davidson’s 2026 model lineup directly supports the push for new customer segments, a key catalyst given the company’s plans to introduce lower-priced, more accessible models designed to offset potential demand softness and an aging customer base.

By contrast, investors should be aware of the persistent risk that ongoing economic uncertainty and high interest rates could...

Read the full narrative on Harley-Davidson (it's free!)

Harley-Davidson's outlook anticipates $3.9 billion in revenue and $390.5 million in earnings by 2028. This reflects a 4.4% annual revenue decline and a $147.7 million increase in earnings from the current $242.8 million.

Uncover how Harley-Davidson's forecasts yield a $29.33 fair value, a 15% upside to its current price.

Exploring Other Perspectives

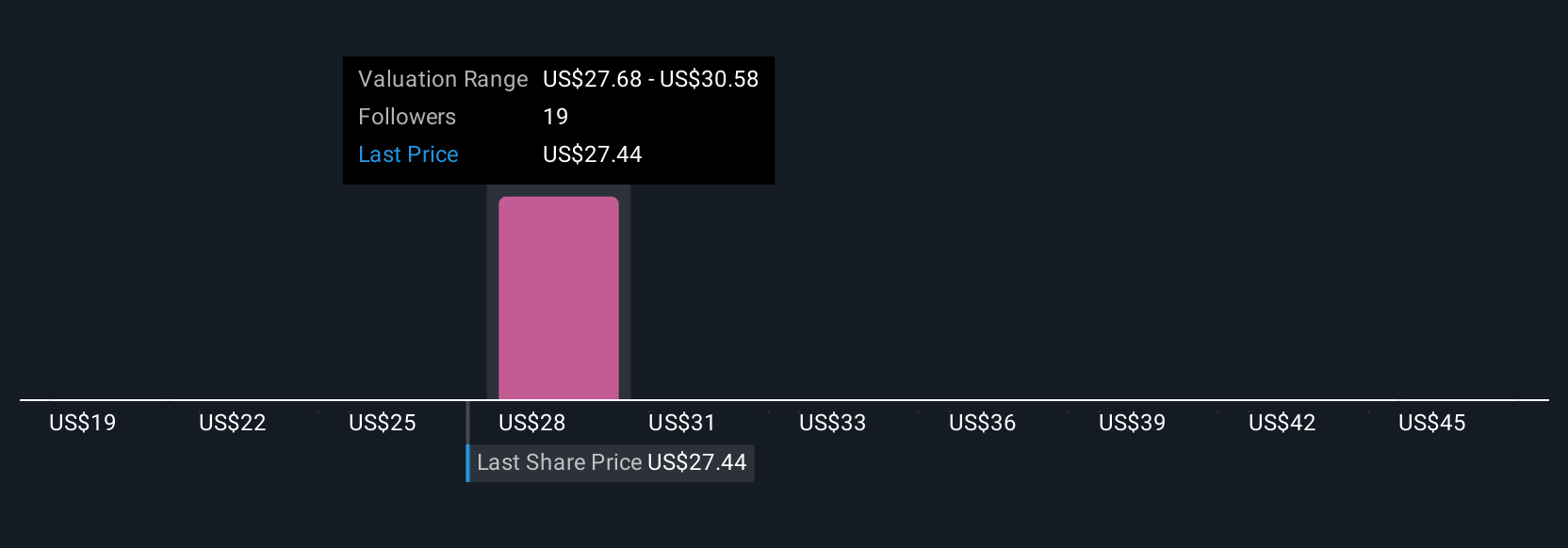

Four members of the Simply Wall St Community estimate Harley-Davidson’s fair value between US$19 and US$47.94 per share, revealing a wide range of expectations. With ongoing pressure from sluggish global sales and changing consumer demand, your own outlook on the company’s prospects could differ sharply from others, explore several perspectives before making any conclusions.

Explore 4 other fair value estimates on Harley-Davidson - why the stock might be worth as much as 87% more than the current price!

Build Your Own Harley-Davidson Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Harley-Davidson research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Harley-Davidson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Harley-Davidson's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Harley-Davidson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HOG

Harley-Davidson

Manufactures and sells motorcycles in the United States and internationally.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor