- United States

- /

- Auto Components

- /

- NasdaqGS:GT

Is There Now an Opportunity in Goodyear After Recent Strategic Reshuffling?

Reviewed by Bailey Pemberton

If you’re wondering what to make of Goodyear Tire & Rubber stock right now, you’re not alone. With shares closing at $7.04 and posting a 4.9% gain over the last week, some investors are hoping for a turnaround. But step back just a bit and the picture gets more complicated. Goodyear’s 1-year return sits at -15.3%, and over 3 years, the stock has dropped by 40.9%. Clearly, long-term holders have had to endure some bumpy roads.

There’s been a steady flow of headlines for Goodyear lately, ranging from shifting demand in the electric vehicle sector to strategic reshuffling in its core business. Earlier consolidation news and ongoing cost structure reviews have sparked some optimism that Goodyear could be repositioning for a sturdier recovery. It’s these kinds of moves that, while not yet fully reflected in the price, tend to change how investors perceive risk and reward, even before fundamentals shift.

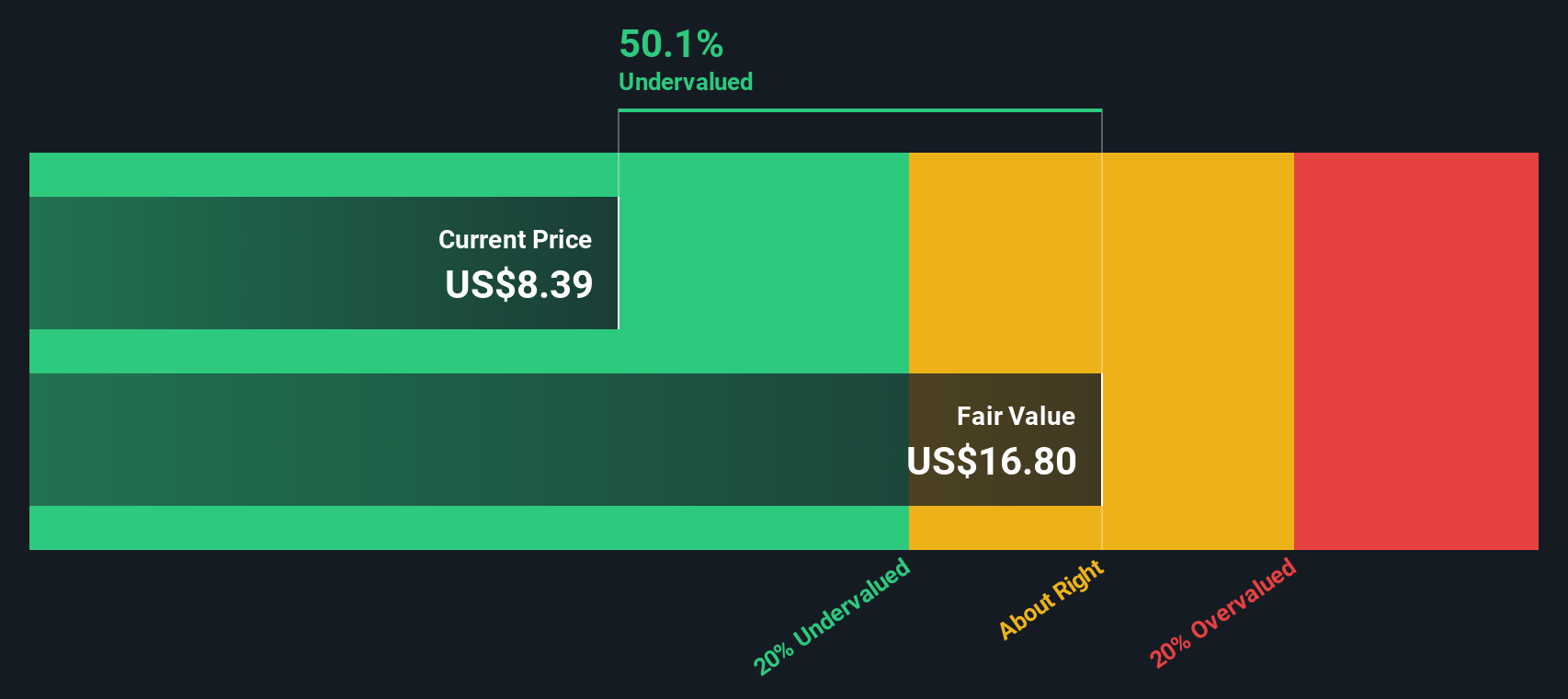

So where does Goodyear stand on valuation? By tallying up the numbers using several well-known valuation checks, the stock currently scores a 5 out of 6, meaning it looks undervalued on nearly every metric that matters. But as always, a simple checklist can only take you so far. Let’s dig into the actual methods behind these checks and, even more importantly, explore the smarter way to think about value for a company like Goodyear.

Why Goodyear Tire & Rubber is lagging behind its peers

Approach 1: Goodyear Tire & Rubber Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and then discounting them back to today’s dollars. This approach helps investors see what a business could be worth, based on realistic expectations for how much cash it will bring in year after year.

For Goodyear Tire & Rubber, the most recent reported Free Cash Flow (FCF) stands at a negative $533 million. However, analyst projections signal a turnaround over the next five years, with estimates for annual FCF moving into positive territory and reaching $540 million by 2029. Looking further out, Simply Wall St models extrapolate growth into the next decade, with FCF expected to climb gradually towards $750 million by 2035.

Crunching these numbers using a 2 Stage Free Cash Flow to Equity approach, the DCF model places Goodyear’s fair value at $19.12 per share. This figure is 63.2 percent higher than today’s share price of $7.04, indicating a significant margin of undervaluation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Goodyear Tire & Rubber is undervalued by 63.2%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

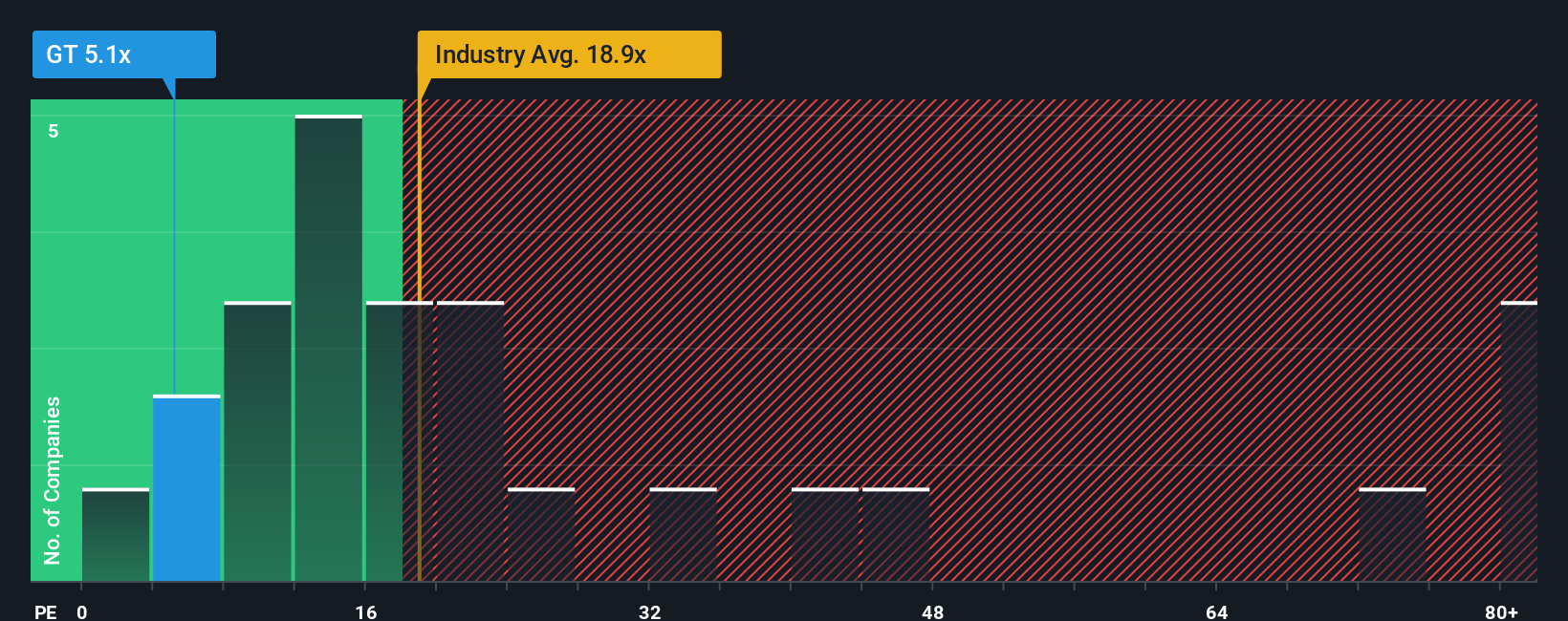

Approach 2: Goodyear Tire & Rubber Price vs Earnings

The Price-to-Earnings (PE) ratio is widely used when valuing established and profitable companies because it quickly tells investors how much they are paying for each dollar of a company’s earnings. For companies like Goodyear Tire & Rubber that are generating consistent profits, the PE ratio can reveal if the stock price reflects reasonable growth and risk expectations compared to its underlying earnings power.

It’s important to note that what counts as a "normal" or "fair" PE ratio varies depending on several factors. Investors generally expect a higher PE for companies with strong growth prospects and lower business risk. On the flip side, slower growers or riskier companies deserve a lower multiple.

Goodyear currently trades at a PE ratio of just 4.7x. That stands in stark contrast to the average PE for the Auto Components industry, which is 18.4x, and its peer group, which averages an even higher 33.7x. At first glance, this makes Goodyear appear deeply undervalued. However, using Simply Wall St’s "Fair Ratio," which factors in the company’s growth, risk profile, profit margins, industry dynamics, and market cap, delivers even more context. Goodyear’s Fair Ratio is 11.3x, offering a more tailored view than broad peer or industry comparisons. By accounting for what actually sets Goodyear apart, this proprietary benchmark filters out noise and hones in on how the market should reasonably value the stock right now.

With Goodyear’s actual PE ratio significantly below its Fair Ratio, this second valuation check also signals that the stock is undervalued by earnings standards.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Goodyear Tire & Rubber Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is simply your story for where a company like Goodyear is headed, linking your perspective about the business to concrete forecasts about its revenue, profits, and margins, and using those numbers to estimate a fair value.

Instead of relying solely on ratios like PE, Narratives help you connect the dots between what you believe will happen and what those beliefs mean for the company’s underlying worth. Think of Narratives as an easy, guided tool you can use anytime on Simply Wall St’s Community page, trusted by millions of investors looking to make smarter, more dynamic decisions.

With a Narrative, you can track your assumptions alongside others, review financial forecasts, and instantly see if your view of Goodyear’s fair value suggests it’s time to buy, hold, or sell, compared to the current share price.

The best part is Narratives automatically update when new events, earnings, or news hit the market, letting you react and rethink your thesis as new facts emerge.

For Goodyear Tire & Rubber, one Narrative might see the company as a long-term turnaround play, forecasting $15 as a fair value based on successful premium tire growth and cost savings, while another might view persistent competition as a drag, supporting a fair value closer to $9. Both are backed by each investor’s story and numbers.

Do you think there's more to the story for Goodyear Tire & Rubber? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:GT

Goodyear Tire & Rubber

Develops, manufactures, distributes, and sells tires and related products and services worldwide.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion