Advertisement

- Taiwan

- /

- Renewable Energy

- /

- TWSE:6873

Some Investors May Be Worried About HD Renewable Energy's (TWSE:6873) Returns On Capital

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. In light of that, when we looked at HD Renewable Energy (TWSE:6873) and its ROCE trend, we weren't exactly thrilled.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on HD Renewable Energy is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.13 = NT$1.4b ÷ (NT$16b - NT$5.4b) (Based on the trailing twelve months to September 2024).

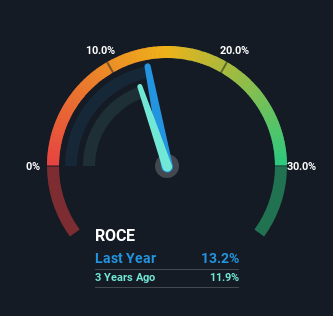

Thus, HD Renewable Energy has an ROCE of 13%. In absolute terms, that's a satisfactory return, but compared to the Renewable Energy industry average of 3.1% it's much better.

Check out our latest analysis for HD Renewable Energy

Above you can see how the current ROCE for HD Renewable Energy compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering HD Renewable Energy for free.

The Trend Of ROCE

The trend of ROCE doesn't look fantastic because it's fallen from 29% five years ago, while the business's capital employed increased by 1,839%. Usually this isn't ideal, but given HD Renewable Energy conducted a capital raising before their most recent earnings announcement, that would've likely contributed, at least partially, to the increased capital employed figure. HD Renewable Energy probably hasn't received a full year of earnings yet from the new funds it raised, so these figures should be taken with a grain of salt.

The Key Takeaway

In summary, despite lower returns in the short term, we're encouraged to see that HD Renewable Energy is reinvesting for growth and has higher sales as a result. And the stock has done incredibly well with a 171% return over the last three years, so long term investors are no doubt ecstatic with that result. So while investors seem to be recognizing these promising trends, we would look further into this stock to make sure the other metrics justify the positive view.

HD Renewable Energy does come with some risks though, we found 4 warning signs in our investment analysis, and 1 of those makes us a bit uncomfortable...

While HD Renewable Energy may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if HD Renewable Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:6873

HD Renewable Energy

Engages in the development of solar power generation systems, engineering construction, and maintenances in Taiwan.

Very undervalued with high growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor