Advertisement

- Taiwan

- /

- Renewable Energy

- /

- TWSE:6873

HD Renewable Energy Co., Ltd. (TWSE:6873) Looks Just Right With A 52% Price Jump

HD Renewable Energy Co., Ltd. (TWSE:6873) shares have had a really impressive month, gaining 52% after a shaky period beforehand. The last month tops off a massive increase of 132% in the last year.

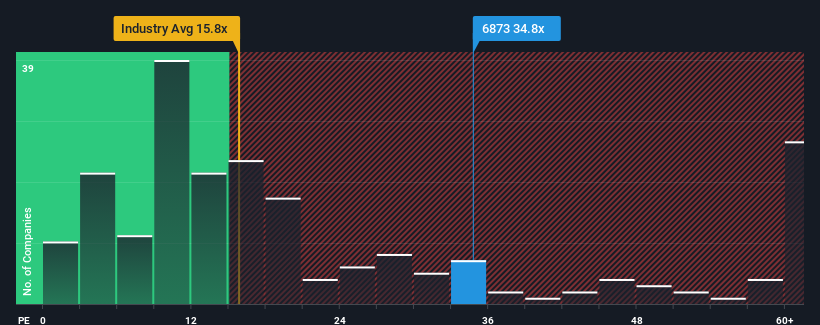

After such a large jump in price, given around half the companies in Taiwan have price-to-earnings ratios (or "P/E's") below 23x, you may consider HD Renewable Energy as a stock to potentially avoid with its 34.8x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

With its earnings growth in positive territory compared to the declining earnings of most other companies, HD Renewable Energy has been doing quite well of late. It seems that many are expecting the company to continue defying the broader market adversity, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for HD Renewable Energy

Does Growth Match The High P/E?

In order to justify its P/E ratio, HD Renewable Energy would need to produce impressive growth in excess of the market.

Taking a look back first, we see that there was hardly any earnings per share growth to speak of for the company over the past year. Although pleasingly EPS has lifted 71% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the two analysts covering the company suggest earnings should grow by 70% over the next year. Meanwhile, the rest of the market is forecast to only expand by 24%, which is noticeably less attractive.

In light of this, it's understandable that HD Renewable Energy's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From HD Renewable Energy's P/E?

The large bounce in HD Renewable Energy's shares has lifted the company's P/E to a fairly high level. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of HD Renewable Energy's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

We don't want to rain on the parade too much, but we did also find 2 warning signs for HD Renewable Energy (1 can't be ignored!) that you need to be mindful of.

Of course, you might also be able to find a better stock than HD Renewable Energy. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if HD Renewable Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6873

HD Renewable Energy

Engages in the development of solar power generation systems, engineering construction, and maintenances in Taiwan.

Very undervalued with high growth potential.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor