- Taiwan

- /

- Wireless Telecom

- /

- TWSE:4904

We Think Far EasTone Telecommunications (TPE:4904) Is Taking Some Risk With Its Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Far EasTone Telecommunications Co., Ltd. (TPE:4904) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Far EasTone Telecommunications

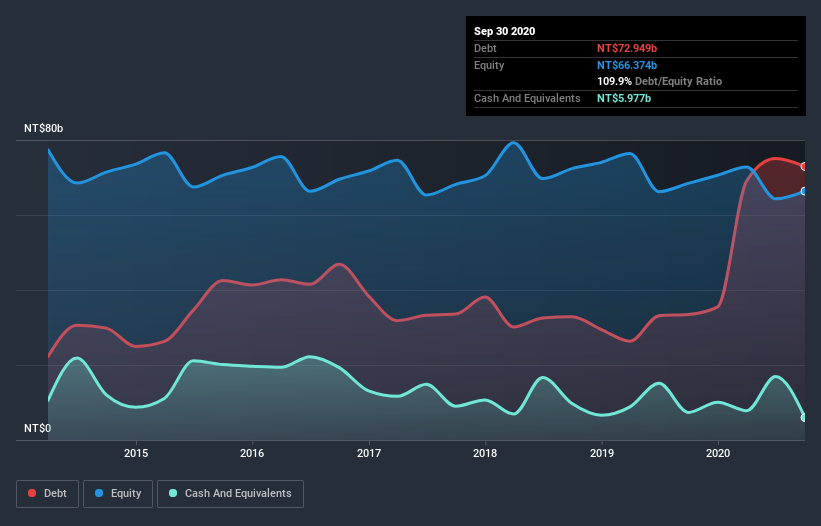

What Is Far EasTone Telecommunications's Debt?

The image below, which you can click on for greater detail, shows that at September 2020 Far EasTone Telecommunications had debt of NT$72.9b, up from NT$33.5b in one year. However, it does have NT$5.98b in cash offsetting this, leading to net debt of about NT$67.0b.

How Healthy Is Far EasTone Telecommunications' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Far EasTone Telecommunications had liabilities of NT$34.1b due within 12 months and liabilities of NT$68.8b due beyond that. On the other hand, it had cash of NT$5.98b and NT$12.2b worth of receivables due within a year. So it has liabilities totalling NT$84.7b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Far EasTone Telecommunications is worth NT$195.5b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Far EasTone Telecommunications's net debt is 2.9 times its EBITDA, which is a significant but still reasonable amount of leverage. However, its interest coverage of 21.5 is very high, suggesting that the interest expense on the debt is currently quite low. Notably Far EasTone Telecommunications's EBIT was pretty flat over the last year. We would prefer to see some earnings growth, because that always helps diminish debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Far EasTone Telecommunications can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Considering the last three years, Far EasTone Telecommunications actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

Neither Far EasTone Telecommunications's ability to convert EBIT to free cash flow nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But its interest cover tells a very different story, and suggests some resilience. Taking the abovementioned factors together we do think Far EasTone Telecommunications's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example Far EasTone Telecommunications has 4 warning signs (and 3 which are significant) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

When trading Far EasTone Telecommunications or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:4904

Far EasTone Telecommunications

Engages in the provision of telecommunications and digital application services in Taiwan.

Fair value with acceptable track record.