Advertisement

- Taiwan

- /

- Tech Hardware

- /

- TWSE:2365

KYE Systems' (TWSE:2365) Solid Profits Have Weak Fundamentals

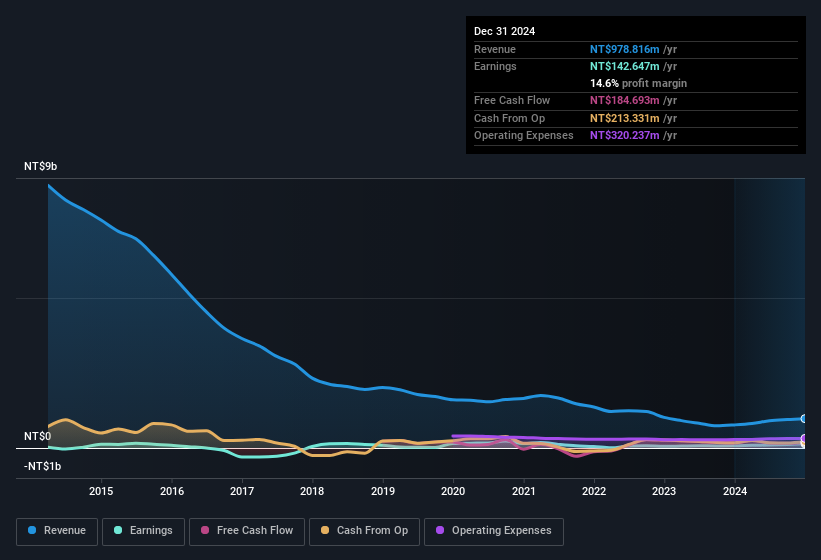

Investors were disappointed with KYE Systems Corp.'s (TWSE:2365) earnings, despite the strong profit numbers. We think that the market might be paying attention to some underlying factors that they find to be concerning.

How Do Unusual Items Influence Profit?

Importantly, our data indicates that KYE Systems' profit received a boost of NT$26m in unusual items, over the last year. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. Which is hardly surprising, given the name. We can see that KYE Systems' positive unusual items were quite significant relative to its profit in the year to December 2024. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of KYE Systems.

Our Take On KYE Systems' Profit Performance

As previously mentioned, KYE Systems' large boost from unusual items won't be there indefinitely, so its statutory earnings are probably a poor guide to its underlying profitability. For this reason, we think that KYE Systems' statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. But the good news is that its EPS growth over the last three years has been very impressive. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. For example - KYE Systems has 1 warning sign we think you should be aware of.

This note has only looked at a single factor that sheds light on the nature of KYE Systems' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Valuation is complex, but we're here to simplify it.

Discover if KYE Systems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2365

KYE Systems

Engages in the manufacturing, processing, and sale of computer peripheral products for business, lifestyle, mobility, and gaming peripherals in Taiwan and internationally.

Flawless balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Vulcan Minerals ·

Uncovering The Hidden Annuity: Why Vulcan Minerals (TSXV:VUL) Trades At A Massive Discount To Its Sum-Of-The-Parts

Fair Value:CA$2.2378.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Rog on CTT - Correios De Portugal ·

Why CTT benefits in multiple ways right now

Fair Value:€7.6721.6% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Adecoagro ·

Why a "2026 Super El Nino" is the Ultimate Hedge for Tech-Heavy Portfolios

Fair Value:US$18.2849.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

60 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative