Advertisement

As global markets navigate a landscape of economic uncertainty and mixed outlooks, Asian markets are capturing attention with their unique growth dynamics. In this environment, companies with high insider ownership often signal strong internal confidence and alignment with shareholder interests, making them compelling considerations for investors seeking growth opportunities in Asia.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.3% | 26% |

| WinWay Technology (TWSE:6515) | 22.2% | 21.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 47.2% |

| Global Tax Free (KOSDAQ:A204620) | 21.8% | 89.3% |

| Oscotec (KOSDAQ:A039200) | 21.3% | 131.6% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 125.9% |

| Fulin Precision (SZSE:300432) | 13.6% | 78.6% |

| Ascentage Pharma Group International (SEHK:6855) | 17.9% | 60.9% |

| Synspective (TSE:290A) | 13.2% | 37.4% |

We're going to check out a few of the best picks from our screener tool.

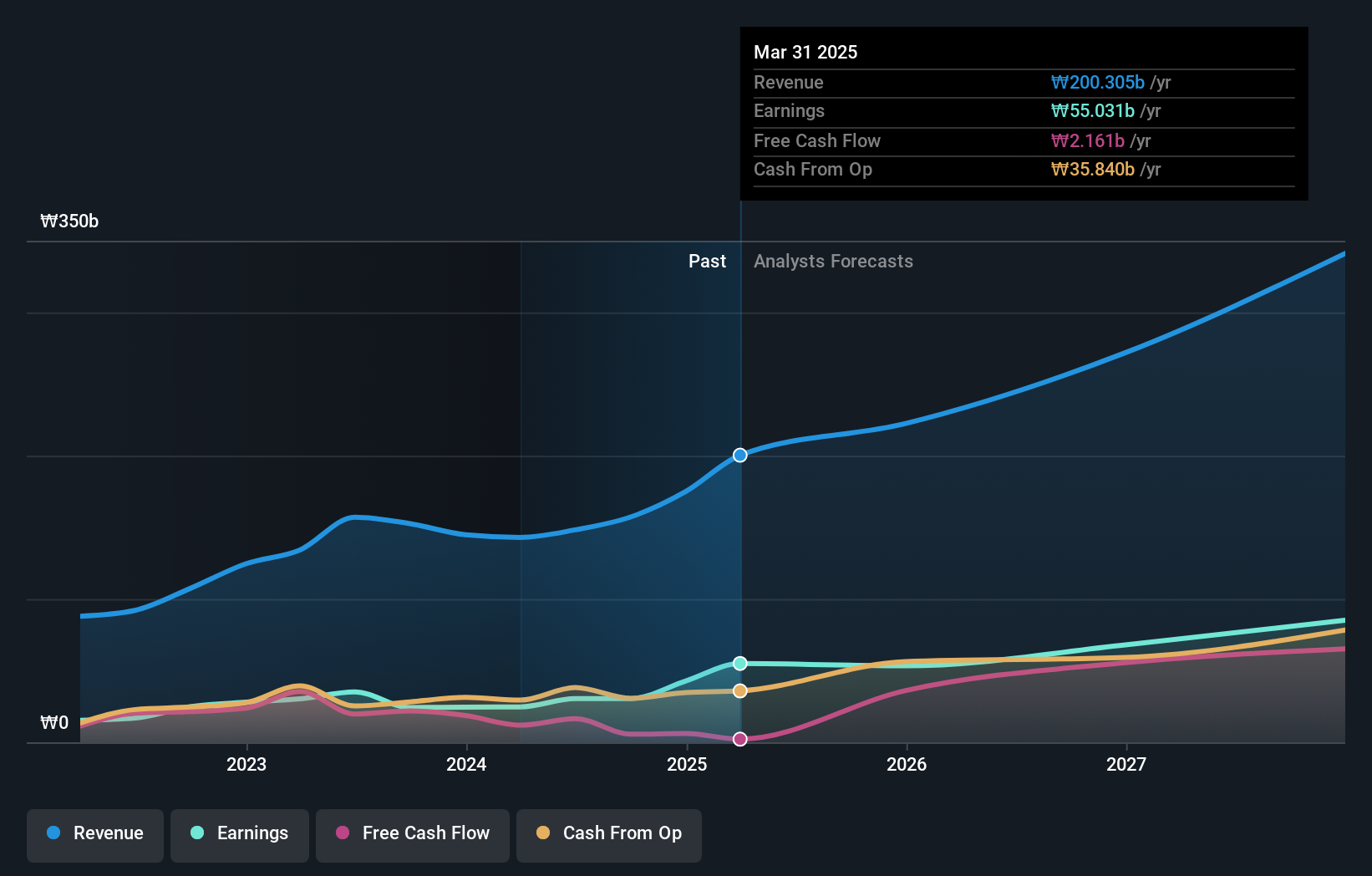

Park Systems (KOSDAQ:A140860)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Park Systems Corp. develops, manufactures, and sells atomic force microscopy (AFM) systems worldwide, with a market cap of ₩1.42 trillion.

Operations: The company's revenue primarily comes from its Scientific & Technical Instruments segment, generating ₩157.20 billion.

Insider Ownership: 33.1%

Earnings Growth Forecast: 34.2% p.a.

Park Systems demonstrates strong growth potential with earnings forecasted to increase significantly at 34.21% annually, outpacing the South Korean market's average. Despite trading slightly below fair value estimates, analysts expect a price rise of 31.8%. Revenue is also projected to grow faster than the market at 17.4% per year. High-quality earnings and a robust return on equity forecast further bolster its investment appeal, though recent insider trading activity is not available for review.

- Navigate through the intricacies of Park Systems with our comprehensive analyst estimates report here.

- Upon reviewing our latest valuation report, Park Systems' share price might be too optimistic.

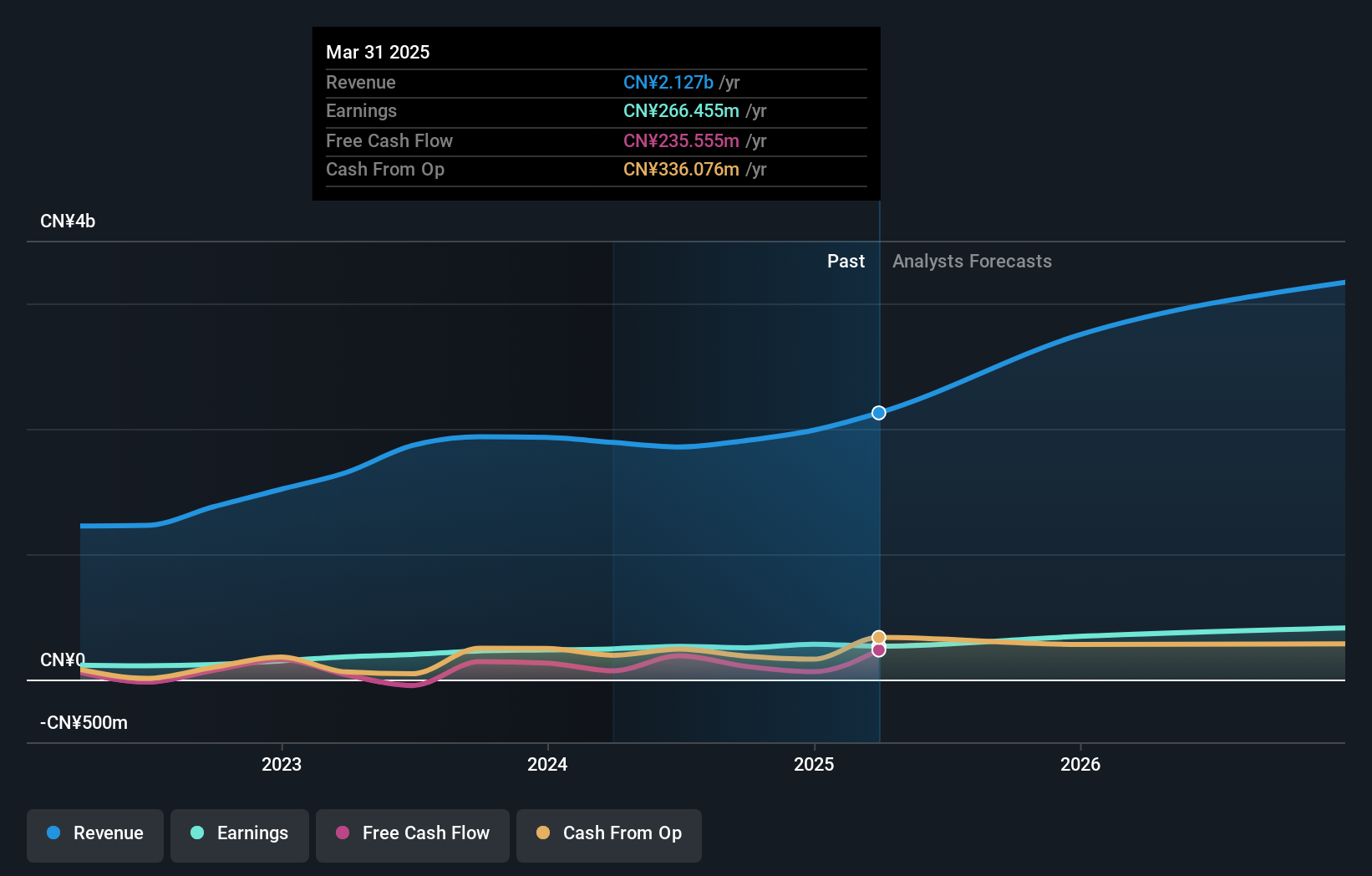

Asian Star Anchor Chain Jiangsu (SHSE:601890)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Asian Star Anchor Chain Co., Ltd. Jiangsu, along with its subsidiaries, specializes in the global production and sale of anchor chains, marine mooring chains, and related accessories, with a market cap of CN¥9.86 billion.

Operations: Asian Star Anchor Chain Jiangsu generates revenue primarily from the manufacturing and sale of anchor chains, marine mooring chains, and related accessories on a global scale.

Insider Ownership: 37.6%

Earnings Growth Forecast: 21.4% p.a.

Asian Star Anchor Chain Jiangsu is poised for substantial growth, with revenue expected to rise by 20.9% annually, surpassing the CN market average. Despite a lower forecasted return on equity of 9.8%, earnings are projected to grow significantly at 21.45% per year, albeit slightly below the broader market's pace. The stock trades at a price-to-earnings ratio of 37.9x, just under the market average, while its dividend yield of 1.05% lacks robust coverage from free cash flows.

- Click here and access our complete growth analysis report to understand the dynamics of Asian Star Anchor Chain Jiangsu.

- Our expertly prepared valuation report Asian Star Anchor Chain Jiangsu implies its share price may be too high.

Chroma ATE (TWSE:2360)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chroma ATE Inc. is involved in the design, assembly, manufacturing, sale, repair, and maintenance of software/hardware for computers and peripherals as well as various electronic testing systems and power supplies across Taiwan, China, the United States, and internationally; it has a market cap of NT$133.03 billion.

Operations: The company's revenue is primarily derived from its Measuring Instruments Business, which accounts for NT$33.42 billion, and Automated Transport Engineering, contributing NT$1.45 billion.

Insider Ownership: 14.5%

Earnings Growth Forecast: 20.1% p.a.

Chroma ATE demonstrates robust growth potential, with earnings forecasted to grow at 20.1% annually, outpacing the Taiwanese market average. Recent inclusion in the FTSE All-World Index highlights its growing prominence. The company reported a significant increase in net income for 2024, reaching TWD 5.26 billion from TWD 3.98 billion previously. Despite trading below fair value estimates and expected price appreciation of 43%, its dividend yield of 2.85% is not well-supported by free cash flows.

- Take a closer look at Chroma ATE's potential here in our earnings growth report.

- Our comprehensive valuation report raises the possibility that Chroma ATE is priced lower than what may be justified by its financials.

Key Takeaways

- Investigate our full lineup of 648 Fast Growing Asian Companies With High Insider Ownership right here.

- Curious About Other Options? The end of cancer? These 21 emerging AI stocks are developing tech that will allow early idenification of life changing disesaes like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:601890

Asian Star Anchor Chain Jiangsu

Engages in the manufacture and sale of anchor chains, marine mooring chains, and related accessories worldwide.

High growth potential with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor