- Taiwan

- /

- Electronic Equipment and Components

- /

- TPEX:8069

High Growth Tech Stocks To Watch Now

Reviewed by Simply Wall St

As global markets celebrate the prospect of upcoming interest rate cuts, small-cap stocks have notably outperformed their larger counterparts, driven by renewed investor optimism. In this favorable environment, identifying high-growth tech stocks becomes crucial for investors looking to capitalize on market momentum and technological innovation.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| TG Therapeutics | 28.62% | 43.05% | ★★★★★★ |

| Sarepta Therapeutics | 24.22% | 44.94% | ★★★★★★ |

| Seojin SystemLtd | 33.61% | 52.05% | ★★★★★★ |

| eWeLLLtd | 26.52% | 27.53% | ★★★★★★ |

| Medley | 24.97% | 30.50% | ★★★★★★ |

| Facilities by ADF | 32.33% | 94.46% | ★★★★★★ |

| G1 Therapeutics | 27.57% | 57.75% | ★★★★★★ |

| KebNi | 34.75% | 86.11% | ★★★★★★ |

| Adveritas | 66.47% | 103.87% | ★★★★★★ |

| UTI | 103.56% | 122.67% | ★★★★★★ |

Click here to see the full list of 1276 stocks from our High Growth Tech and AI Stocks screener.

Let's review some notable picks from our screened stocks.

Bilibili (NasdaqGS:BILI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bilibili Inc. offers online entertainment services targeting young generations in the People’s Republic of China, with a market cap of approximately $6.19 billion.

Operations: Bilibili Inc. generates revenue primarily through its Internet Information Providers segment, amounting to CN¥23.95 billion. The company focuses on delivering online entertainment services tailored for younger audiences in China.

Bilibili's revenue is forecast to grow at 11.1% per year, outpacing the US market's 8.8%. Despite a net loss of ¥608.7 million in Q2 2024, down from ¥1,546.71 million a year ago, the company shows promising signs with earnings expected to grow by 77.77% annually. The company invests significantly in R&D to drive innovation and user engagement; this strategic focus positions Bilibili as a dynamic player within high-growth tech sectors despite current profitability challenges.

- Dive into the specifics of Bilibili here with our thorough health report.

Review our historical performance report to gain insights into Bilibili's's past performance.

International Games SystemLtd (TPEX:3293)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: International Games System Co., Ltd. engages in the planning, designing, researching, developing, manufacturing, marketing, servicing, and licensing of arcade, online, and mobile games primarily in Taiwan, the United Kingdom, and China with a market cap of NT$236.99 billion.

Operations: The company generates revenue primarily through its Online Games Division (NT$8.99 billion) and Business Game Division (NT$7.13 billion). Its operations span the planning, designing, researching, developing, manufacturing, marketing, servicing, and licensing of various game types across Taiwan, the United Kingdom, and China.

International Games System Ltd. (IGS) is showcasing impressive growth with a 20.6% annual revenue increase, outpacing the TW market's 11.8%. The company's earnings are also forecasted to grow at 19.4% per year, slightly above the market average of 18.7%. Notably, IGS reported Q2 sales of TWD 4.58 billion and net income of TWD 2.28 billion, reflecting strong performance compared to last year's figures of TWD 3.48 billion and TWD 1.66 billion respectively. Investing heavily in R&D, IGS spent a significant portion on innovation to maintain its competitive edge in the tech sector; this strategic focus is evident from their robust financial results and consistent product advancements within gaming technology segments. With software firms increasingly adopting SaaS models for recurring revenue streams, IGS’s commitment to research positions it well for sustained growth in an evolving industry landscape.

- Navigate through the intricacies of International Games SystemLtd with our comprehensive health report here.

Gain insights into International Games SystemLtd's past trends and performance with our Past report.

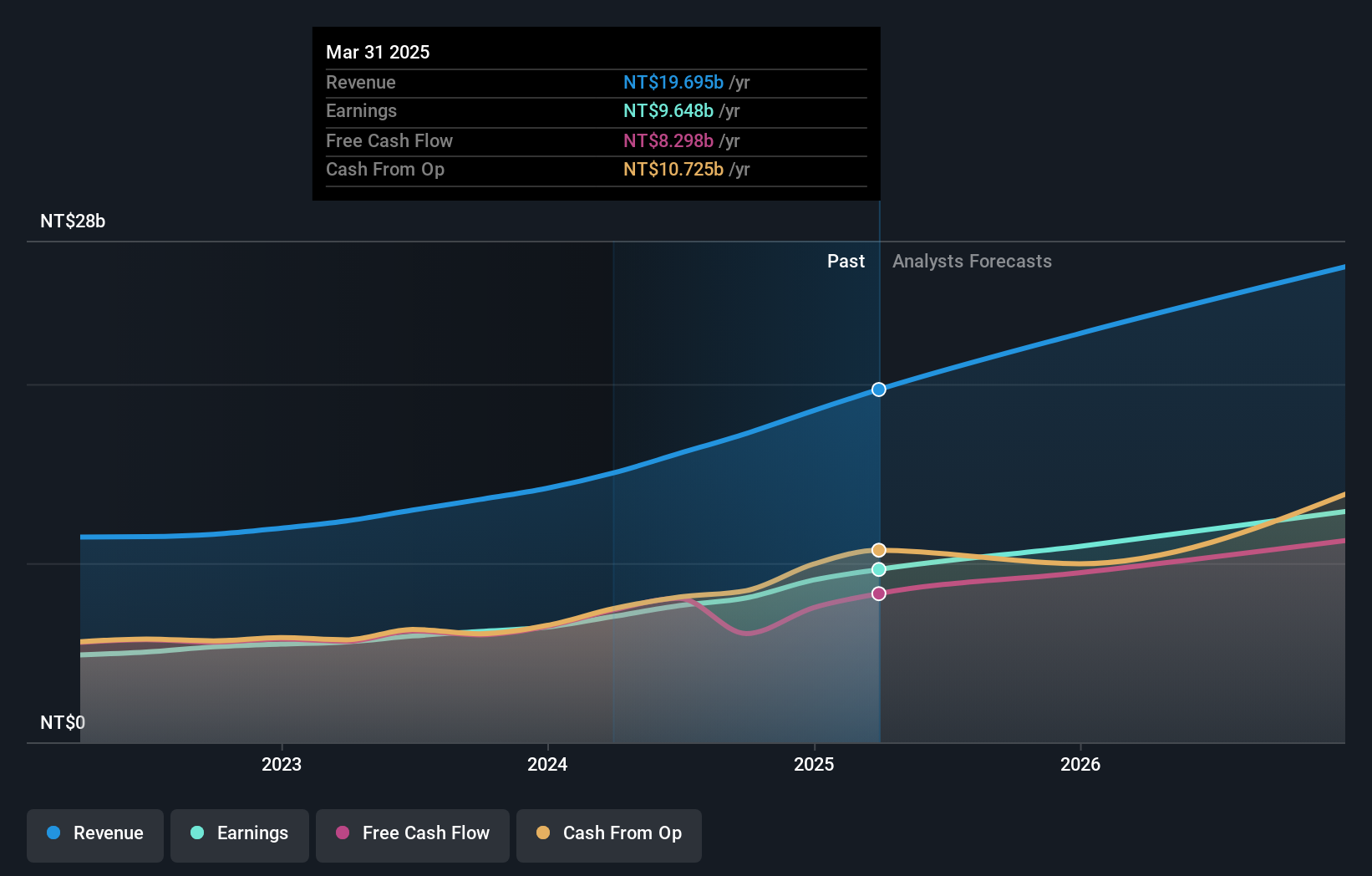

E Ink Holdings (TPEX:8069)

Simply Wall St Growth Rating: ★★★★★★

Overview: E Ink Holdings Inc. researches, develops, manufactures, and sells electronic paper display panels worldwide with a market cap of NT$345.62 billion.

Operations: E Ink Holdings generates revenue primarily from the sale of electronic components and parts, amounting to NT$25.95 billion. The company's business involves extensive research, development, and manufacturing activities focused on electronic paper display panels for a global market.

E Ink Holdings is making strides in the tech sector with a forecasted annual revenue growth of 30.6%, significantly outpacing the TW market's 11.9%. Despite a recent 31.9% drop in earnings, the company anticipates a robust profit growth rate of 35.8% annually over the next three years, driven by innovative products like the T2000 timing controller ASIC for ePaper displays. Investing heavily in R&D, E Ink spent TWD 1.49 billion on new production equipment to bolster future capabilities and maintain its competitive edge in display technology advancements.

- Take a closer look at E Ink Holdings' potential here in our health report.

Gain insights into E Ink Holdings' historical performance by reviewing our past performance report.

Seize The Opportunity

- Discover the full array of 1276 High Growth Tech and AI Stocks right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if E Ink Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:8069

E Ink Holdings

Researches, develops, manufactures, and sells electronic paper display panels worldwide.

Exceptional growth potential with excellent balance sheet.