- Taiwan

- /

- Electronic Equipment and Components

- /

- TPEX:6732

Is There More To The Story Than Sensortek Technology's (GTSM:6732) Earnings Growth?

Broadly speaking, profitable businesses are less risky than unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. This article will consider whether Sensortek Technology's (GTSM:6732) statutory profits are a good guide to its underlying earnings.

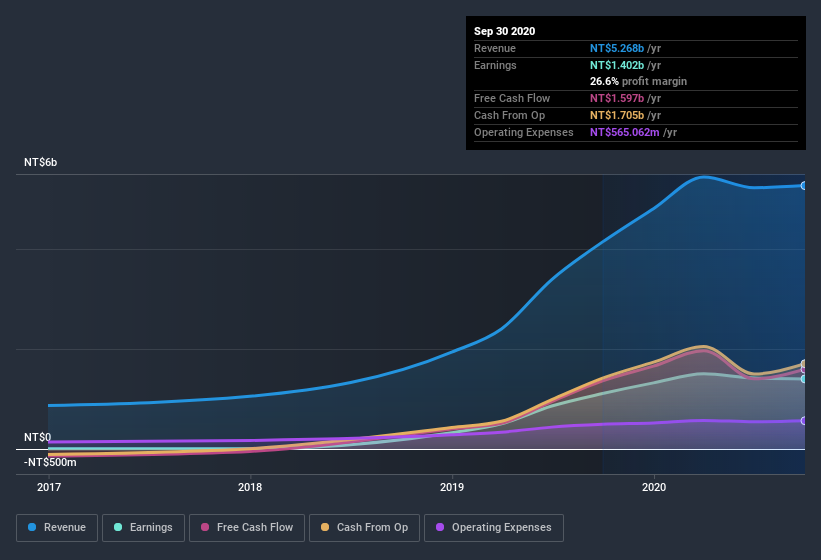

We like the fact that Sensortek Technology made a profit of NT$1.40b on its revenue of NT$5.27b, in the last year. In the chart below, you can see that its profit and revenue have both grown over the last three years.

Check out our latest analysis for Sensortek Technology

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. As a result, we'll today take a look at how dilution and cashflow shape our understanding of Sensortek Technology's earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Sensortek Technology.

Examining Cashflow Against Sensortek Technology's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Sensortek Technology has an accrual ratio of -7.34 for the year to September 2020. Therefore, its statutory earnings were very significantly less than its free cashflow. To wit, it produced free cash flow of NT$1.6b during the period, dwarfing its reported profit of NT$1.40b. Sensortek Technology's free cash flow improved over the last year, which is generally good to see. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. Sensortek Technology expanded the number of shares on issue by 9.5% over the last year. Therefore, each share now receives a smaller portion of profit. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Sensortek Technology's historical EPS growth by clicking on this link.

How Is Dilution Impacting Sensortek Technology's Earnings Per Share? (EPS)

Sensortek Technology has improved its profit over the last three years, with an annualized gain of 26,486% in that time. But EPS was only up 14,971% per year, in the exact same period. And at a glance the 26% gain in profit over the last year impresses. But in comparison, EPS only increased by 23% over the same period. So you can see that the dilution has had a bit of an impact on shareholders. Therefore, the dilution is having a noteworthy influence on shareholder returns. And so, you can see quite clearly that dilution is influencing shareholder earnings.

In the long term, earnings per share growth should beget share price growth. So it will certainly be a positive for shareholders if Sensortek Technology can grow EPS persistently. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On Sensortek Technology's Profit Performance

In conclusion, Sensortek Technology has strong cashflow relative to earnings, which indicates good quality earnings, but the dilution means its earnings per share growth is weaker than its profit growth. Considering all the aforementioned, we'd venture that Sensortek Technology's profit result is a pretty good guide to its true profitability, albeit a bit on the conservative side. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example - Sensortek Technology has 3 warning signs we think you should be aware of.

Our examination of Sensortek Technology has focussed on certain factors that can make its earnings look better than they are. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you decide to trade Sensortek Technology, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:6732

Sensortek Technology

A chip design company, provides various sensor chips for smart phones and wearable devices in Taiwan.

Flawless balance sheet second-rate dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion