Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:6573

Improved Revenues Required Before HY Electronic (Cayman) Limited (TWSE:6573) Stock's 26% Jump Looks Justified

HY Electronic (Cayman) Limited (TWSE:6573) shares have continued their recent momentum with a 26% gain in the last month alone. Taking a wider view, although not as strong as the last month, the full year gain of 13% is also fairly reasonable.

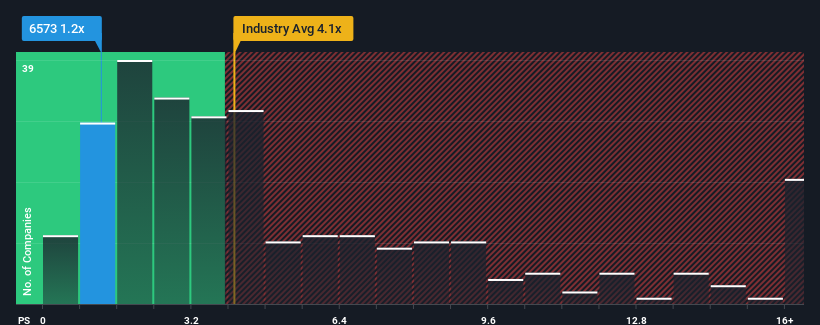

Even after such a large jump in price, HY Electronic (Cayman) may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 1.2x, since almost half of all companies in the Semiconductor industry in Taiwan have P/S ratios greater than 4.1x and even P/S higher than 8x are not unusual. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for HY Electronic (Cayman)

What Does HY Electronic (Cayman)'s Recent Performance Look Like?

For instance, HY Electronic (Cayman)'s receding revenue in recent times would have to be some food for thought. Perhaps the market believes the recent revenue performance isn't good enough to keep up the industry, causing the P/S ratio to suffer. Those who are bullish on HY Electronic (Cayman) will be hoping that this isn't the case so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for HY Electronic (Cayman), take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is HY Electronic (Cayman)'s Revenue Growth Trending?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like HY Electronic (Cayman)'s to be considered reasonable.

Retrospectively, the last year delivered a frustrating 5.1% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 38% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Comparing that to the industry, which is predicted to deliver 27% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

In light of this, it's understandable that HY Electronic (Cayman)'s P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as recent revenue trends are already weighing down the shares.

The Key Takeaway

Shares in HY Electronic (Cayman) have risen appreciably however, its P/S is still subdued. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

It's no surprise that HY Electronic (Cayman) maintains its low P/S off the back of its sliding revenue over the medium-term. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

You need to take note of risks, for example - HY Electronic (Cayman) has 3 warning signs (and 1 which is a bit concerning) we think you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if HY Electronic (Cayman) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6573

HY Electronic (Cayman)

Engages in research and development, manufacture, and sale of rectifier diodes, bridge rectifiers, solar diodes, and wafers in China, Asia, Europe, and internationally.

Mediocre balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor