Advertisement

As the global economy navigates a complex landscape marked by fluctuating consumer sentiment and evolving trade dynamics, Asian markets have shown resilience, with Chinese stocks experiencing a modest rise amid easing U.S.-China tensions. In this environment, identifying promising opportunities requires a keen eye for companies that demonstrate strong fundamentals and adaptability to shifting economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Tsubakimoto Kogyo | NA | 7.85% | 12.88% | ★★★★★★ |

| Cresco | 4.98% | 9.33% | 11.61% | ★★★★★★ |

| Kyoritsu Electric | 3.87% | 6.01% | 17.16% | ★★★★★★ |

| Yashima Denki | 2.28% | 2.70% | 25.81% | ★★★★★★ |

| DoshishaLtd | NA | 3.17% | 3.20% | ★★★★★★ |

| Hyakugo Bank | 172.81% | 6.28% | 7.46% | ★★★★★☆ |

| KinjiroLtd | 20.72% | 11.66% | 24.80% | ★★★★★☆ |

| Nippon Ski Resort DevelopmentLtd | 38.68% | 15.71% | 60.81% | ★★★★★☆ |

| Iljin DiamondLtd | 2.18% | -3.74% | 9.21% | ★★★★☆☆ |

| ILSEUNG | 34.83% | -10.92% | 30.64% | ★★★★☆☆ |

We'll examine a selection from our screener results.

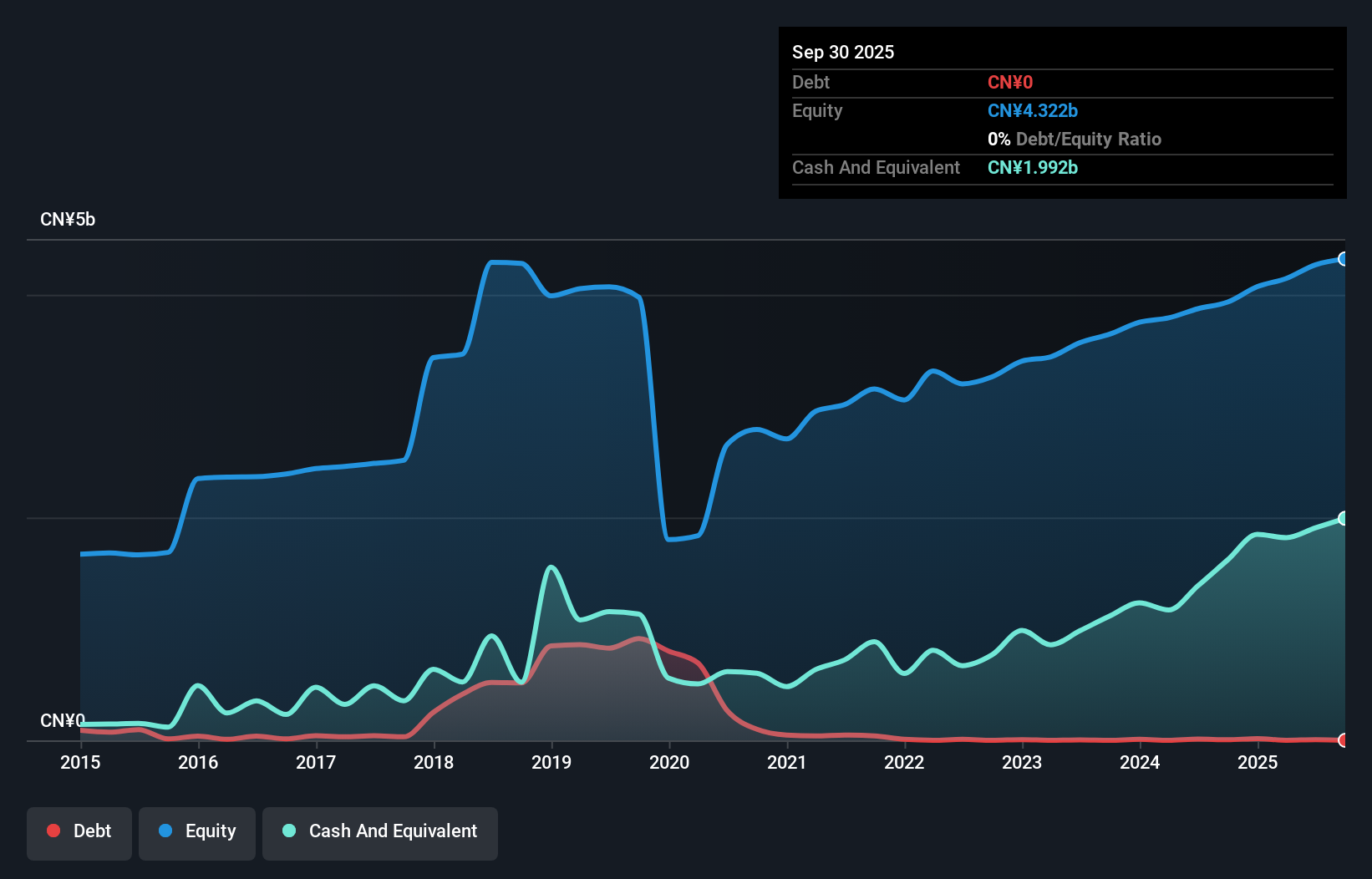

Suzhou Hailu Heavy IndustryLtd (SZSE:002255)

Simply Wall St Value Rating: ★★★★★★

Overview: Suzhou Hailu Heavy Industry Co., Ltd specializes in the design, manufacture, and sale of industrial waste heat boilers, large and special material pressure vessels, and nuclear safety equipment with a market capitalization of CN¥12.35 billion.

Operations: Suzhou Hailu Heavy Industry generates revenue primarily from the sale of industrial waste heat boilers, large and special material pressure vessels, and nuclear safety equipment. The company's net profit margin has shown fluctuations over recent periods.

Suzhou Hailu Heavy Industry, a nimble player in the machinery sector, showcases robust financial health with no debt on its books and a notable 31.4% earnings growth over the past year. This growth outpaces the broader industry rate of 6.4%, highlighting its competitive edge. Despite recent volatility in share price, the company remains attractive with a price-to-earnings ratio of 27.1x, which is favorable compared to China's market average of 45x. Recent earnings reports show net income rising to CNY 319 million for nine months ending September 2025 from CNY 241 million last year, reflecting strong operational performance despite slightly lower sales figures.

- Navigate through the intricacies of Suzhou Hailu Heavy IndustryLtd with our comprehensive health report here.

Learn about Suzhou Hailu Heavy IndustryLtd's historical performance.

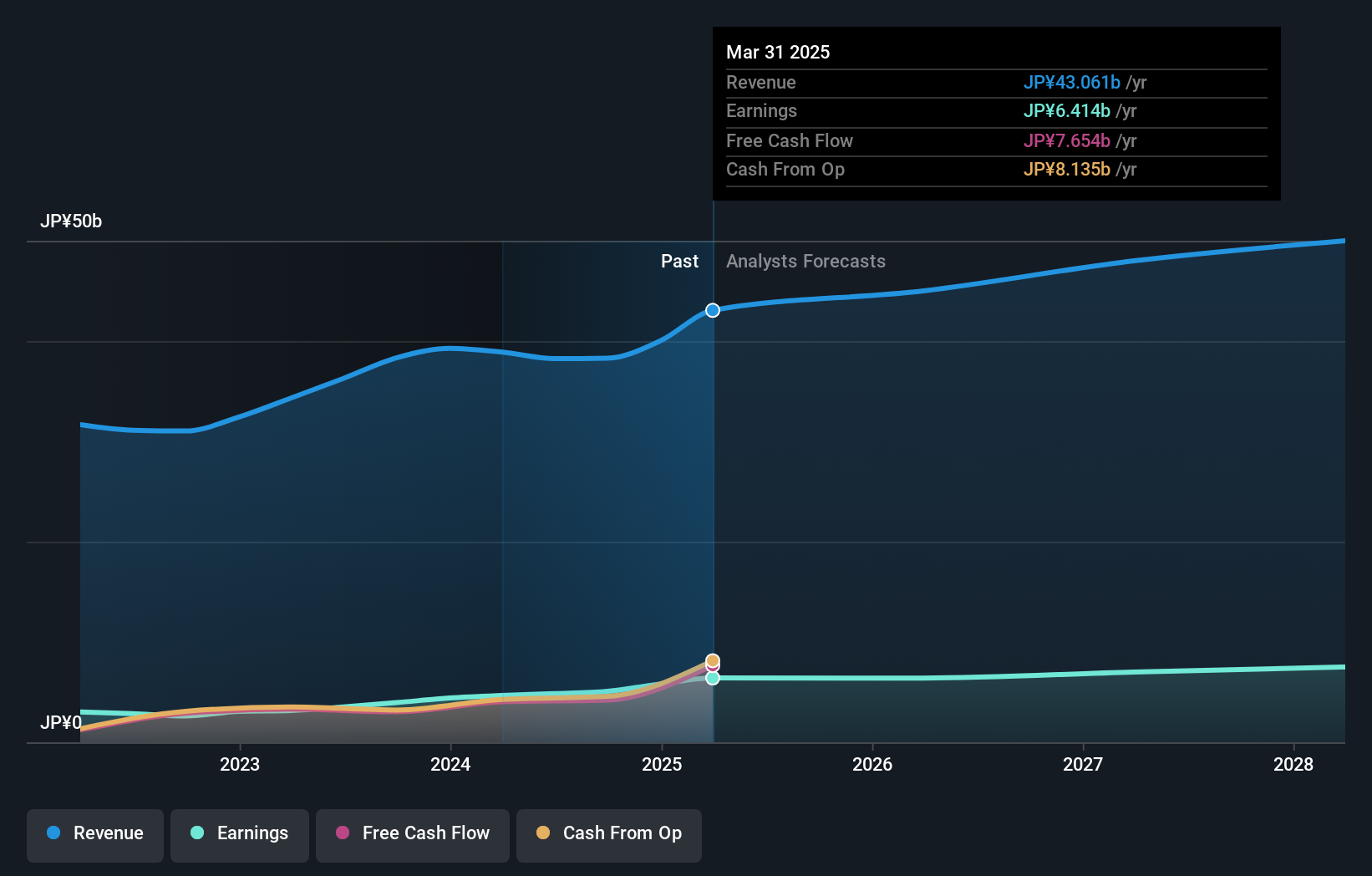

Nihon Dengi (TSE:1723)

Simply Wall St Value Rating: ★★★★★★

Overview: Nihon Dengi Co., Ltd. specializes in designing and constructing automatic control systems in Japan, with a market cap of ¥101.49 billion.

Operations: Nihon Dengi generates revenue primarily from designing and constructing automatic control systems. The company's market cap stands at ¥101.49 billion.

Nihon Dengi, a promising player in the building industry, has shown impressive financial health with earnings growth of 52.2% over the past year, outpacing the industry's 1.9%. This debt-free company trades at an attractive 30.6% below its estimated fair value and boasts high-quality earnings. Recent guidance forecasts net sales of ¥46 billion (US$), with operating profit expected to hit ¥10.5 billion (US$). However, dividends have decreased to ¥71 per share from last year's ¥81 per share. Despite this cutback, inclusion in the S&P Global BMI Index underscores its growing market recognition and potential for future growth.

- Dive into the specifics of Nihon Dengi here with our thorough health report.

Evaluate Nihon Dengi's historical performance by accessing our past performance report.

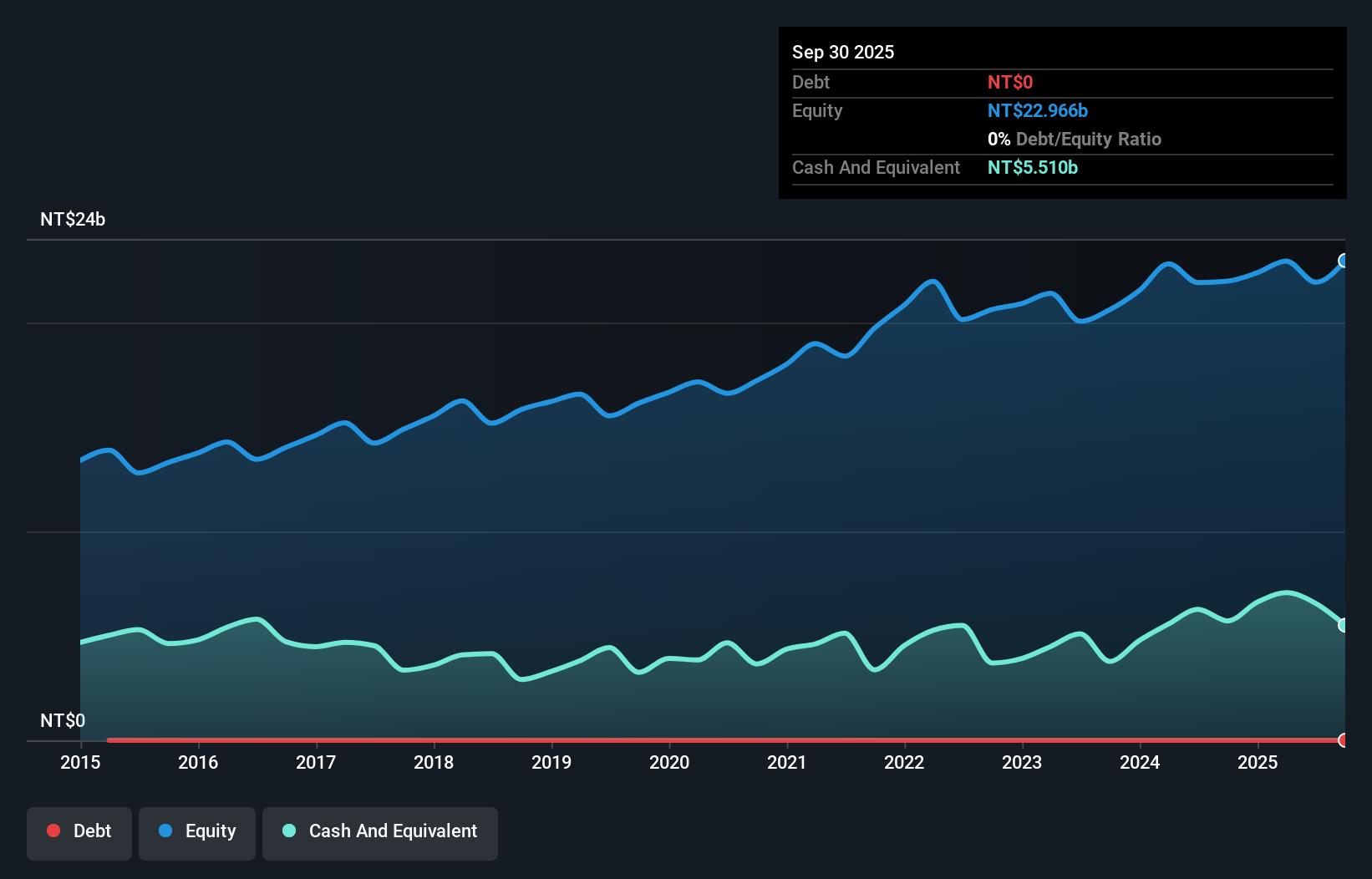

Greatek Electronics (TWSE:2441)

Simply Wall St Value Rating: ★★★★★★

Overview: Greatek Electronics Inc., along with its subsidiaries, offers semiconductor assembly and testing services across Taiwan, Asia, America, Europe, and Africa with a market capitalization of NT$44.03 billion.

Operations: The primary revenue stream for Greatek Electronics comes from its semiconductor segment, generating NT$16.36 billion.

Greatek Electronics, a nimble player in the semiconductor sector, shows promising attributes despite some challenges. With earnings growth of 0.8% over the past year, it outpaced the industry's -2.3% performance, highlighting its resilience. The company is debt-free and boasts high-quality earnings with a favorable price-to-earnings ratio of 18.4x compared to the Taiwan market's 20.7x, indicating good value potential. Recent quarterly sales hit TWD 4,250 million from TWD 3,860 million last year; however, net income for nine months fell slightly to TWD 1,811 million from TWD 1,918 million previously—showcasing mixed results but maintaining profitability.

- Take a closer look at Greatek Electronics' potential here in our health report.

Assess Greatek Electronics' past performance with our detailed historical performance reports.

Turning Ideas Into Actions

- Click this link to deep-dive into the 2431 companies within our Asian Undiscovered Gems With Strong Fundamentals screener.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002255

Suzhou Hailu Heavy IndustryLtd

Designs, manufactures, and sells industrial waste heat boilers, large and special material pressure vessels, and nuclear safety equipment.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor