Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:2449

Has King Yuan Electronics Co., Ltd.'s (TPE:2449) Impressive Stock Performance Got Anything to Do With Its Fundamentals?

King Yuan Electronics' (TPE:2449) stock is up by a considerable 34% over the past three months. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. Particularly, we will be paying attention to King Yuan Electronics' ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for King Yuan Electronics

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for King Yuan Electronics is:

14% = NT$4.0b ÷ NT$28b (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. Another way to think of that is that for every NT$1 worth of equity, the company was able to earn NT$0.14 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

King Yuan Electronics' Earnings Growth And 14% ROE

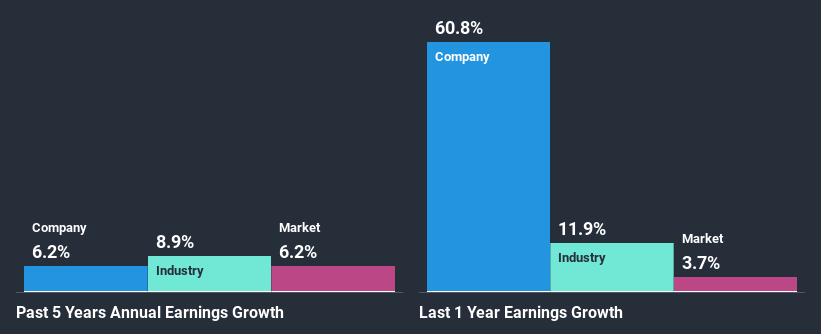

At first glance, King Yuan Electronics seems to have a decent ROE. On comparing with the average industry ROE of 11% the company's ROE looks pretty remarkable. This probably laid the ground for King Yuan Electronics' moderate 6.2% net income growth seen over the past five years.

Next, on comparing with the industry net income growth, we found that King Yuan Electronics' reported growth was lower than the industry growth of 8.9% in the same period, which is not something we like to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if King Yuan Electronics is trading on a high P/E or a low P/E, relative to its industry.

Is King Yuan Electronics Making Efficient Use Of Its Profits?

King Yuan Electronics has a significant three-year median payout ratio of 70%, meaning that it is left with only 30% to reinvest into its business. This implies that the company has been able to achieve decent earnings growth despite returning most of its profits to shareholders.

Moreover, King Yuan Electronics is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 70%. As a result, King Yuan Electronics' ROE is not expected to change by much either, which we inferred from the analyst estimate of 13% for future ROE.

Conclusion

In total, it does look like King Yuan Electronics has some positive aspects to its business. Its earnings have grown respectably as we saw earlier, which was likely due to the company reinvesting its earnings at a pretty high rate of return. However, given the high ROE, we do think that the company is reinvesting a small portion of its profits. This could likely be preventing the company from growing to its full extent. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

When trading King Yuan Electronics or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if King Yuan Electronics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:2449

King Yuan Electronics

Engages in the designing, manufacturing, selling, testing, and assembly service of integrated circuits in Taiwan, Asia, North America, and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|59.6% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.8% undervalued

ZW

Community Contributor