Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, CoAsia Electronics Corp. (GTSM:8096) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for CoAsia Electronics

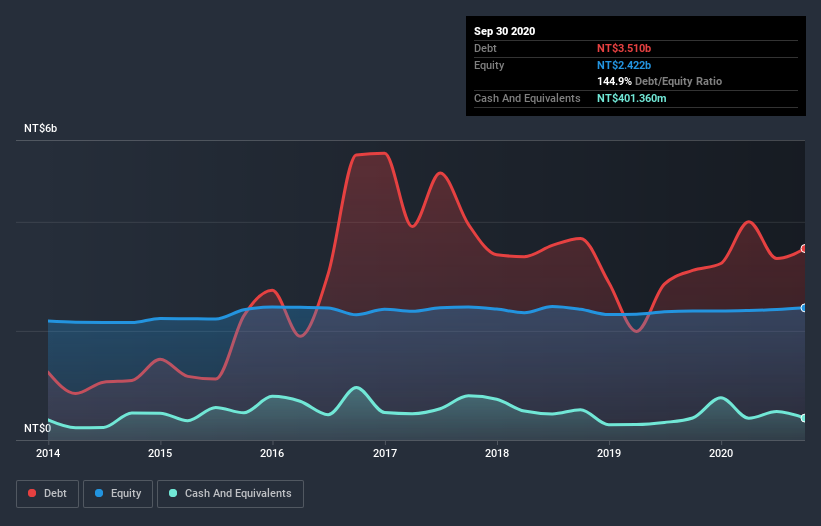

What Is CoAsia Electronics's Net Debt?

The image below, which you can click on for greater detail, shows that at September 2020 CoAsia Electronics had debt of NT$3.51b, up from NT$3.11b in one year. However, it also had NT$401.4m in cash, and so its net debt is NT$3.11b.

A Look At CoAsia Electronics's Liabilities

The latest balance sheet data shows that CoAsia Electronics had liabilities of NT$4.22b due within a year, and liabilities of NT$34.3m falling due after that. On the other hand, it had cash of NT$401.4m and NT$3.79b worth of receivables due within a year. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

Since publicly traded CoAsia Electronics shares are worth a total of NT$1.94b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

CoAsia Electronics has a rather high debt to EBITDA ratio of 13.0 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 3.3 times, suggesting it can responsibly service its obligations. The silver lining is that CoAsia Electronics grew its EBIT by 107% last year, which nourishing like the idealism of youth. If that earnings trend continues it will make its debt load much more manageable in the future. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since CoAsia Electronics will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, CoAsia Electronics's free cash flow amounted to 47% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Based on what we've seen CoAsia Electronics is not finding it easy, given its net debt to EBITDA, but the other factors we considered give us cause to be optimistic. In particular, we are dazzled with its EBIT growth rate. Considering this range of data points, we think CoAsia Electronics is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 4 warning signs we've spotted with CoAsia Electronics (including 2 which is are a bit concerning) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade CoAsia Electronics, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:8096

CoAsia Electronics

Provides components for mobile multimedia in Taiwan, China, the United States, Southeast Asia, India, and Korea.

Mediocre balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor