Advertisement

- Taiwan

- /

- Semiconductors

- /

- TPEX:5425

These 4 Measures Indicate That Taiwan Semiconductor (GTSM:5425) Is Using Debt Reasonably Well

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Taiwan Semiconductor Co., Ltd. (GTSM:5425) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Taiwan Semiconductor

What Is Taiwan Semiconductor's Net Debt?

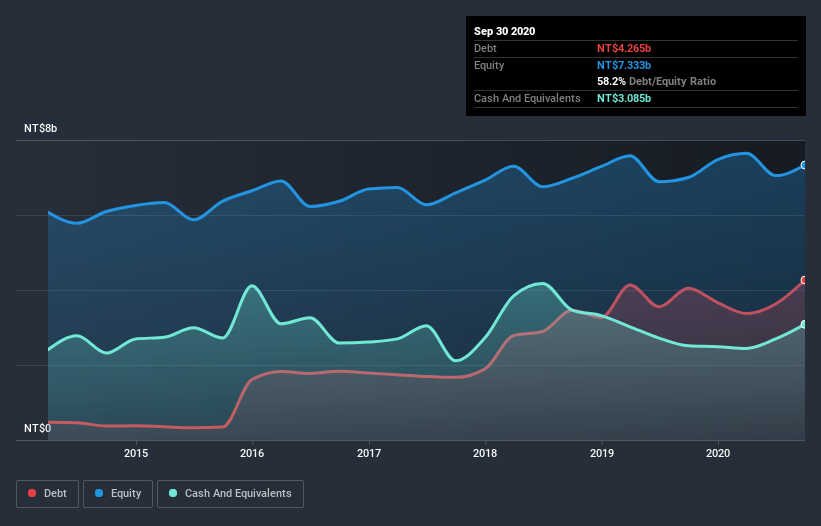

As you can see below, at the end of September 2020, Taiwan Semiconductor had NT$4.27b of debt, up from NT$4.05b a year ago. Click the image for more detail. However, because it has a cash reserve of NT$3.09b, its net debt is less, at about NT$1.18b.

How Healthy Is Taiwan Semiconductor's Balance Sheet?

We can see from the most recent balance sheet that Taiwan Semiconductor had liabilities of NT$4.62b falling due within a year, and liabilities of NT$2.60b due beyond that. On the other hand, it had cash of NT$3.09b and NT$2.13b worth of receivables due within a year. So it has liabilities totalling NT$2.01b more than its cash and near-term receivables, combined.

Since publicly traded Taiwan Semiconductor shares are worth a total of NT$12.5b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Taiwan Semiconductor has a low net debt to EBITDA ratio of only 0.63. And its EBIT easily covers its interest expense, being 120 times the size. So we're pretty relaxed about its super-conservative use of debt. But the bad news is that Taiwan Semiconductor has seen its EBIT plunge 15% in the last twelve months. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Taiwan Semiconductor's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Taiwan Semiconductor recorded free cash flow worth 56% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

On our analysis Taiwan Semiconductor's interest cover should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. In particular, EBIT growth rate gives us cold feet. Considering this range of data points, we think Taiwan Semiconductor is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 2 warning signs we've spotted with Taiwan Semiconductor .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

When trading Taiwan Semiconductor or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Taiwan Semiconductor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:5425

Taiwan Semiconductor

Manufactures and sells rectifiers and bar code printers in Asia, the United States, Europe, and internationally.

Excellent balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor