Advertisement

- Taiwan

- /

- Semiconductors

- /

- TPEX:3490

Something To Consider Before Buying Single Well Industrial Corporation (GTSM:3490) For The 1.6% Dividend

Is Single Well Industrial Corporation (GTSM:3490) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. Yet sometimes, investors buy a stock for its dividend and lose money because the share price falls by more than they earned in dividend payments.

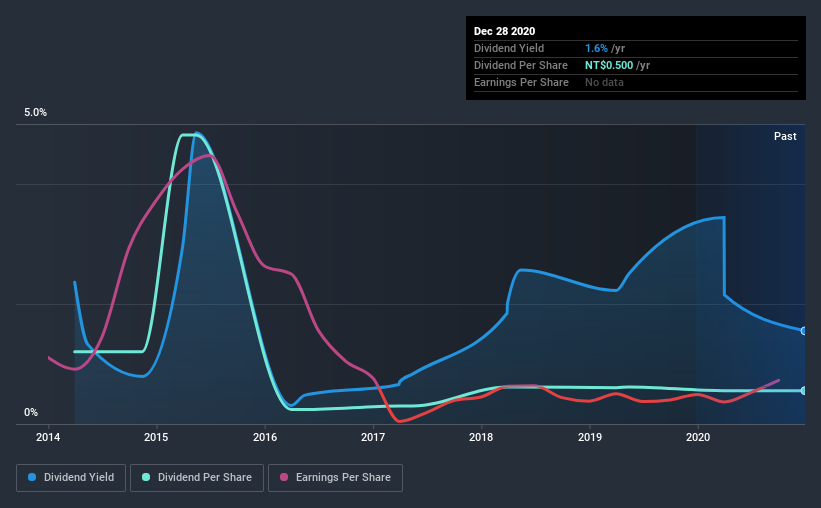

With a 1.6% yield and a seven-year payment history, investors probably think Single Well Industrial looks like a reliable dividend stock. A 1.6% yield is not inspiring, but the longer payment history has some appeal. During the year, the company also conducted a buyback equivalent to around 3.8% of its market capitalisation. Before you buy any stock for its dividend however, you should always remember Warren Buffett's two rules: 1) Don't lose money, and 2) Remember rule #1. We'll run through some checks below to help with this.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. In the last year, Single Well Industrial paid out 154% of its profit as dividends. A payout ratio above 100% is definitely an item of concern, unless there are some other circumstances that would justify it.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. Single Well Industrial paid out a conservative 29% of its free cash flow as dividends last year. It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Single Well Industrial fortunately did generate enough cash to fund its dividend. If executives were to continue paying more in dividends than the company reported in profits, we'd view this as a warning sign. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

With a strong net cash balance, Single Well Industrial investors may not have much to worry about in the near term from a dividend perspective.

We update our data on Single Well Industrial every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Single Well Industrial has been paying a dividend for the past seven years. Although it has been paying a dividend for several years now, the dividend has been cut at least once, and we're cautious about the consistency of its dividend across a full economic cycle. During the past seven-year period, the first annual payment was NT$1.1 in 2013, compared to NT$0.5 last year. This works out to a decline of approximately 54% over that time.

We struggle to make a case for buying Single Well Industrial for its dividend, given that payments have shrunk over the past seven years.

Dividend Growth Potential

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. Single Well Industrial's EPS have fallen by approximately 49% per year during the past five years. With this kind of significant decline, we always wonder what has changed in the business. Dividends are about stability, and Single Well Industrial's earnings per share, which support the dividend, have been anything but stable.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. We're a bit uncomfortable with its high payout ratio, although at least the dividend was covered by free cash flow. Second, earnings per share have been in decline, and its dividend has been cut at least once in the past. With this information in mind, we think Single Well Industrial may not be an ideal dividend stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 3 warning signs for Single Well Industrial (of which 1 can't be ignored!) you should know about.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you’re looking to trade Single Well Industrial, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:3490

Single Well Industrial

Manufactures and sells packaging molds, automation equipment, and solar energy products in Taiwan.

Mediocre balance sheet unattractive dividend payer.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor