- Taiwan

- /

- Real Estate

- /

- TWSE:2520

Unveiling None And 2 Other Undiscovered Gems With Promising Potential

Reviewed by Simply Wall St

In a week marked by geopolitical tensions and consumer spending concerns, major U.S. indices experienced declines, with the S&P 500 and Nasdaq Composite both retreating from record highs. Amidst this backdrop of uncertainty and cautious sentiment, investors are increasingly on the lookout for undiscovered gems—stocks that may offer promising potential despite broader market volatility.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Force Motors | 8.95% | 26.62% | 61.62% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Wuxi Chemical Equipment | NA | 12.26% | -0.74% | ★★★★★★ |

| Grade Upon Technology | 4.99% | 7.57% | 67.08% | ★★★★★★ |

| Silvery Dragon Prestressed MaterialsLTD Tianjin | 31.26% | 0.80% | 0.71% | ★★★★☆☆ |

| Changshu Fengfan Power Equipment | 91.61% | 6.89% | 31.92% | ★★★★☆☆ |

| Yukiguni Maitake | 126.48% | -5.17% | -33.78% | ★★★★☆☆ |

| Central Cooperative Bank AD | 4.88% | 37.94% | 537.05% | ★★★★☆☆ |

| Sichuan Dowell Science and Technology | 34.59% | 12.97% | -14.44% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

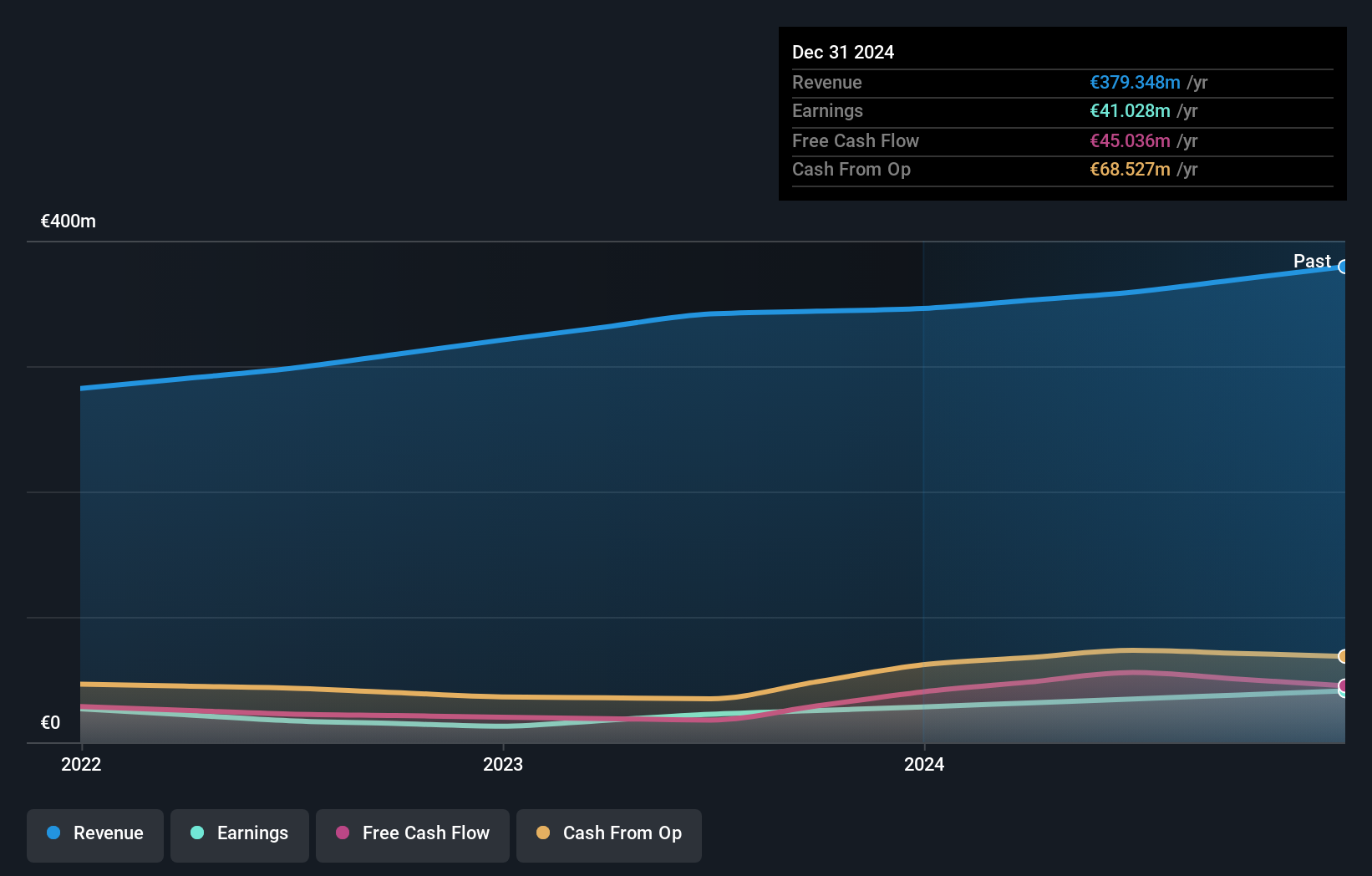

Spadel (ENXTBR:SPA)

Simply Wall St Value Rating: ★★★★★★

Overview: Spadel SA is a company that produces and markets natural mineral water in Belgium, with a market capitalization of €780.27 million.

Operations: Spadel generates revenue primarily from its non-alcoholic beverages segment, amounting to €359.03 million. The company's market capitalization stands at €780.27 million.

Spadel, a nimble player in the beverage sector, presents an intriguing profile with its debt-free status and impressive earnings growth of 54% over the past year. This growth outpaces the broader industry rate of 5.7%, highlighting its competitive edge. Despite a historical decline in earnings by 5.1% annually over five years, Spadel's high-quality earnings and positive free cash flow underscore its financial health. Trading at roughly 73% below estimated fair value, it seems undervalued, offering potential upside for investors seeking opportunities in this space.

- Click here and access our complete health analysis report to understand the dynamics of Spadel.

Review our historical performance report to gain insights into Spadel's's past performance.

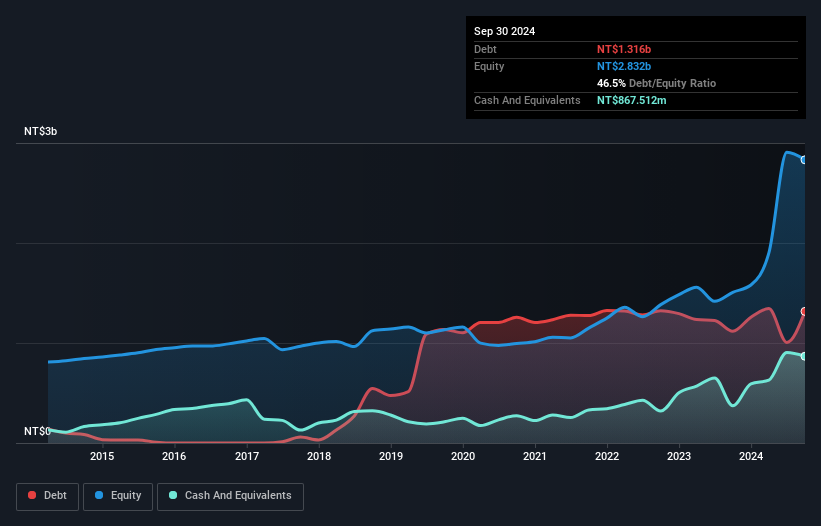

Eris Technology (TPEX:3675)

Simply Wall St Value Rating: ★★★★★★

Overview: Eris Technology Corporation, with a market cap of NT$11.90 billion, operates as an original design manufacturer offering design, manufacturing, and after-marketing services for diode products.

Operations: Eris Technology's revenue streams include contributions from Yea Shin Technology at NT$1.42 billion and Dewei Technology and Jiecheng at NT$1.75 billion.

Eris Technology, a nimble player in the semiconductor space, showcases robust financial health. Its debt to equity ratio has impressively decreased from 100.2% to 46.5% over five years, indicating prudent financial management. The company's earnings growth of 13.1% outpaced the industry average of 5.9%, reflecting its competitive edge and operational efficiency. With a price-to-earnings ratio of 28.9x below the industry norm of 30.4x, Eris seems attractively valued for those seeking opportunities in this sector. Additionally, its net debt to equity ratio at 15.8% is satisfactory, ensuring stability amidst market fluctuations while maintaining high-quality earnings throughout recent periods.

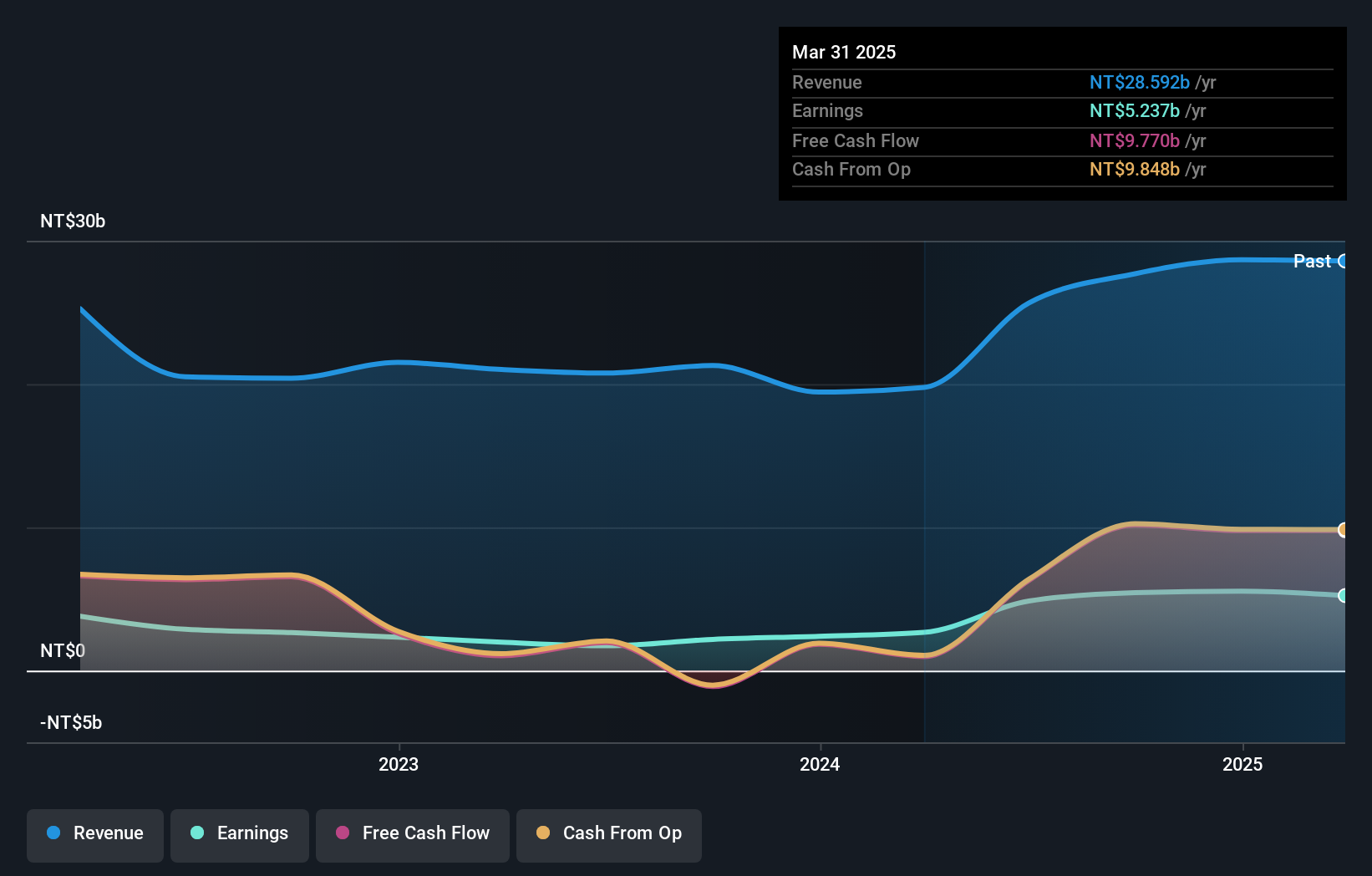

Kindom Development (TWSE:2520)

Simply Wall St Value Rating: ★★★★★★

Overview: Kindom Development Co., Ltd. is a company that constructs, develops, and sells real estate properties in Taiwan, with a market capitalization of NT$30.05 billion.

Operations: Kindom Development generates revenue primarily from its manufacturing and construction segments, with NT$15.39 billion and NT$13.98 billion respectively, while its department store operations contribute NT$1.76 billion.

Kindom Development shines with a notable 149% earnings growth over the past year, outpacing the real estate sector's 58%. Trading at a significant 87% below its estimated fair value, it presents an intriguing opportunity. The company's debt to equity ratio has impressively dropped from 196% to 61% in five years, reflecting robust financial health. Recent acquisition of construction land for TWD1.35 billion suggests strategic expansion efforts are underway. With interest payments well covered by EBIT at over 110 times and more cash than total debt, Kindom seems poised for steady growth while maintaining high-quality earnings performance.

- Delve into the full analysis health report here for a deeper understanding of Kindom Development.

Understand Kindom Development's track record by examining our Past report.

Taking Advantage

- Gain an insight into the universe of 4757 Undiscovered Gems With Strong Fundamentals by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kindom Development might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2520

Kindom Development

Kindom Development Co., Ltd., together with its subsidiaries, constructs, develops, and sells real estate properties in Taiwan.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion