Advertisement

Great China Metal Ind Full Year 2024 Earnings: EPS: NT$1.63 (vs NT$1.45 in FY 2023)

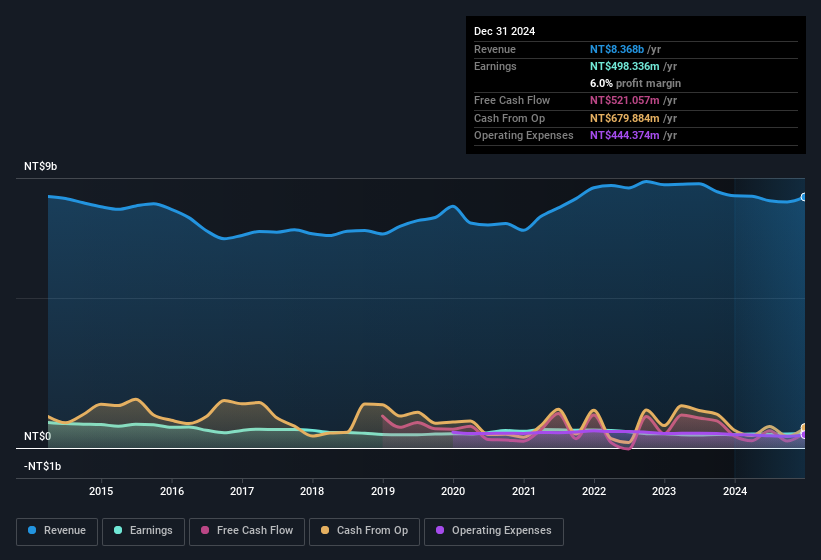

Great China Metal Ind (TWSE:9905) Full Year 2024 Results

Key Financial Results

- Revenue: NT$8.37b (flat on FY 2023).

- Net income: NT$498.3m (up 13% from FY 2023).

- Profit margin: 6.0% (up from 5.3% in FY 2023).

- EPS: NT$1.63 (up from NT$1.45 in FY 2023).

All figures shown in the chart above are for the trailing 12 month (TTM) period

Great China Metal Ind's share price is broadly unchanged from a week ago.

Risk Analysis

It's necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Great China Metal Ind (at least 1 which is concerning), and understanding these should be part of your investment process.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:9905

Great China Metal Ind

Manufactures and supplies food and beverage packaging containers in Taiwan and internationally.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor