Advertisement

In the current global market landscape, small-cap stocks have faced challenges as cautious Federal Reserve commentary and political uncertainties weigh on investor sentiment. Despite a backdrop of economic growth and positive jobs data, smaller-cap indexes have struggled, highlighting the importance of identifying promising companies that can navigate these turbulent times. In this environment, a good stock is often characterized by strong fundamentals and resilience to broader market fluctuations—qualities that can help it emerge as an undiscovered gem with potential for growth.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Canal Shipping Agencies | NA | 8.92% | 22.01% | ★★★★★★ |

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Parker Drilling | 46.05% | 0.86% | 52.25% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Invest Bank | 135.69% | 11.07% | 18.67% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Castellana Properties Socimi | 53.49% | 6.65% | 21.96% | ★★★★☆☆ |

| DIRTT Environmental Solutions | 58.73% | -5.34% | -5.43% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

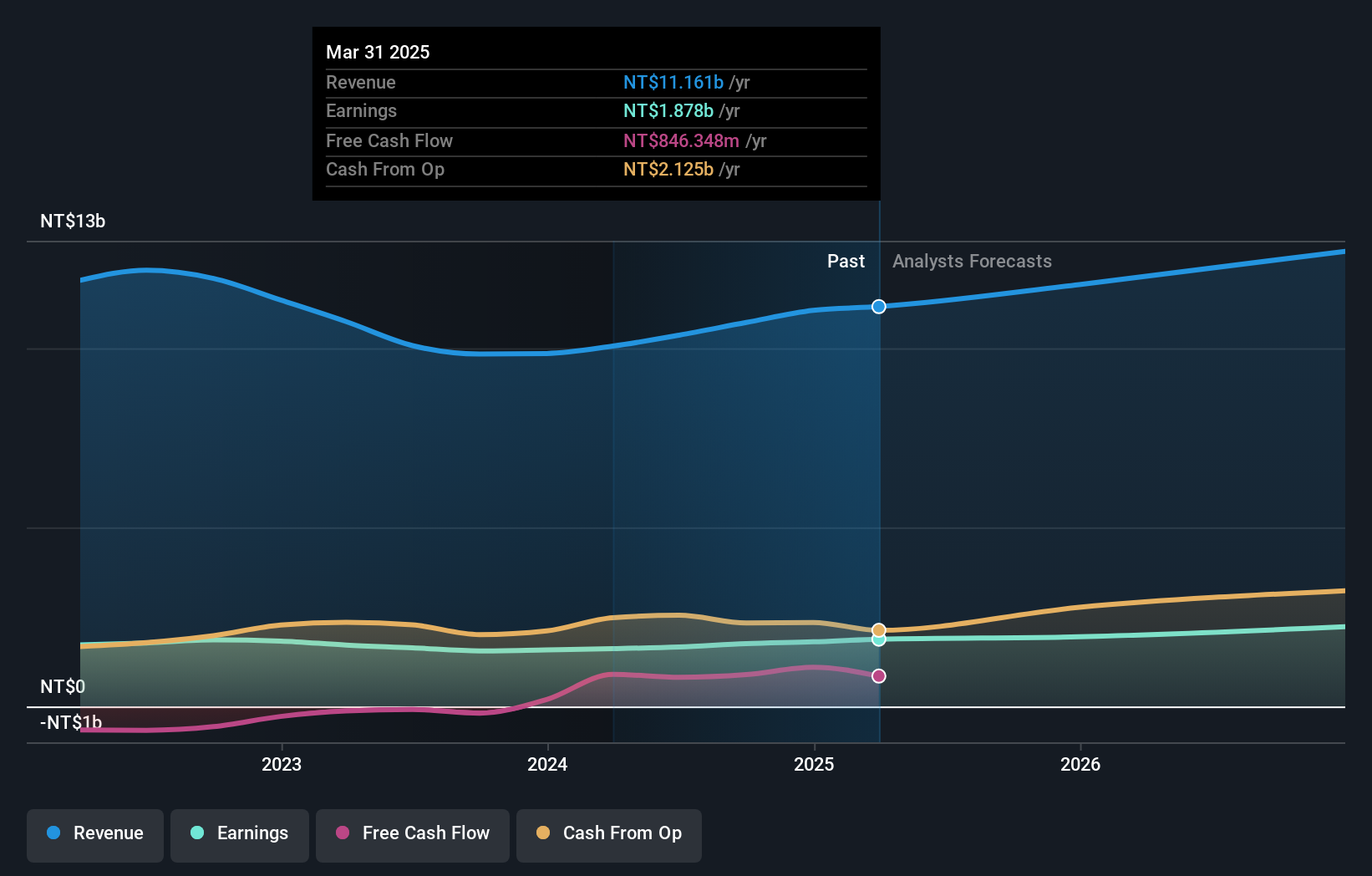

Shiny Chemical Industrial (TWSE:1773)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Shiny Chemical Industrial Co., Ltd. is involved in the manufacturing, processing, and trading of chemical solvents in Taiwan with a market capitalization of NT$39.88 billion.

Operations: Shiny Chemical Industrial's revenue primarily comes from its Yongan Factory, contributing NT$9.90 billion, followed by the Zhangbin Plant with NT$1.54 billion.

Shiny Chemical Industrial, a relatively small player in the chemicals sector, has seen its earnings grow at 11.9% annually over the past five years. Despite a high net debt to equity ratio of 40.8%, interest payments are well covered with an EBIT coverage of 45.5 times, indicating robust financial health. Recent reports show sales for Q3 at TWD 2,876 million and net income at TWD 478 million, both up from last year’s figures of TWD 2,522 million and TWD 388 million respectively. The company’s earnings per share increased to TWD 1.91 from TWD 1.55 year-on-year.

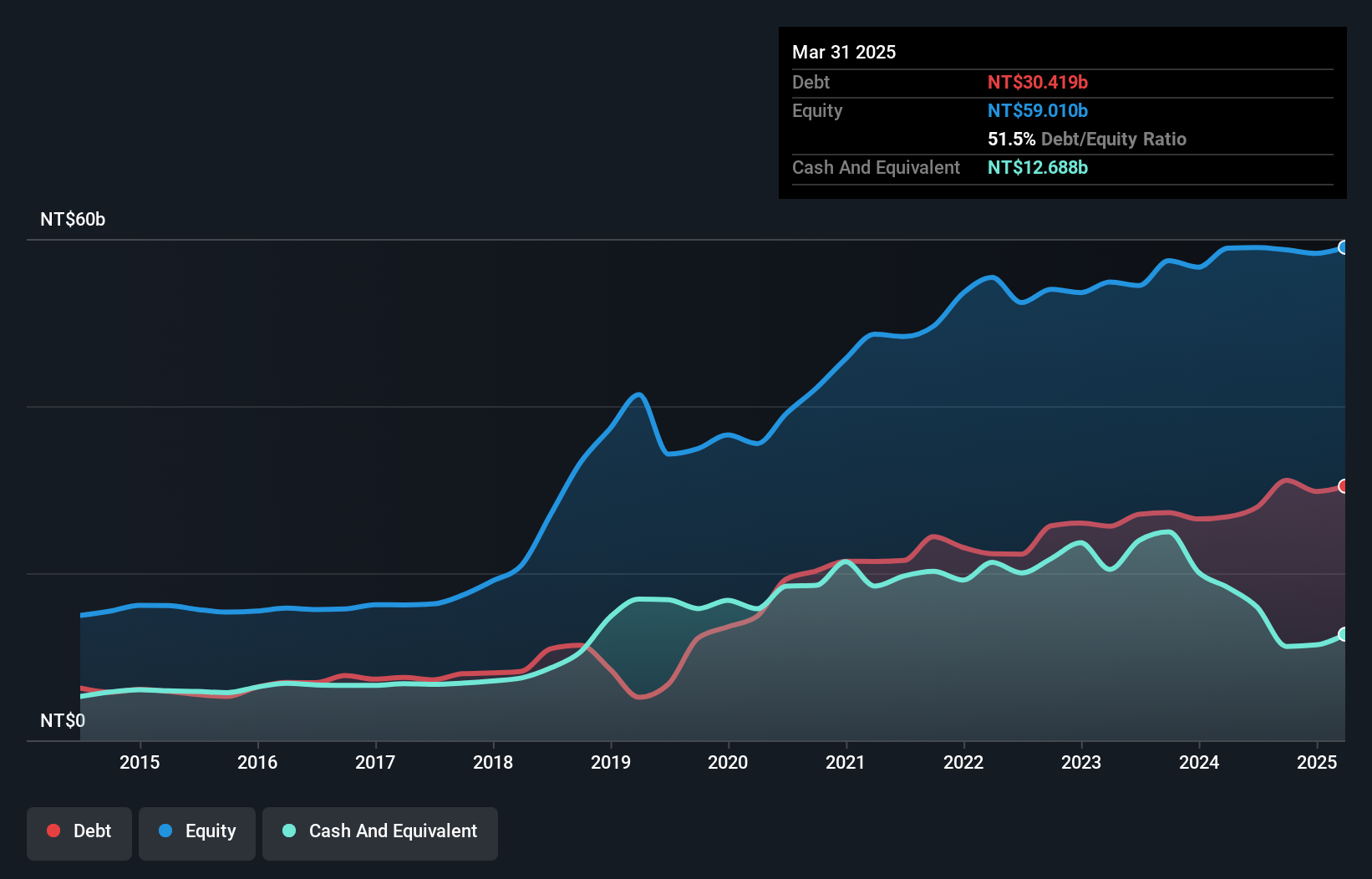

Walsin Technology (TWSE:2492)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Walsin Technology Corporation is engaged in the development, manufacturing, and sale of passive electronic components across Asia, America, and Europe with a market capitalization of NT$45.09 billion.

Operations: Walsin Technology generates revenue primarily from three segments, with Segment A contributing NT$23.86 billion and Segment C adding NT$7.30 billion. The company's financial performance is impacted by adjustments and write-offs amounting to -NT$2.51 billion.

Walsin Technology, a notable player in the electronics sector, has shown mixed results recently. Sales for Q3 2024 reached TWD 9.35 billion, up from TWD 8.69 billion the previous year, yet net income fell to TWD 445 million from TWD 1.06 billion. The company's basic earnings per share dropped to TWD 0.92 from TWD 2.19 year-on-year, reflecting challenges despite revenue growth over nine months totaling TWD 26.39 billion compared to last year's TWD 24.74 billion. With a satisfactory net debt-to-equity ratio of 33%, Walsin remains financially stable and continues to grow faster than its industry peers at a rate of approximately 10%.

- Click here to discover the nuances of Walsin Technology with our detailed analytical health report.

Assess Walsin Technology's past performance with our detailed historical performance reports.

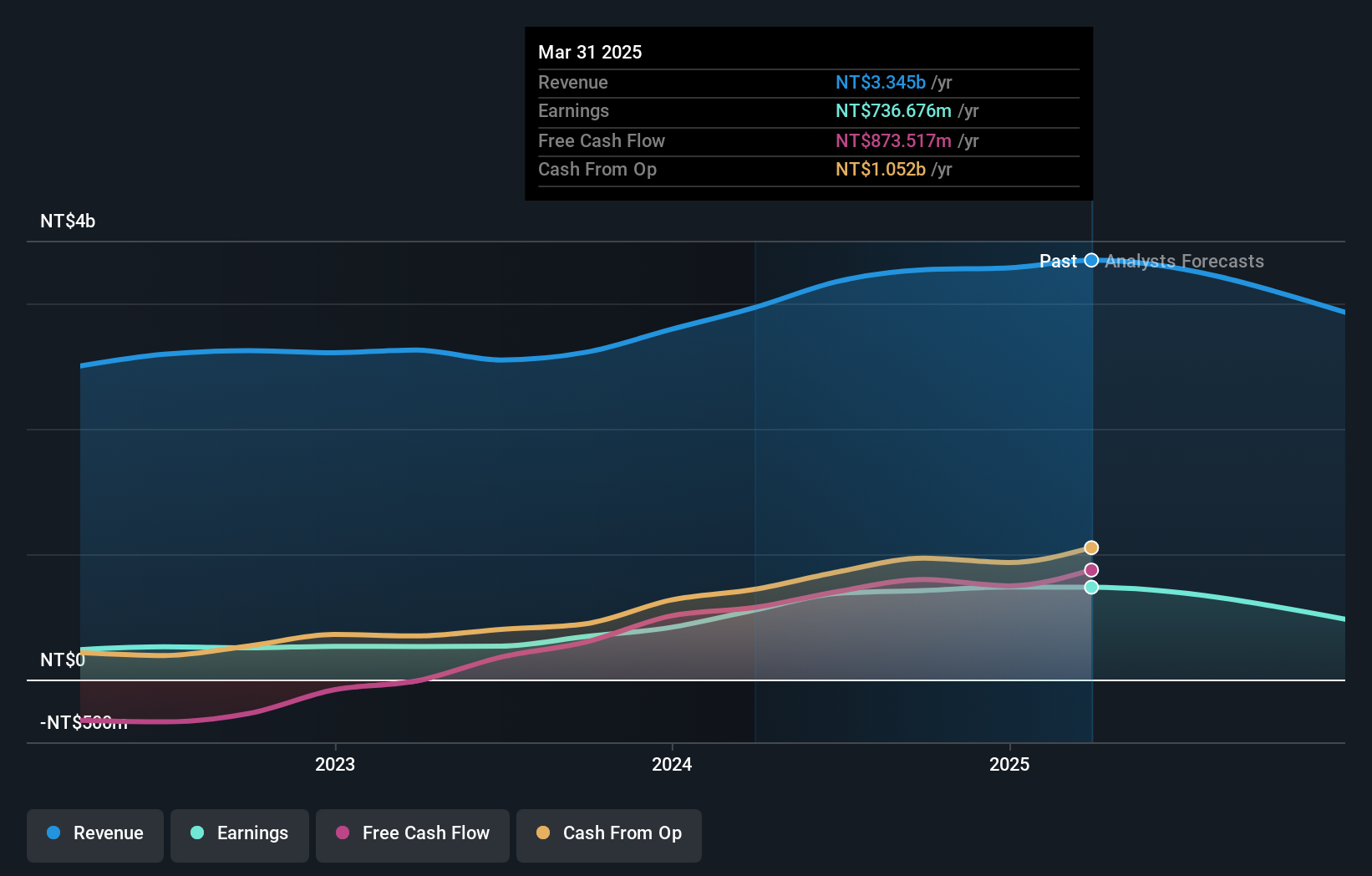

DingZing Advanced Materials (TWSE:6585)

Simply Wall St Value Rating: ★★★★★★

Overview: DingZing Advanced Materials Inc. engages in the research, development, production, and sale of composite materials and technical films for various industries in Taiwan with a market capitalization of NT$10.54 billion.

Operations: DingZing generates revenue primarily from its Specialty Chemicals segment, which accounts for NT$3.27 billion. The company's gross profit margin is a key financial metric to consider when evaluating its performance.

DingZing Advanced Materials, a company with promising potential, reported strong earnings growth of 106.9% over the past year, significantly outpacing the Chemicals industry average of 14.3%. With a satisfactory net debt to equity ratio at 5.2%, its financial health appears robust. The firm also boasts high-quality earnings and trades at a favorable price-to-earnings ratio of 14.8x compared to the TW market's 20.7x. Recent performance highlights include third-quarter sales reaching TWD 820 million and net income climbing to TWD 162 million, showcasing solid operational momentum in an evolving market landscape.

- Get an in-depth perspective on DingZing Advanced Materials' performance by reading our health report here.

Gain insights into DingZing Advanced Materials' past trends and performance with our Past report.

Taking Advantage

- Take a closer look at our Undiscovered Gems With Strong Fundamentals list of 4624 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6585

DingZing Advanced Materials

Researches, develops, produces, and sells composite materials, technical films, and other components for various industries in Taiwan.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor