Advertisement

As global markets edge toward record highs, buoyed by strong performances in major indices like the Nasdaq Composite and S&P 500, investors are closely watching inflation data that could influence future monetary policy decisions. In this dynamic environment, dividend stocks such as Komatsu offer a compelling option for those seeking steady income streams alongside potential capital appreciation.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Wuliangye YibinLtd (SZSE:000858) | 3.92% | ★★★★★★ |

| Chongqing Rural Commercial Bank (SEHK:3618) | 8.33% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.51% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.90% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.32% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 4.04% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 3.99% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.23% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.60% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 3.97% | ★★★★★★ |

Click here to see the full list of 1974 stocks from our Top Dividend Stocks screener.

Let's review some notable picks from our screened stocks.

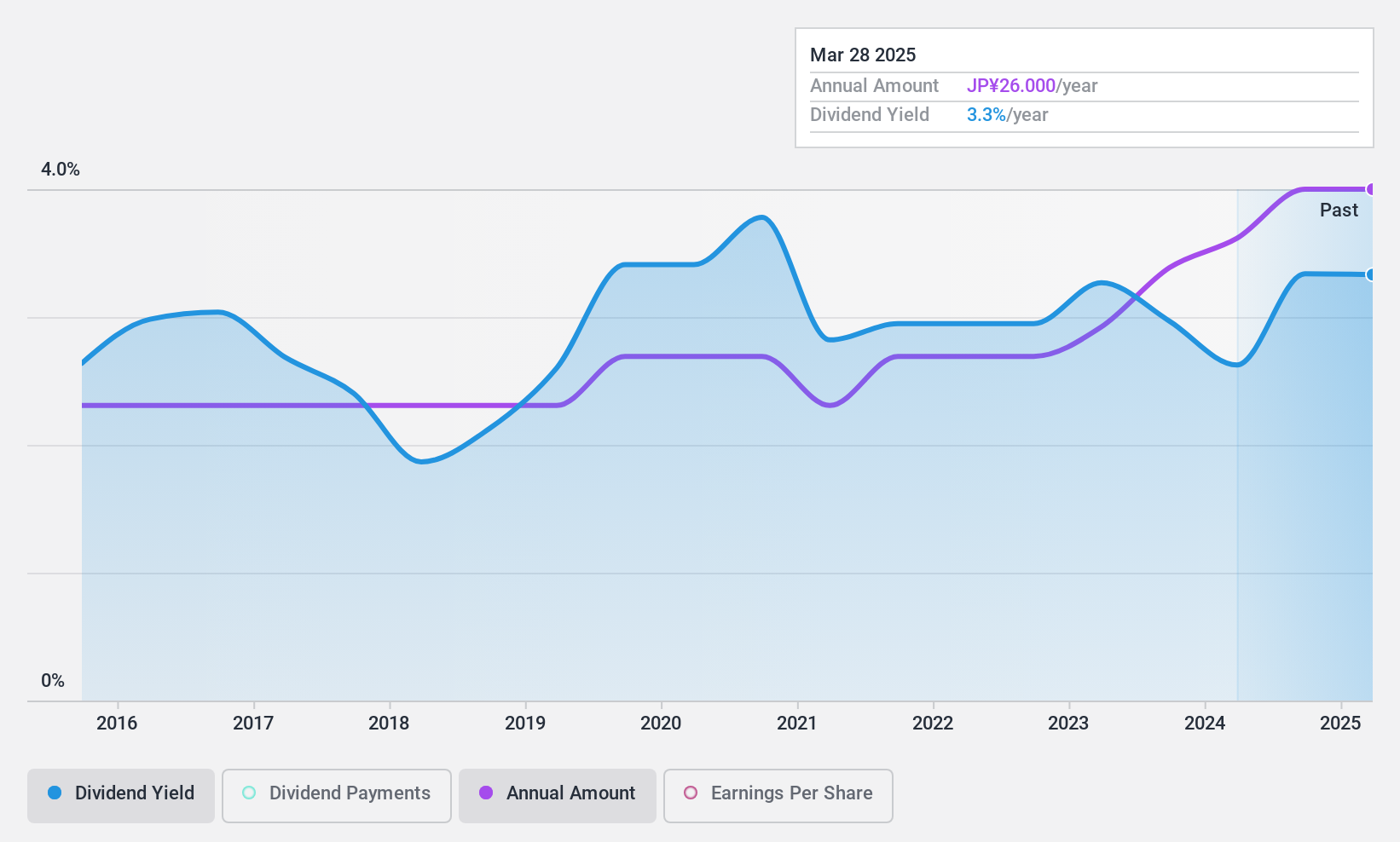

Komatsu (TSE:6301)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Komatsu Ltd. is a global manufacturer and seller of construction, mining, and utility equipment with operations spanning Japan, the Americas, Europe, China, the rest of Asia, Oceania, the Middle East, Africa, and CIS countries; it has a market cap of ¥4.37 trillion.

Operations: Komatsu Ltd.'s revenue is primarily derived from its construction, mining, and utility equipment segments across its global operations.

Dividend Yield: 3.5%

Komatsu's dividend yield of 3.53% is slightly below the top quartile in Japan, reflecting a modest appeal for income-focused investors. Despite trading at a significant discount to its estimated fair value, the company's dividends have been volatile over the past decade, indicating an unstable track record. However, with a low payout ratio of 22.2% and reasonable cash flow coverage at 54.5%, dividends are well-supported by earnings and cash flows, suggesting sustainability despite historical volatility.

- Navigate through the intricacies of Komatsu with our comprehensive dividend report here.

- According our valuation report, there's an indication that Komatsu's share price might be on the cheaper side.

Fukuvi Chemical IndustryLtd (TSE:7871)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Fukuvi Chemical Industry Co., Ltd. is engaged in the manufacturing and sale of plastic extrusion products for construction and industrial applications under the Fukuvi brand, both in Japan and internationally, with a market cap of ¥16.75 billion.

Operations: Fukuvi Chemical Industry Co., Ltd.'s revenue is derived from the production and distribution of plastic extrusion products for construction and industrial sectors, serving both domestic and international markets.

Dividend Yield: 3.1%

Fukuvi Chemical Industry's dividend yield of 3.1% is below the top quartile in Japan, offering limited appeal for high-yield seekers. Despite trading significantly below its estimated fair value, the company has a history of volatile dividends over the past decade. However, with low payout ratios—23.1% from earnings and 17.3% from cash flows—dividends are well-covered, indicating sustainability despite their unreliability and lack of consistent growth historically.

- Unlock comprehensive insights into our analysis of Fukuvi Chemical IndustryLtd stock in this dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Fukuvi Chemical IndustryLtd shares in the market.

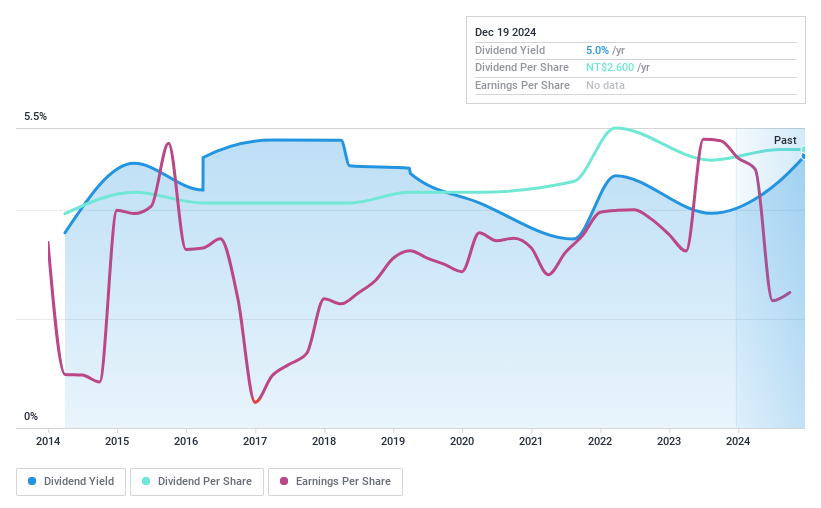

Taiwan Fertilizer (TWSE:1722)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Taiwan Fertilizer Co., Ltd. manufactures and sells inorganic and organic fertilizers, along with other chemical products, operating in Taiwan, the Middle East, and internationally, with a market cap of NT$51.45 billion.

Operations: Taiwan Fertilizer Co., Ltd.'s revenue is primarily derived from Chemical Fertilizers at NT$9.18 billion and its Property and Investment Business at NT$2.38 billion.

Dividend Yield: 5%

Taiwan Fertilizer's dividend yield of 4.95% ranks in the top quartile of the Taiwan market, yet its sustainability is questionable due to high payout ratios—147.9% from earnings and 95% from cash flows. Despite these concerns, dividends have been stable and growing over the past decade. Recent developments include a TWD 120.75 billion investment in an office building project, potentially impacting future cash flows and dividend coverage capabilities.

- Click to explore a detailed breakdown of our findings in Taiwan Fertilizer's dividend report.

- Our expertly prepared valuation report Taiwan Fertilizer implies its share price may be too high.

Seize The Opportunity

- Explore the 1974 names from our Top Dividend Stocks screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Taiwan Fertilizer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1722

Taiwan Fertilizer

Manufactures and sells inorganic and organic fertilizers, and other chemical products in Taiwan and internationally.

Adequate balance sheet with very low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

105 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

141 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative