Advertisement

Returns On Capital Are A Standout For Taita Chemical Company (TPE:1309)

What trends should we look for it we want to identify stocks that can multiply in value over the long term? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. So when we looked at the ROCE trend of Taita Chemical Company (TPE:1309) we really liked what we saw.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Taita Chemical Company:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.35 = NT$2.4b ÷ (NT$9.2b - NT$2.2b) (Based on the trailing twelve months to December 2020).

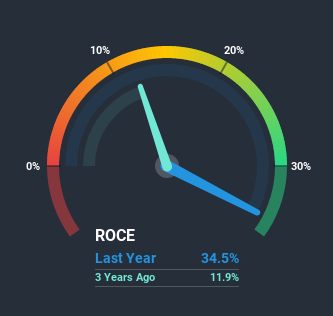

Therefore, Taita Chemical Company has an ROCE of 35%. That's a fantastic return and not only that, it outpaces the average of 7.7% earned by companies in a similar industry.

Check out our latest analysis for Taita Chemical Company

Above you can see how the current ROCE for Taita Chemical Company compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Taita Chemical Company.

What Can We Tell From Taita Chemical Company's ROCE Trend?

The trends we've noticed at Taita Chemical Company are quite reassuring. The data shows that returns on capital have increased substantially over the last five years to 35%. Basically the business is earning more per dollar of capital invested and in addition to that, 36% more capital is being employed now too. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

One more thing to note, Taita Chemical Company has decreased current liabilities to 23% of total assets over this period, which effectively reduces the amount of funding from suppliers or short-term creditors. So shareholders would be pleased that the growth in returns has mostly come from underlying business performance.

In Conclusion...

To sum it up, Taita Chemical Company has proven it can reinvest in the business and generate higher returns on that capital employed, which is terrific. And a remarkable 597% total return over the last five years tells us that investors are expecting more good things to come in the future. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

One final note, you should learn about the 3 warning signs we've spotted with Taita Chemical Company (including 1 which shouldn't be ignored) .

Taita Chemical Company is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

If you decide to trade Taita Chemical Company, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Taita Chemical Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1309

Taita Chemical Company

Engages in the production and sale of styrenics in Taiwan, Hong Kong, Mainland China, Southeastern/Central Asia, Europe, and North America.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.5% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.3% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.3% undervalued

AG

Community Contributor