Return Trends At Nan Ya Plastics (TPE:1303) Aren't Appealing

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after investigating Nan Ya Plastics (TPE:1303), we don't think it's current trends fit the mold of a multi-bagger.

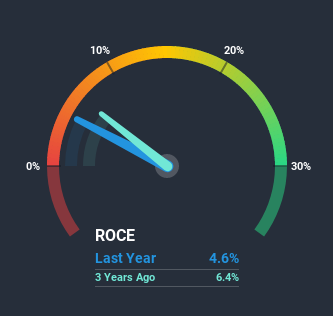

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Nan Ya Plastics is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.046 = NT$21b ÷ (NT$585b - NT$120b) (Based on the trailing twelve months to December 2020).

Therefore, Nan Ya Plastics has an ROCE of 4.6%. In absolute terms, that's a low return and it also under-performs the Chemicals industry average of 6.8%.

See our latest analysis for Nan Ya Plastics

Above you can see how the current ROCE for Nan Ya Plastics compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

What Does the ROCE Trend For Nan Ya Plastics Tell Us?

There hasn't been much to report for Nan Ya Plastics' returns and its level of capital employed because both metrics have been steady for the past five years. Businesses with these traits tend to be mature and steady operations because they're past the growth phase. With that in mind, unless investment picks up again in the future, we wouldn't expect Nan Ya Plastics to be a multi-bagger going forward. On top of that you'll notice that Nan Ya Plastics has been paying out a large portion (74%) of earnings in the form of dividends to shareholders. These mature businesses typically have reliable earnings and not many places to reinvest them, so the next best option is to put the earnings into shareholders pockets.

The Key Takeaway

We can conclude that in regards to Nan Ya Plastics' returns on capital employed and the trends, there isn't much change to report on. Since the stock has gained an impressive 48% over the last five years, investors must think there's better things to come. But if the trajectory of these underlying trends continue, we think the likelihood of it being a multi-bagger from here isn't high.

On a separate note, we've found 2 warning signs for Nan Ya Plastics you'll probably want to know about.

While Nan Ya Plastics isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

When trading Nan Ya Plastics or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Nan Ya Plastics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1303

Nan Ya Plastics

Engages in the manufacture and sale of plastic products, polyester fibers, petrochemical products, and electronic materials in Taiwan, China and Hong Kong, the United States, and internationally.

Moderate growth potential with mediocre balance sheet.