Advertisement

- Taiwan

- /

- Medical Equipment

- /

- TWSE:4736

Bullish: Analysts Just Made A Substantial Upgrade To Their TaiDoc Technology Corporation (GTSM:4736) Forecasts

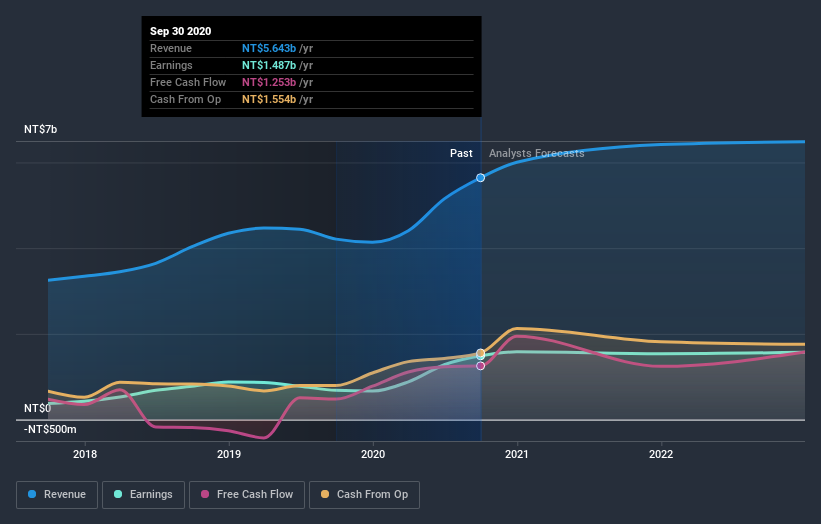

TaiDoc Technology Corporation (GTSM:4736) shareholders will have a reason to smile today, with the analysts making substantial upgrades to next year's statutory forecasts. The analysts greatly increased their revenue estimates, suggesting a stark improvement in business fundamentals.

After the upgrade, the four analysts covering TaiDoc Technology are now predicting revenues of NT$6.4b in 2021. If met, this would reflect a solid 14% improvement in sales compared to the last 12 months. Statutory earnings per share are supposed to decrease 2.8% to NT$16.60 in the same period. Prior to this update, the analysts had been forecasting revenues of NT$5.7b and earnings per share (EPS) of NT$13.31 in 2021. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

View our latest analysis for TaiDoc Technology

It will come as no surprise to learn that the analysts have increased their price target for TaiDoc Technology 10% to NT$264 on the back of these upgrades. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic TaiDoc Technology analyst has a price target of NT$295 per share, while the most pessimistic values it at NT$213. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await TaiDoc Technology shareholders.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We can infer from the latest estimates that forecasts expect a continuation of TaiDoc Technology'shistorical trends, as next year's 14% revenue growth is roughly in line with 14% annual revenue growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 21% per year. So it's pretty clear that TaiDoc Technology is expected to grow slower than similar companies in the same industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for next year. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. Given that the consensus looks almost universally bullish, with a substantial increase to forecasts and a higher price target, TaiDoc Technology could be worth investigating further.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple TaiDoc Technology analysts - going out to 2022, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade TaiDoc Technology, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if TaiDoc Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TWSE:4736

TaiDoc Technology

Manufactures and markets medical devices in Taiwan and internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor