Advertisement

These 4 Measures Indicate That Formosa Oilseed Processing (TWSE:1225) Is Using Debt Reasonably Well

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Formosa Oilseed Processing Co., Ltd. (TWSE:1225) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Formosa Oilseed Processing

How Much Debt Does Formosa Oilseed Processing Carry?

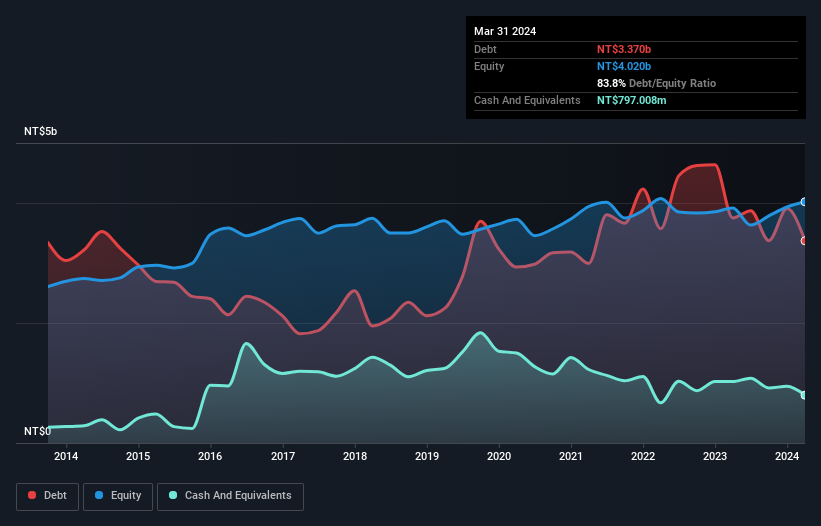

You can click the graphic below for the historical numbers, but it shows that Formosa Oilseed Processing had NT$3.37b of debt in March 2024, down from NT$3.75b, one year before. However, it also had NT$797.0m in cash, and so its net debt is NT$2.57b.

How Strong Is Formosa Oilseed Processing's Balance Sheet?

The latest balance sheet data shows that Formosa Oilseed Processing had liabilities of NT$2.65b due within a year, and liabilities of NT$1.53b falling due after that. Offsetting this, it had NT$797.0m in cash and NT$1.95b in receivables that were due within 12 months. So its liabilities total NT$1.43b more than the combination of its cash and short-term receivables.

Since publicly traded Formosa Oilseed Processing shares are worth a total of NT$33.0b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Formosa Oilseed Processing has a debt to EBITDA ratio of 4.3 and its EBIT covered its interest expense 6.5 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Pleasingly, Formosa Oilseed Processing is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 147% gain in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Formosa Oilseed Processing will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Formosa Oilseed Processing created free cash flow amounting to 16% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

When it comes to the balance sheet, the standout positive for Formosa Oilseed Processing was the fact that it seems able to grow its EBIT confidently. But the other factors we noted above weren't so encouraging. For example, its net debt to EBITDA makes us a little nervous about its debt. When we consider all the elements mentioned above, it seems to us that Formosa Oilseed Processing is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Formosa Oilseed Processing you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1225

Formosa Oilseed Processing

Produces and sells oil and feed products in China.

Flawless balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor