Advertisement

Are Formosa Oilseed Processing's (TPE:1225) Statutory Earnings A Good Guide To Its Underlying Profitability?

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. This article will consider whether Formosa Oilseed Processing's (TPE:1225) statutory profits are a good guide to its underlying earnings.

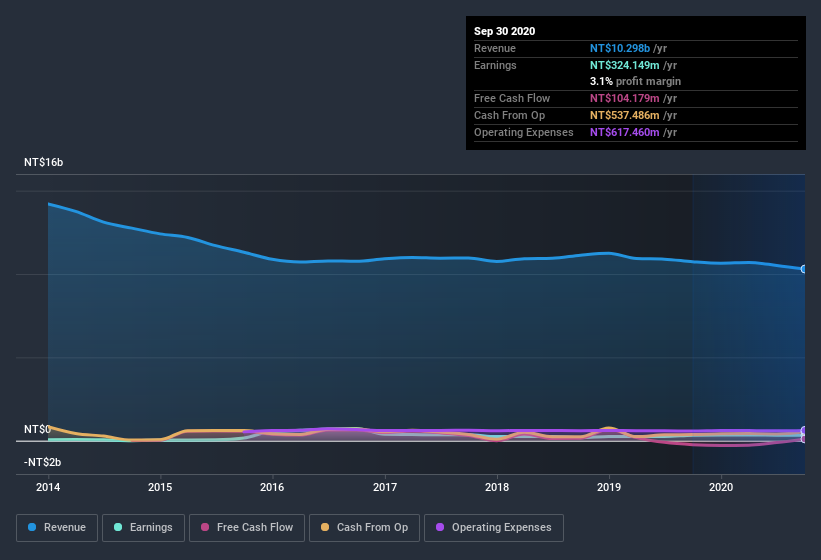

We like the fact that Formosa Oilseed Processing made a profit of NT$324.1m on its revenue of NT$10.3b, in the last year. In the last few years both its revenue and its profit have fallen, as you can see in the chart below.

See our latest analysis for Formosa Oilseed Processing

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. This article will discuss how unusual items have impacted Formosa Oilseed Processing's most recent profit results. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Formosa Oilseed Processing.

The Impact Of Unusual Items On Profit

For anyone who wants to understand Formosa Oilseed Processing's profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit gained from NT$59m worth of unusual items. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. And that's as you'd expect, given these boosts are described as 'unusual'. If Formosa Oilseed Processing doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Formosa Oilseed Processing's Profit Performance

Arguably, Formosa Oilseed Processing's statutory earnings have been distorted by unusual items boosting profit. Therefore, it seems possible to us that Formosa Oilseed Processing's true underlying earnings power is actually less than its statutory profit. Sadly, its EPS was down over the last twelve months. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example, Formosa Oilseed Processing has 3 warning signs (and 2 which can't be ignored) we think you should know about.

This note has only looked at a single factor that sheds light on the nature of Formosa Oilseed Processing's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you decide to trade Formosa Oilseed Processing, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1225

Formosa Oilseed Processing

Produces and sells oil and feed products in China.

Flawless balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor