- Taiwan

- /

- Consumer Durables

- /

- TWSE:9911

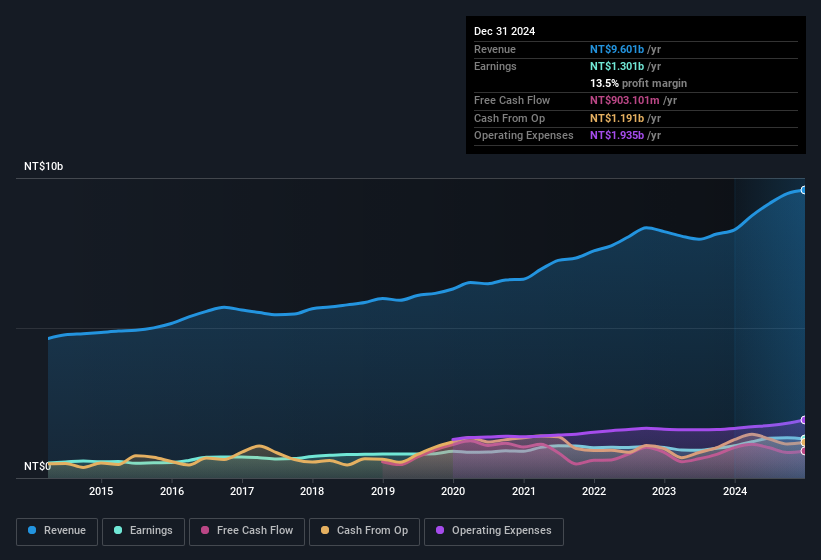

Taiwan Sakura Full Year 2024 Earnings: EPS: NT$5.94 (vs NT$4.90 in FY 2023)

Taiwan Sakura (TWSE:9911) Full Year 2024 Results

Key Financial Results

- Revenue: NT$9.60b (up 16% from FY 2023).

- Net income: NT$1.30b (up 21% from FY 2023).

- Profit margin: 14% (in line with FY 2023).

- EPS: NT$5.94 (up from NT$4.90 in FY 2023).

All figures shown in the chart above are for the trailing 12 month (TTM) period

Taiwan Sakura shares are up 1.0% from a week ago.

Risk Analysis

You should learn about the 1 warning sign we've spotted with Taiwan Sakura.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Taiwan Sakura might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:9911

Taiwan Sakura

Manufactures and sells kitchen appliances in Taiwan, China, Hong Kong, Vietnam, and internationally.

Excellent balance sheet established dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion