Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Thunder Tiger Corp. (TWSE:8033) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Thunder Tiger

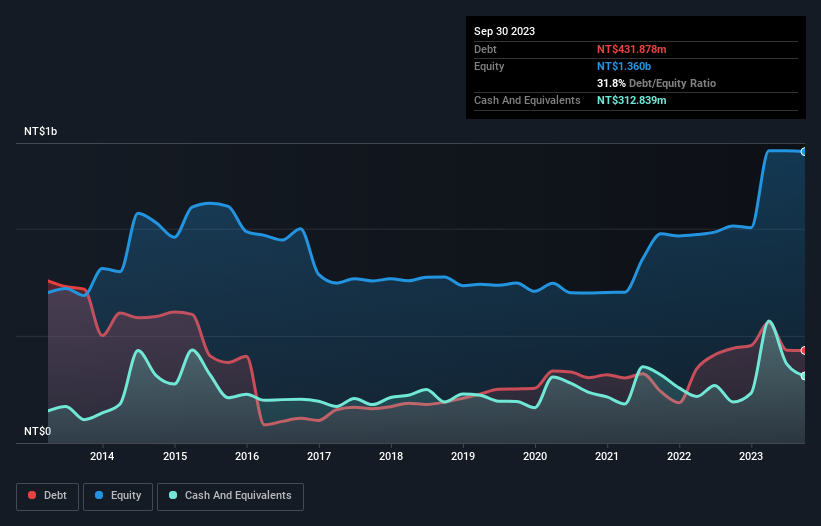

What Is Thunder Tiger's Net Debt?

The chart below, which you can click on for greater detail, shows that Thunder Tiger had NT$431.9m in debt in September 2023; about the same as the year before. However, it also had NT$312.8m in cash, and so its net debt is NT$119.0m.

How Strong Is Thunder Tiger's Balance Sheet?

The latest balance sheet data shows that Thunder Tiger had liabilities of NT$455.9m due within a year, and liabilities of NT$177.4m falling due after that. Offsetting these obligations, it had cash of NT$312.8m as well as receivables valued at NT$185.5m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by NT$134.9m.

Having regard to Thunder Tiger's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the NT$8.00b company is struggling for cash, we still think it's worth monitoring its balance sheet. Carrying virtually no net debt, Thunder Tiger has a very light debt load indeed. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Thunder Tiger's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Thunder Tiger made a loss at the EBIT level, and saw its revenue drop to NT$1.0b, which is a fall of 3.6%. We would much prefer see growth.

Caveat Emptor

Over the last twelve months Thunder Tiger produced an earnings before interest and tax (EBIT) loss. Indeed, it lost NT$40m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through NT$255m of cash over the last year. So to be blunt we think it is risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 1 warning sign for Thunder Tiger that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Thunder Tiger might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:8033

Thunder Tiger

Manufactures and sells remote-controlled planes, helicopters, cars, boats, engine parts, and medical devices in Taiwan, the Americas, and internationally.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor