Advertisement

- Taiwan

- /

- Consumer Durables

- /

- TWSE:2488

Is The Market Rewarding Hanpin Electron Co., Ltd. (TPE:2488) With A Negative Sentiment As A Result Of Its Mixed Fundamentals?

Hanpin Electron (TPE:2488) has had a rough week with its share price down 2.8%. We, however decided to study the company's financials to determine if they have got anything to do with the price decline. Long-term fundamentals are usually what drive market outcomes, so it's worth paying close attention. Particularly, we will be paying attention to Hanpin Electron's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

Check out our latest analysis for Hanpin Electron

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Hanpin Electron is:

9.5% = NT$193m ÷ NT$2.0b (Based on the trailing twelve months to September 2020).

The 'return' is the amount earned after tax over the last twelve months. So, this means that for every NT$1 of its shareholder's investments, the company generates a profit of NT$0.10.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Hanpin Electron's Earnings Growth And 9.5% ROE

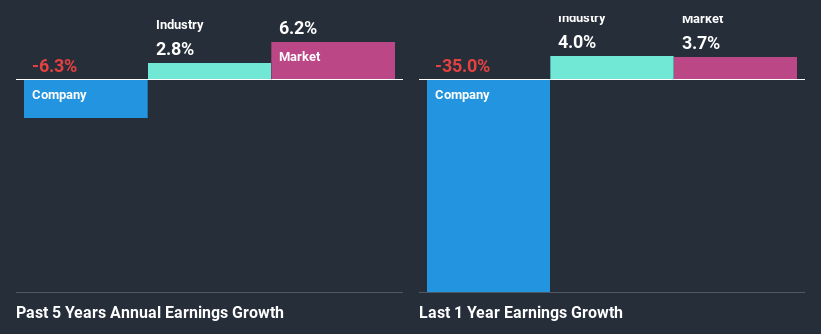

To begin with, Hanpin Electron seems to have a respectable ROE. Even so, when compared with the average industry ROE of 13%, we aren't very excited. Moreover, Hanpin Electron's net income shrunk at a rate of 6.3%over the past five years. Bear in mind, the company does have a high ROE. It is just that the industry ROE is higher. Hence there might be some other aspects that are causing earnings to shrink. These include low earnings retention or poor allocation of capital.

That being said, we compared Hanpin Electron's performance with the industry and were concerned when we found that while the company has shrunk its earnings, the industry has grown its earnings at a rate of 2.8% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about Hanpin Electron's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Hanpin Electron Making Efficient Use Of Its Profits?

Hanpin Electron's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 73% (or a retention ratio of 27%). The business is only left with a small pool of capital to reinvest - A vicious cycle that doesn't benefit the company in the long-run. Our risks dashboard should have the 3 risks we have identified for Hanpin Electron.

In addition, Hanpin Electron has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth.

Conclusion

Overall, we have mixed feelings about Hanpin Electron. On the one hand, the company does have a decent rate of return, however, its earnings growth number is quite disappointing and as discussed earlier, the low retained earnings is hampering the growth. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. To gain further insights into Hanpin Electron's past profit growth, check out this visualization of past earnings, revenue and cash flows.

If you’re looking to trade Hanpin Electron, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hanpin Electron might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:2488

Hanpin Electron

Designs, manufactures, and sells electronic consumer products, professional audio products, and professional DJ equipment in Taiwan, China, Hong Kong, and Singapore.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor