Advertisement

We Think KMC (Kuei Meng) International (GTSM:5306) Can Manage Its Debt With Ease

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that KMC (Kuei Meng) International Inc. (GTSM:5306) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for KMC (Kuei Meng) International

How Much Debt Does KMC (Kuei Meng) International Carry?

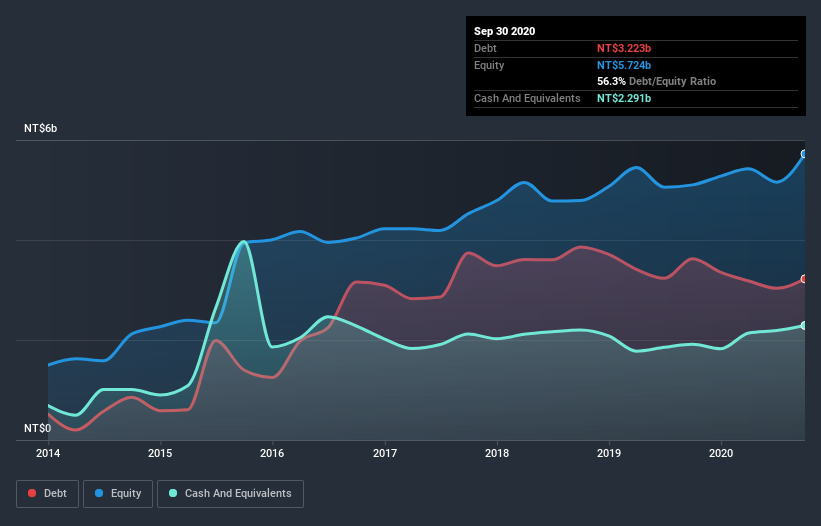

As you can see below, KMC (Kuei Meng) International had NT$3.22b of debt at September 2020, down from NT$3.62b a year prior. However, it does have NT$2.29b in cash offsetting this, leading to net debt of about NT$932.1m.

A Look At KMC (Kuei Meng) International's Liabilities

We can see from the most recent balance sheet that KMC (Kuei Meng) International had liabilities of NT$2.18b falling due within a year, and liabilities of NT$2.49b due beyond that. Offsetting this, it had NT$2.29b in cash and NT$1.37b in receivables that were due within 12 months. So it has liabilities totalling NT$1.02b more than its cash and near-term receivables, combined.

Given KMC (Kuei Meng) International has a market capitalization of NT$24.1b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

KMC (Kuei Meng) International's net debt is only 0.47 times its EBITDA. And its EBIT covers its interest expense a whopping 254 times over. So we're pretty relaxed about its super-conservative use of debt. Also positive, KMC (Kuei Meng) International grew its EBIT by 27% in the last year, and that should make it easier to pay down debt, going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine KMC (Kuei Meng) International's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, KMC (Kuei Meng) International recorded free cash flow worth 79% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

KMC (Kuei Meng) International's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And that's just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. We think KMC (Kuei Meng) International is no more beholden to its lenders, than the birds are to birdwatchers. To our minds it has a healthy happy balance sheet. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for KMC (Kuei Meng) International that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade KMC (Kuei Meng) International, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if KMC (Kuei Meng) International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TWSE:5306

KMC (Kuei Meng) International

Manufactures and sells various types of chains, motorcycle components, and vehicle components in Asia, Europe, and the United States.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor