Advertisement

- Taiwan

- /

- Commercial Services

- /

- TPEX:8423

Are Polygreen Resources Co., Ltd.'s (GTSM:8423) Fundamentals Good Enough to Warrant Buying Given The Stock's Recent Weakness?

With its stock down 3.3% over the past three months, it is easy to disregard Polygreen Resources (GTSM:8423). However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. Particularly, we will be paying attention to Polygreen Resources' ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

Check out our latest analysis for Polygreen Resources

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Polygreen Resources is:

5.4% = NT$18m ÷ NT$331m (Based on the trailing twelve months to September 2020).

The 'return' is the profit over the last twelve months. Another way to think of that is that for every NT$1 worth of equity, the company was able to earn NT$0.05 in profit.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Polygreen Resources' Earnings Growth And 5.4% ROE

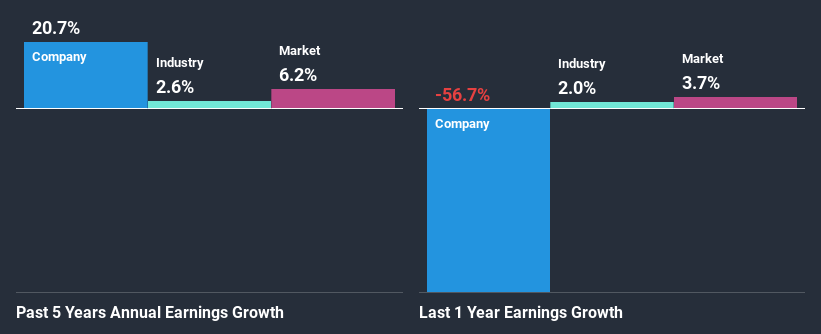

At first glance, Polygreen Resources' ROE doesn't look very promising. However, its ROE is similar to the industry average of 5.6%, so we won't completely dismiss the company. Particularly, the exceptional 21% net income growth seen by Polygreen Resources over the past five years is pretty remarkable. Given the slightly low ROE, it is likely that there could be some other aspects that are driving this growth. For instance, the company has a low payout ratio or is being managed efficiently.

We then compared Polygreen Resources' net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 2.6% in the same period.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. Has the market priced in the future outlook for 8423? You can find out in our latest intrinsic value infographic research report

Is Polygreen Resources Using Its Retained Earnings Effectively?

Polygreen Resources has a three-year median payout ratio of 48% (where it is retaining 52% of its income) which is not too low or not too high. By the looks of it, the dividend is well covered and Polygreen Resources is reinvesting its profits efficiently as evidenced by its exceptional growth which we discussed above.

Besides, Polygreen Resources has been paying dividends over a period of seven years. This shows that the company is committed to sharing profits with its shareholders.

Conclusion

Overall, we feel that Polygreen Resources certainly does have some positive factors to consider. With a high rate of reinvestment, albeit at a low ROE, the company has managed to see a considerable growth in its earnings. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. You can see the 4 risks we have identified for Polygreen Resources by visiting our risks dashboard for free on our platform here.

If you’re looking to trade Polygreen Resources, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:8423

Polygreen Resources

An investment holding company, engages in resource recycling and environmental protection business in Taiwan, Japan, China, Philippines, Vietnam, Indonesia, the Middle East, Singapore, and internationally.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor