As global markets experience a resurgence with key indices like the Dow Jones and S&P 500 reaching record highs, investor sentiment has been buoyed by moderating inflation and favorable economic indicators. In such an environment, growth companies with high insider ownership can be particularly intriguing to watch, as these insiders may have significant confidence in their firms' prospects amidst current market dynamics.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

| Modetour Network (KOSDAQ:A080160) | 12.3% | 45.6% |

| Cettire (ASX:CTT) | 28.7% | 29.9% |

| Gaming Innovation Group (OB:GIG) | 22.8% | 36.2% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 24.5% |

| Vow (OB:VOW) | 31.8% | 99.3% |

| UTI (KOSDAQ:A179900) | 34.2% | 111.6% |

| EHang Holdings (NasdaqGM:EH) | 33% | 98.2% |

| Seojin SystemLtd (KOSDAQ:A178320) | 26.9% | 48.1% |

| Adocia (ENXTPA:ADOC) | 12.8% | 104.5% |

We'll examine a selection from our screener results.

Merdeka Copper Gold (IDX:MDKA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PT Merdeka Copper Gold Tbk operates in the mining sector within Indonesia, with a market capitalization of approximately IDR 68.83 billion.

Operations: The company's revenue is primarily derived from its Battery Materials segment, generating $1.33 billion, followed by the Tujuh Bukit Project at $261.76 million and the Wetar Project at $114.55 million.

Insider Ownership: 11.1%

Revenue Growth Forecast: 18.3% p.a.

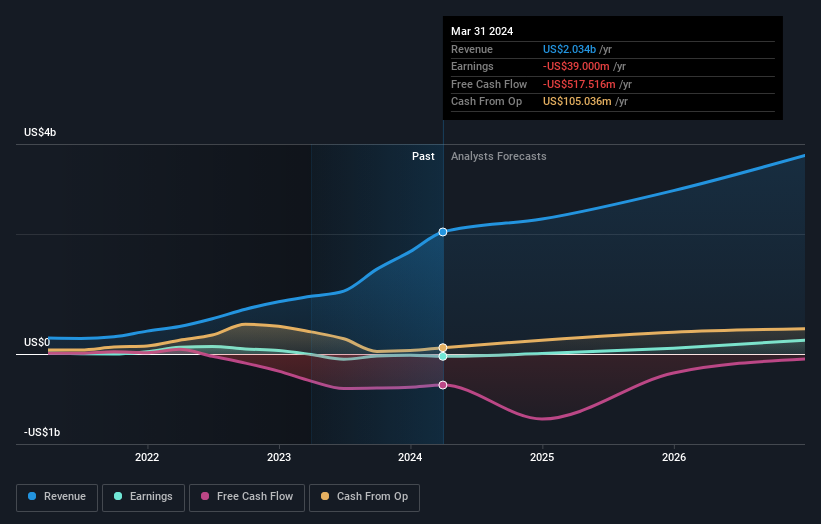

Merdeka Copper Gold's recent performance shows a significant shift with sales reaching US$1.71 billion, up from US$869.88 million, despite a swing to a net loss of US$20.66 million from a previous net profit of US$58.42 million. The company has also engaged in substantial capital raising activities, completing an equity offering for IDR 785.10 billion at IDR 2168 per share. Forecasted revenue growth at 18.3% annually outpaces the Indonesian market's 10.6%, with profitability expected within three years, although current return on equity projections remain modest at 17%.

- Delve into the full analysis future growth report here for a deeper understanding of Merdeka Copper Gold.

- Our comprehensive valuation report raises the possibility that Merdeka Copper Gold is priced higher than what may be justified by its financials.

Shin Zu Shing (TWSE:3376)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Shin Zu Shing Co., Ltd. is a company based in Taiwan that specializes in the production and sale of precision springs, stamping parts, hinge components, CNC lathes, and metal injection molding, with operations extending to Singapore and China. The company has a market capitalization of approximately NT$37.83 billion.

Operations: Shin Zu Shing's revenue is derived from the production and sale of precision springs, stamping parts, hinge components, CNC lathes, and metal injection molding across Taiwan, Singapore, and China.

Insider Ownership: 24%

Revenue Growth Forecast: 17.6% p.a.

Shin Zu Shing has demonstrated robust growth with its recent Q1 earnings more than doubling year-over-year, reflecting a significant increase in sales and net income. Despite this, the company's profit margins have declined from the previous year, and its share price remains highly volatile. Looking ahead, Shin Zu Shing is expected to see substantial earnings growth at 26.55% annually over the next three years, outpacing broader market forecasts. However, its dividend coverage is weak, indicating potential challenges in sustaining payouts amidst rapid expansion.

- Unlock comprehensive insights into our analysis of Shin Zu Shing stock in this growth report.

- Upon reviewing our latest valuation report, Shin Zu Shing's share price might be too optimistic.

Kaori Heat Treatment (TWSE:8996)

Simply Wall St Growth Rating: ★★★★★★

Overview: Kaori Heat Treatment Co., Ltd. is a company based in Taiwan that specializes in developing, manufacturing, and selling heat exchanger solutions across Asia, the United States, Europe, and other international markets, with a market capitalization of NT$42.73 billion.

Operations: The firm specializes in producing and distributing heat exchanger solutions, serving markets across Asia, the United States, Europe, and globally.

Insider Ownership: 12.7%

Revenue Growth Forecast: 31.8% p.a.

Kaori Heat Treatment Co., Ltd. is set to outperform with a forecasted annual revenue growth of 31.8% and earnings expected to increase by 37.6% per year, both metrics surpassing the broader Taiwanese market projections. Despite its highly volatile share price recently, the company's return on equity is anticipated to be strong at 38% in three years. Additionally, Kaori has established a Sustainable Development Committee, enhancing its governance framework which may appeal to socially conscious investors.

- Click here and access our complete growth analysis report to understand the dynamics of Kaori Heat Treatment.

- Our valuation report here indicates Kaori Heat Treatment may be overvalued.

Turning Ideas Into Actions

- Dive into all 1500 of the Fast Growing Companies With High Insider Ownership we have identified here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Kaori Heat Treatment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:8996

Kaori Heat Treatment

Engages in the research, development, manufacture, and sale of heat exchanger solutions in Taiwan, rest of Asia, the United States, Europe, and internationally.

Exceptional growth potential with excellent balance sheet.