Advertisement

Broker Revenue Forecasts For Shin Zu Shing Co., Ltd. (TWSE:3376) Are Surging Higher

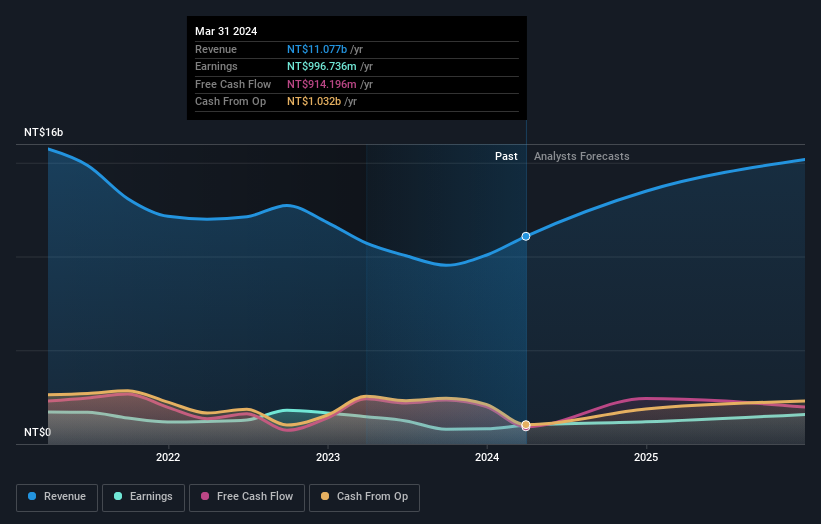

Shin Zu Shing Co., Ltd. (TWSE:3376) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The revenue forecast for this year has experienced a facelift, with the analysts now much more optimistic on its sales pipeline. Shin Zu Shing has also found favour with investors, with the stock up a noteworthy 14% to NT$207 over the past week. It will be interesting to see if today's upgrade is enough to propel the stock even higher.

Following the upgrade, the most recent consensus for Shin Zu Shing from its four analysts is for revenues of NT$13b in 2024 which, if met, would be a huge 22% increase on its sales over the past 12 months. Statutory earnings per share are presumed to grow 19% to NT$6.30. Before this latest update, the analysts had been forecasting revenues of NT$12b and earnings per share (EPS) of NT$6.35 in 2024. It seems analyst sentiment has certainly become more bullish on revenues, even though they haven't changed their view on earnings per share.

View our latest analysis for Shin Zu Shing

Analysts increased their price target 20% to NT$219, perhaps signalling that higher revenues are a strong leading indicator for Shin Zu Shing's valuation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. One thing stands out from these estimates, which is that Shin Zu Shing is forecast to grow faster in the future than it has in the past, with revenues expected to display 30% annualised growth until the end of 2024. If achieved, this would be a much better result than the 2.5% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 14% per year. So it looks like Shin Zu Shing is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with analysts reconfirming that earnings per share are expected to continue performing in line with their prior expectations. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. There was also a nice increase in the price target, with analysts apparently feeling that the intrinsic value of the business is improving. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Shin Zu Shing.

These earnings upgrades look like a sterling endorsement, but before diving in - you should know that we've spotted 3 potential flags with Shin Zu Shing, including its declining profit margins. For more information, you can click through to our platform to learn more about this and the 2 other flags we've identified .

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:3376

Shin Zu Shing

Engages in the research, design, development, production, assembly, testing, manufacturing, and trading of various precision springs, stamping parts, hinge components, CNC lathes, and metal injection molding in Taiwan, Singapore, and China.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor