Advertisement

- Taiwan

- /

- Auto Components

- /

- TPEX:1586

Is China Fineblanking TechnologyLtd (GTSM:1586) Using Too Much Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that China Fineblanking Technology Co.,Ltd. (GTSM:1586) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for China Fineblanking TechnologyLtd

What Is China Fineblanking TechnologyLtd's Debt?

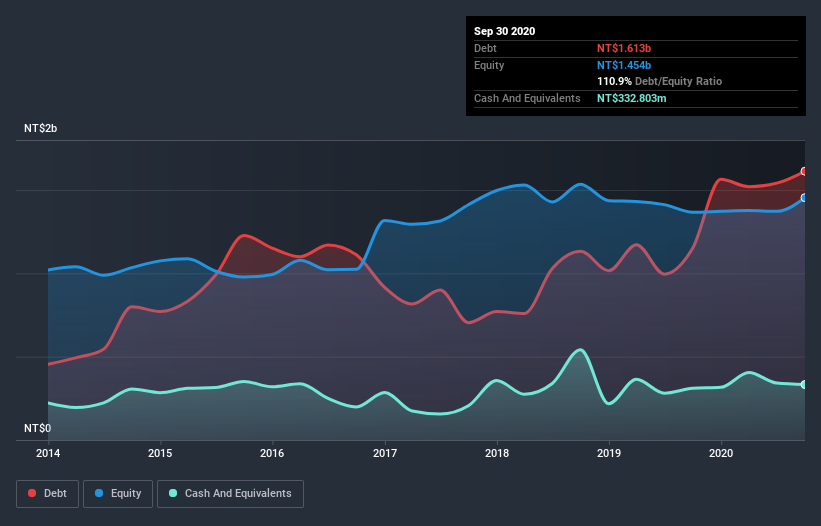

As you can see below, at the end of September 2020, China Fineblanking TechnologyLtd had NT$1.61b of debt, up from NT$1.15b a year ago. Click the image for more detail. However, it does have NT$332.8m in cash offsetting this, leading to net debt of about NT$1.28b.

A Look At China Fineblanking TechnologyLtd's Liabilities

Zooming in on the latest balance sheet data, we can see that China Fineblanking TechnologyLtd had liabilities of NT$1.21b due within 12 months and liabilities of NT$1.13b due beyond that. Offsetting these obligations, it had cash of NT$332.8m as well as receivables valued at NT$737.7m due within 12 months. So its liabilities total NT$1.27b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since China Fineblanking TechnologyLtd has a market capitalization of NT$3.30b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt to EBITDA of 3.5 China Fineblanking TechnologyLtd has a fairly noticeable amount of debt. On the plus side, its EBIT was 7.0 times its interest expense, and its net debt to EBITDA, was quite high, at 3.5. Pleasingly, China Fineblanking TechnologyLtd is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 871% gain in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is China Fineblanking TechnologyLtd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, China Fineblanking TechnologyLtd saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Neither China Fineblanking TechnologyLtd's ability to convert EBIT to free cash flow nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But the good news is it seems to be able to grow its EBIT with ease. Looking at all the angles mentioned above, it does seem to us that China Fineblanking TechnologyLtd is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with China Fineblanking TechnologyLtd , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade China Fineblanking TechnologyLtd, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:1586

China Fineblanking TechnologyLtd

Manufactures and sells computer hard drives, automobiles, and metal parts in Taiwan and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor