- Taiwan

- /

- Auto Components

- /

- TWSE:4557

Yusin Holding (TWSE:4557) Will Pay A Smaller Dividend Than Last Year

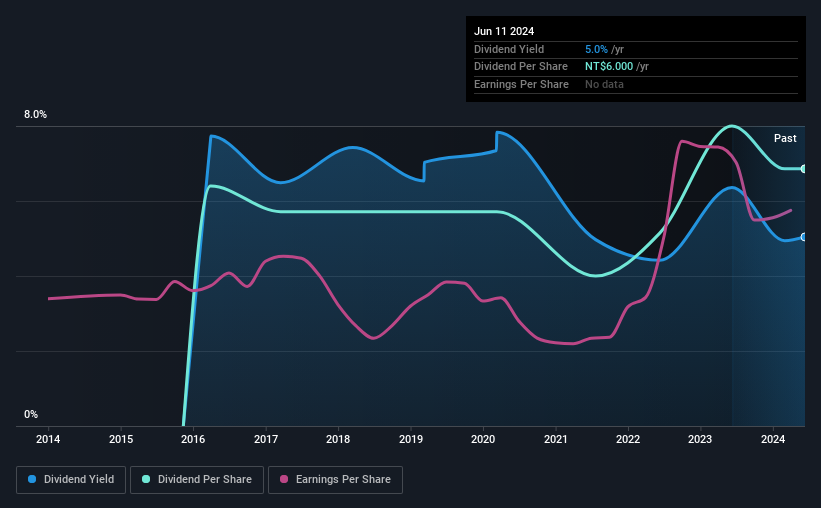

Yusin Holding Corp. (TWSE:4557) has announced that on 17th of July, it will be paying a dividend ofNT$6.00, which a reduction from last year's comparable dividend. However, the dividend yield of 5.0% is still a decent boost to shareholder returns.

Check out our latest analysis for Yusin Holding

Yusin Holding's Payment Has Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much. Before making this announcement, Yusin Holding was earning enough to cover the dividend, but it wasn't generating any free cash flows. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

If the trend of the last few years continues, EPS will grow by 10.4% over the next 12 months. Assuming the dividend continues along recent trends, we think the payout ratio could be 62% by next year, which is in a pretty sustainable range.

Yusin Holding's Dividend Has Lacked Consistency

Yusin Holding has been paying dividends for a while, but the track record isn't stellar. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2016, the dividend has gone from NT$5.60 total annually to NT$6.00. Dividend payments have grown at less than 1% a year over this period. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Yusin Holding has seen EPS rising for the last five years, at 10% per annum. The lack of cash flows does make us a bit cautious though, especially when it comes to the future of the dividend.

Our Thoughts On Yusin Holding's Dividend

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. This company is not in the top tier of income providing stocks.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Just as an example, we've come across 2 warning signs for Yusin Holding you should be aware of, and 1 of them is potentially serious. Is Yusin Holding not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:4557

Yusin Holding

An investment holding company, manufactures and sells vehicle’s brake systems in Asia, North America, Central and South America, Europe, and internationally.

Adequate balance sheet second-rate dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Automotive Electronics Manufacturer Consistent and Stable

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion