Advertisement

- Taiwan

- /

- Auto Components

- /

- TWSE:2105

Take Care Before Diving Into The Deep End On Cheng Shin Rubber Ind. Co., Ltd. (TWSE:2105)

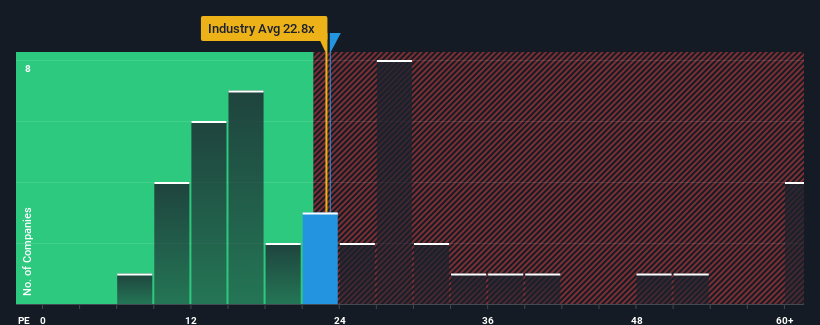

It's not a stretch to say that Cheng Shin Rubber Ind. Co., Ltd.'s (TWSE:2105) price-to-earnings (or "P/E") ratio of 23.2x right now seems quite "middle-of-the-road" compared to the market in Taiwan, where the median P/E ratio is around 22x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Cheng Shin Rubber Ind certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to deteriorate like the rest, which has kept the P/E from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

See our latest analysis for Cheng Shin Rubber Ind

Does Growth Match The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Cheng Shin Rubber Ind's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 33% last year. The strong recent performance means it was also able to grow EPS by 102% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next year should generate growth of 27% as estimated by the four analysts watching the company. That's shaping up to be materially higher than the 22% growth forecast for the broader market.

In light of this, it's curious that Cheng Shin Rubber Ind's P/E sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Cheng Shin Rubber Ind's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Having said that, be aware Cheng Shin Rubber Ind is showing 1 warning sign in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on Cheng Shin Rubber Ind, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2105

Cheng Shin Rubber Ind

Together with subsidiaries, processes, manufactures, and trades in bicycle and electrical vehicle tires, reclaimed rubbers, rubbers and resins, and other rubber products.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor