Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Hwa Fong Rubber Ind. Co., Ltd. (TPE:2109) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Hwa Fong Rubber Ind

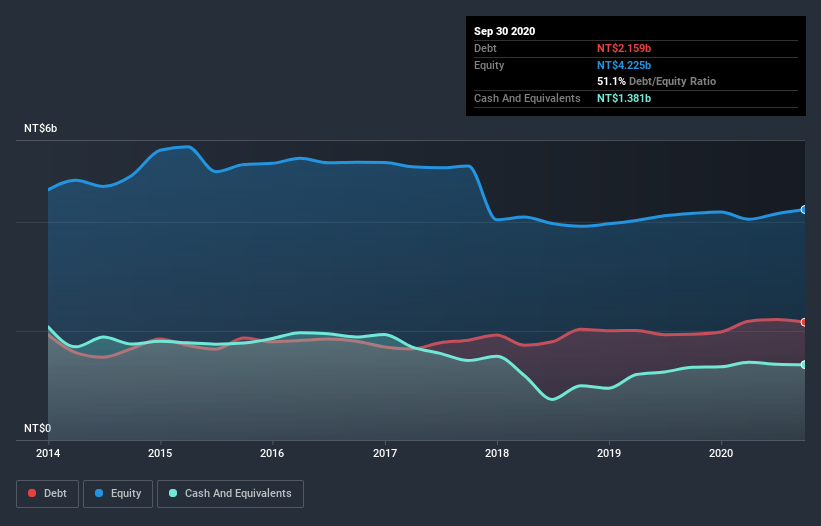

What Is Hwa Fong Rubber Ind's Net Debt?

As you can see below, at the end of September 2020, Hwa Fong Rubber Ind had NT$2.16b of debt, up from NT$1.94b a year ago. Click the image for more detail. However, it does have NT$1.38b in cash offsetting this, leading to net debt of about NT$778.1m.

A Look At Hwa Fong Rubber Ind's Liabilities

The latest balance sheet data shows that Hwa Fong Rubber Ind had liabilities of NT$1.76b due within a year, and liabilities of NT$1.57b falling due after that. On the other hand, it had cash of NT$1.38b and NT$807.1m worth of receivables due within a year. So it has liabilities totalling NT$1.14b more than its cash and near-term receivables, combined.

Hwa Fong Rubber Ind has a market capitalization of NT$4.09b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Hwa Fong Rubber Ind has a low net debt to EBITDA ratio of only 1.1. And its EBIT covers its interest expense a whopping 12.7 times over. So we're pretty relaxed about its super-conservative use of debt. On top of that, Hwa Fong Rubber Ind grew its EBIT by 89% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Hwa Fong Rubber Ind will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Hwa Fong Rubber Ind recorded negative free cash flow, in total. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

Both Hwa Fong Rubber Ind's ability to to cover its interest expense with its EBIT and its EBIT growth rate gave us comfort that it can handle its debt. In contrast, our confidence was undermined by its apparent struggle to convert EBIT to free cash flow. When we consider all the elements mentioned above, it seems to us that Hwa Fong Rubber Ind is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Like risks, for instance. Every company has them, and we've spotted 2 warning signs for Hwa Fong Rubber Ind (of which 1 makes us a bit uncomfortable!) you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade Hwa Fong Rubber Ind, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hwa Fong Rubber Industrial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TWSE:2109

Hwa Fong Rubber Industrial

Hwa Fong Rubber Industrial Co., Ltd., together with its subsidiaries, manufacture, process, sells, imports, and exports rubber and plastic products in Taiwan, China, the United States, Thailand, and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor