Advertisement

- Taiwan

- /

- Auto Components

- /

- TWSE:2105

Can Cheng Shin Rubber Ind. Co., Ltd.'s (TPE:2105) Weak Financials Pull The Plug On The Stock's Current Momentum On Its Share Price?

Cheng Shin Rubber Ind's (TPE:2105) stock is up by a considerable 14% over the past three months. However, in this article, we decided to focus on its weak fundamentals, as long-term financial performance of a business is what ultimatley dictates market outcomes. Particularly, we will be paying attention to Cheng Shin Rubber Ind's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

Check out our latest analysis for Cheng Shin Rubber Ind

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Cheng Shin Rubber Ind is:

4.3% = NT$3.3b ÷ NT$76b (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. So, this means that for every NT$1 of its shareholder's investments, the company generates a profit of NT$0.04.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Cheng Shin Rubber Ind's Earnings Growth And 4.3% ROE

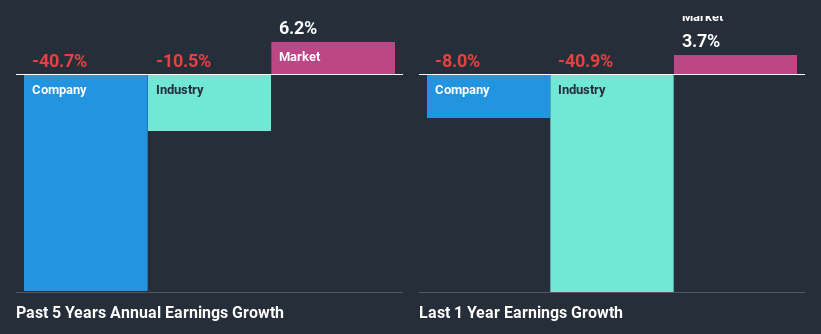

When you first look at it, Cheng Shin Rubber Ind's ROE doesn't look that attractive. However, its ROE is similar to the industry average of 5.1%, so we won't completely dismiss the company. Having said that, Cheng Shin Rubber Ind's five year net income decline rate was 41%. Bear in mind, the company does have a slightly low ROE. Hence, this goes some way in explaining the shrinking earnings.

Furthermore, even when compared to the industry, which has been shrinking its earnings at a rate 11% in the same period, we found that Cheng Shin Rubber Ind's performance is pretty disappointing, as it suggests that the company has been shrunk its earnings at a rate faster than the industry.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. Is Cheng Shin Rubber Ind fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Cheng Shin Rubber Ind Efficiently Re-investing Its Profits?

Cheng Shin Rubber Ind's very high three-year median payout ratio of 106% over the last three years suggests that the company is paying its shareholders more than what it is earning and this explains the company's shrinking earnings. Its usually very hard to sustain dividend payments that are higher than reported profits. You can see the 2 risks we have identified for Cheng Shin Rubber Ind by visiting our risks dashboard for free on our platform here.

Additionally, Cheng Shin Rubber Ind has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 83% over the next three years. Accordingly, the expected drop in the payout ratio explains the expected increase in the company's ROE to 7.8%, over the same period.

Conclusion

In total, we would have a hard think before deciding on any investment action concerning Cheng Shin Rubber Ind. The low ROE, combined with the fact that the company is paying out almost if not all, of its profits as dividends, has resulted in the lack or absence of growth in its earnings. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

When trading Cheng Shin Rubber Ind or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:2105

Cheng Shin Rubber Ind

Together with subsidiaries, processes, manufactures, and trades in bicycle and electrical vehicle tires, reclaimed rubbers, rubbers and resins, and other rubber products.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor