Advertisement

- Turkey

- /

- Electrical

- /

- IBSE:ASTOR

Undiscovered Gems with Promising Potential in October 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape of shifting economic indicators and interest rate adjustments, small-cap stocks have shown resilience, with indices like the Russell 2000 outperforming larger counterparts. In this dynamic environment, identifying promising stocks involves looking for companies that exhibit strong fundamentals and growth potential amid broader market trends.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| ITOCHU-SHOKUHIN | NA | -0.08% | 12.04% | ★★★★★★ |

| Shanghai Chlor-Alkali Chemical | 7.56% | 3.92% | 3.37% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| ASIA Holdings | 34.98% | 8.43% | 16.17% | ★★★★★☆ |

| Hongrun Construction Group | 56.74% | -11.36% | 0.79% | ★★★★★☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Sichuan Zigong Conveying Machine Group | 30.45% | 15.38% | 3.12% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

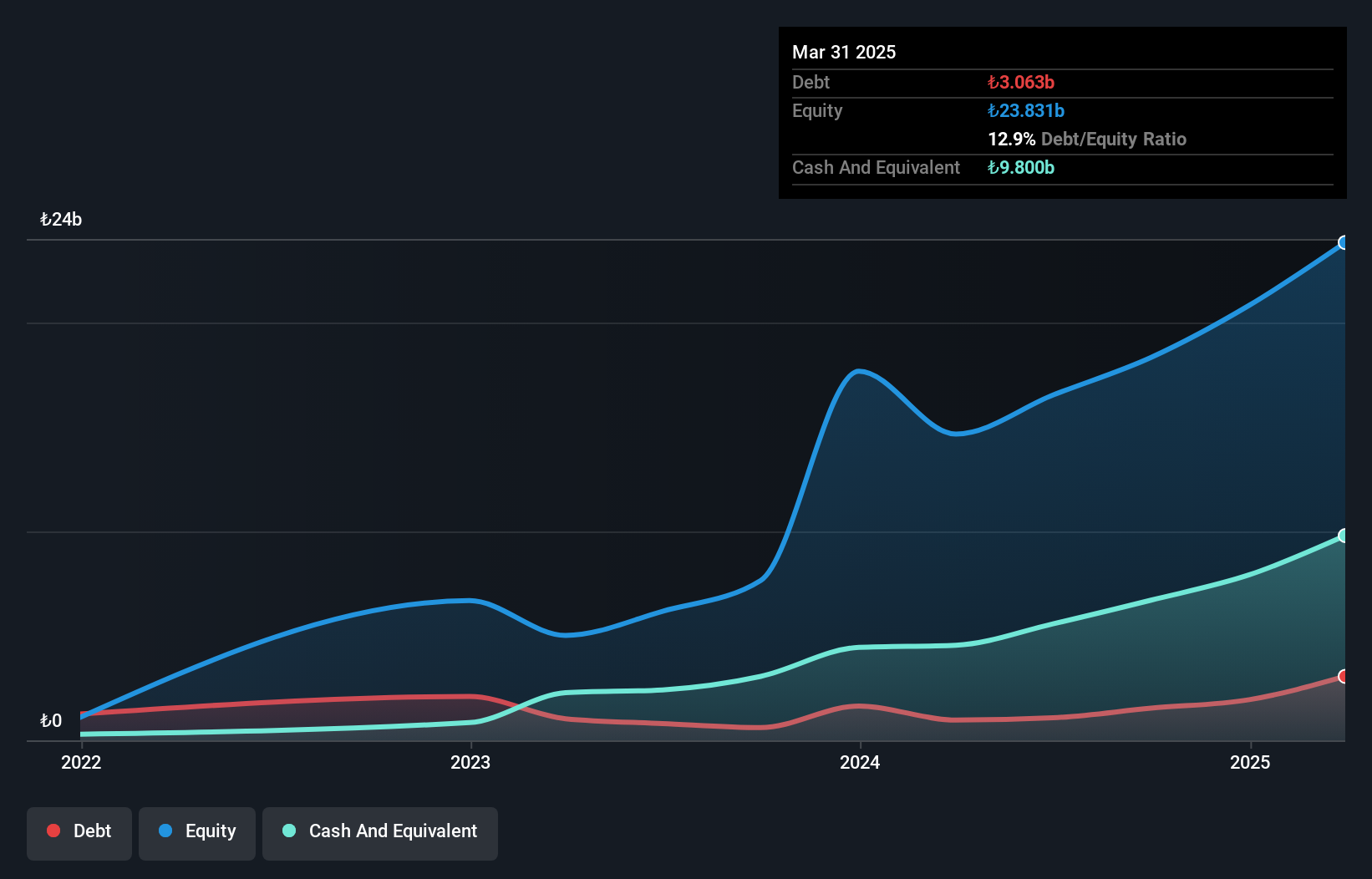

Astor Enerji (IBSE:ASTOR)

Simply Wall St Value Rating: ★★★★★☆

Overview: Astor Enerji A.S. specializes in the manufacturing and sales of transformers and switching products, with a market cap of TRY67.71 billion.

Operations: Astor Enerji generates revenue primarily from its electric equipment segment, amounting to TRY19.91 billion.

Astor Enerji, a relatively small player in the electrical industry, has demonstrated impressive growth. Over the past year, its earnings surged by 146%, outpacing the industry's -11% performance. The company reported TRY 5.16 billion in sales for Q2 2024, up from TRY 4.93 billion a year earlier, with net income increasing to TRY 661 million from TRY 572 million. Astor's price-to-earnings ratio of 13.1x is below the market average of 14.6x, suggesting good value relative to peers and industry norms while holding more cash than total debt enhances its financial stability and appeal as an investment prospect.

- Dive into the specifics of Astor Enerji here with our thorough health report.

Evaluate Astor Enerji's historical performance by accessing our past performance report.

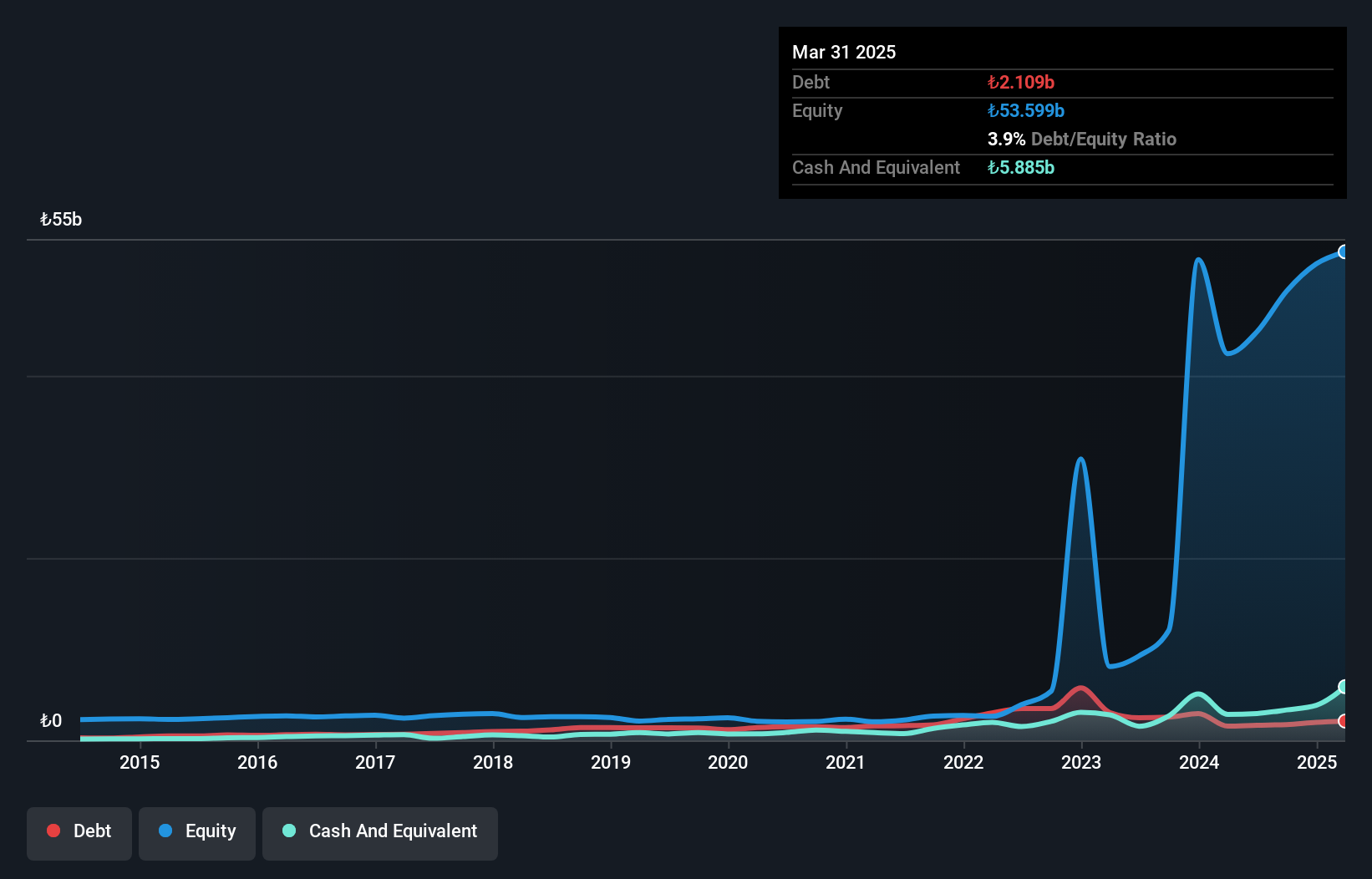

Aygaz (IBSE:AYGAZ)

Simply Wall St Value Rating: ★★★★★★

Overview: Aygaz A.S. is a company that purchases liquid petroleum gas (LPG) for distribution to retailers in Turkey, with a market cap of TRY32.97 billion.

Operations: Aygaz generates revenue primarily from LPG and natural gas sales, amounting to TRY58.03 billion, supplemented by cargo transportation and distribution services contributing TRY1.22 billion. The company's net profit margin is a key financial metric to consider when evaluating its profitability.

Aygaz, a player in the energy sector, showcases a mixed financial landscape. Despite trading at 87.2% below its estimated fair value, recent figures reveal challenges; net income for the second quarter was TRY 256.83 million compared to TRY 834.09 million last year, with basic earnings per share dropping from TRY 3.79 to TRY 1.17. Over five years, debt-to-equity improved significantly from 59.7% to just 3.7%, indicating better financial management and stability despite negative earnings growth of -28.8%. While Aygaz has more cash than total debt and generates positive free cash flow, future earnings are expected to decline by an average of 28.3% annually over the next three years.

- Get an in-depth perspective on Aygaz's performance by reading our health report here.

Gain insights into Aygaz's past trends and performance with our Past report.

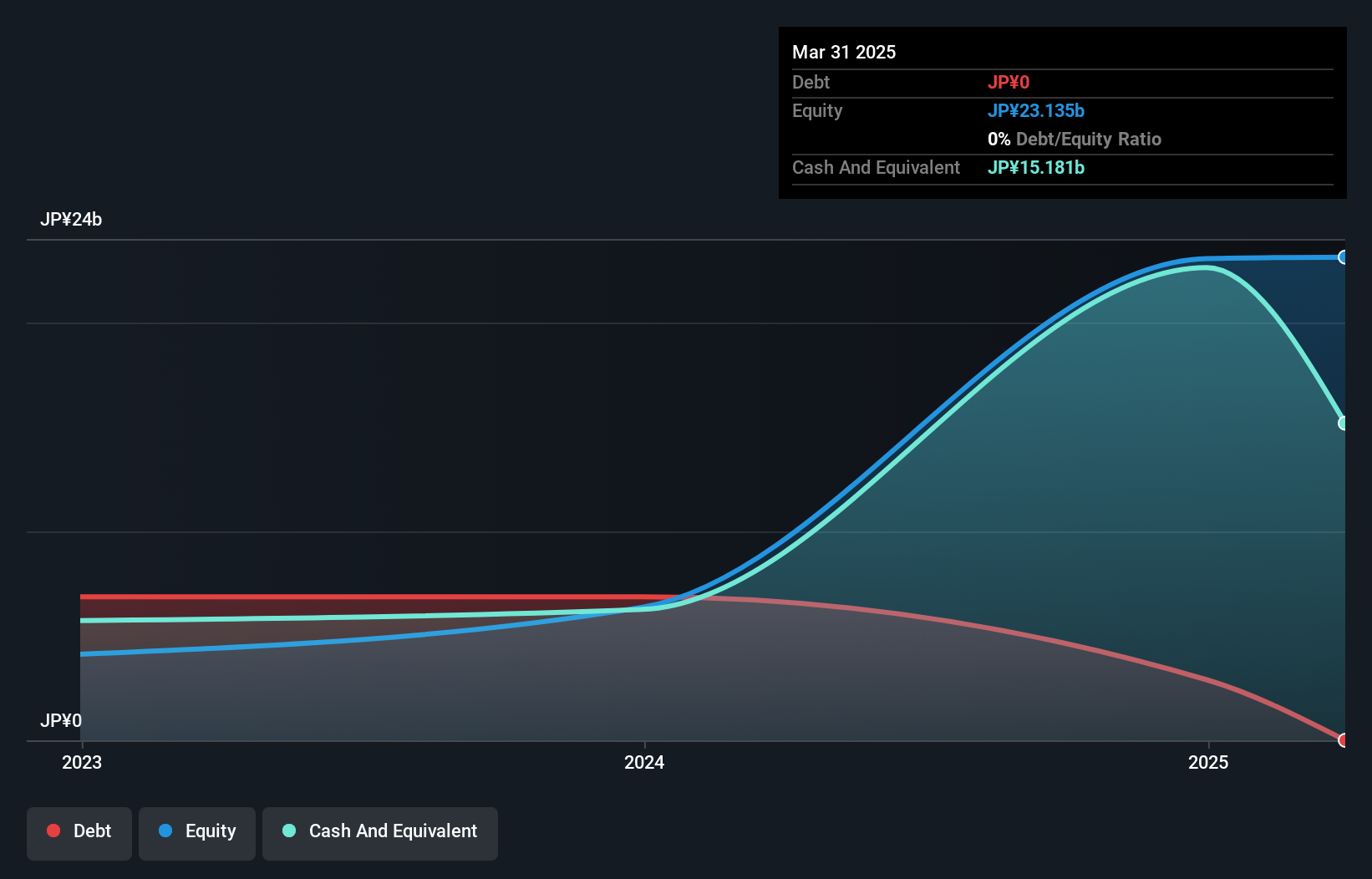

Intermestic (TSE:262A)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Intermestic Inc. operates retail and online platforms for selling eyeglasses and sunglasses in Japan, with a market cap of ¥42.43 billion.

Operations: Intermestic generates revenue primarily from its Domestic Business, contributing ¥38.17 billion, while the Overseas Segment adds ¥2.09 billion.

Intermestic's recent IPO raised ¥17.48 billion, offering 10.72 million shares at a price of ¥1630 each, with a slight discount per security. The company is trading 8.5% below its estimated fair value, highlighting potential undervaluation for investors. Over the past year, earnings surged by 102%, significantly outpacing the Specialty Retail industry average of 4.6%. With interest coverage at an impressive 112 times EBIT and a net debt to equity ratio of just 9.5%, Intermestic demonstrates solid financial health despite having less than three years of financial data available for deeper analysis.

- Click to explore a detailed breakdown of our findings in Intermestic's health report.

Assess Intermestic's past performance with our detailed historical performance reports.

Make It Happen

- Click here to access our complete index of 4788 Undiscovered Gems With Strong Fundamentals.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IBSE:ASTOR

Astor Enerji

Engages in the manufacturing of transformers, and medium and high voltage switching products for industrial facilities.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.7% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|18.7% undervalued

GM

Community Contributor