Why It Might Not Make Sense To Buy Singapore Press Holdings Limited (SGX:T39) For Its Upcoming Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Singapore Press Holdings Limited (SGX:T39) is about to go ex-dividend in just 3 days. If you purchase the stock on or after the 5th of May, you won't be eligible to receive this dividend, when it is paid on the 22nd of May.

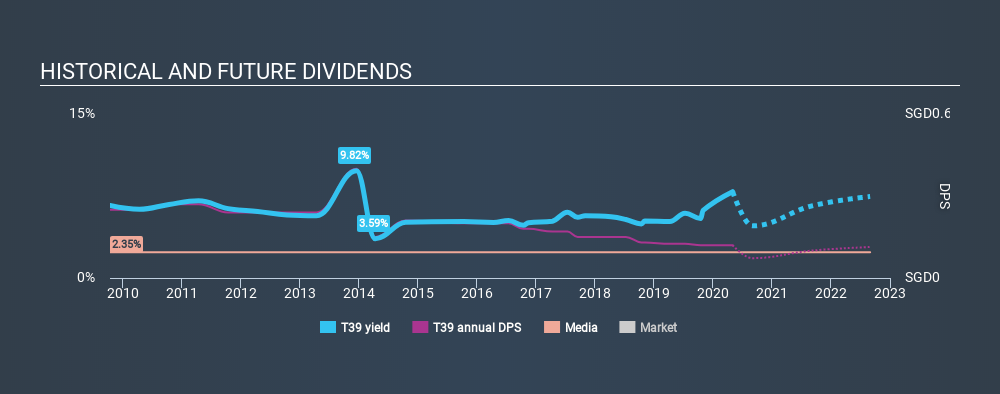

Singapore Press Holdings's next dividend payment will be S$0.015 per share, on the back of last year when the company paid a total of S$0.12 to shareholders. Based on the last year's worth of payments, Singapore Press Holdings stock has a trailing yield of around 7.9% on the current share price of SGD1.52. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

View our latest analysis for Singapore Press Holdings

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Singapore Press Holdings paid out 59% of its earnings to investors last year, a normal payout level for most businesses. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Singapore Press Holdings paid out more free cash flow than it generated - 133%, to be precise - last year, which we think is concerningly high. It's hard to consistently pay out more cash than you generate without either borrowing or using company cash, so we'd wonder how the company justifies this payout level.

Singapore Press Holdings paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough cash to cover the dividend. Cash is king, as they say, and were Singapore Press Holdings to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings fall far enough, the company could be forced to cut its dividend. Readers will understand then, why we're concerned to see Singapore Press Holdings's earnings per share have dropped 14% a year over the past five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

Singapore Press Holdings also issued more than 5% of its market cap in new stock during the past year, which we feel is likely to hurt its dividend prospects in the long run. Trying to grow the dividend while issuing large amounts of new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Singapore Press Holdings's dividend payments per share have declined at 7.1% per year on average over the past ten years, which is uninspiring. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

Final Takeaway

Should investors buy Singapore Press Holdings for the upcoming dividend? Singapore Press Holdings had an average payout ratio, but its free cash flow was lower and earnings per share have been declining. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

With that in mind though, if the poor dividend characteristics of Singapore Press Holdings don't faze you, it's worth being mindful of the risks involved with this business. Our analysis shows 5 warning signs for Singapore Press Holdings that we strongly recommend you have a look at before investing in the company.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.