Advertisement

- Singapore

- /

- Energy Services

- /

- SGX:M05

The MTQ (SGX:M05) Share Price Is Down 88% So Some Shareholders Are Rather Upset

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

While not a mind-blowing move, it is good to see that the MTQ Corporation Limited (SGX:M05) share price has gained 15% in the last three months. But will that repair the damage for the weary investors who have owned this stock as it declined over half a decade? Probably not. Like a ship taking on water, the share price has sunk 88% in that time. While the recent increase might be a green shoot, we're certainly hesitant to rejoice. The important question is if the business itself justifies a higher share price in the long term.

While a drop like that is definitely a body blow, money isn't as important as health and happiness.

See our latest analysis for MTQ

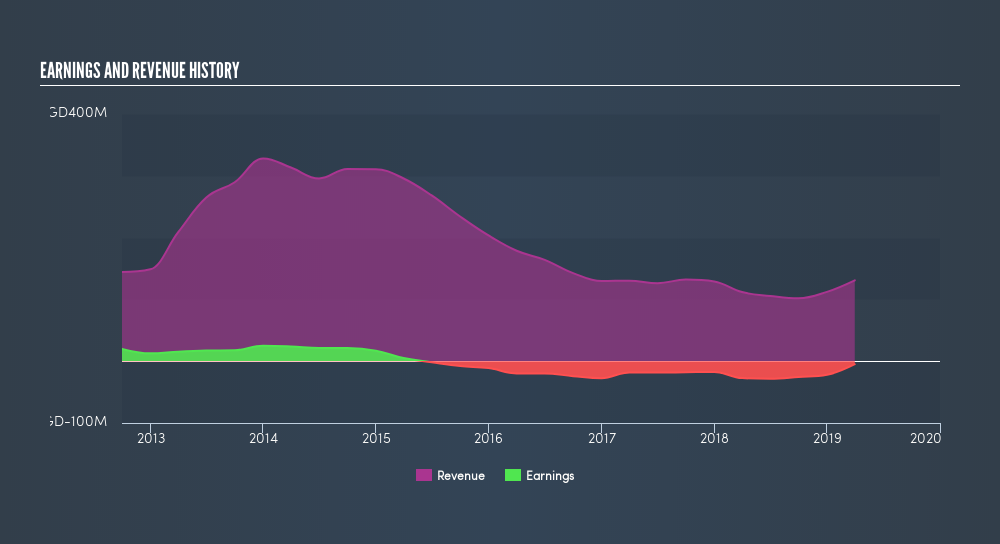

Because MTQ is loss-making, we think the market is probably more focussed on revenue and revenue growth, at least for now. When a company doesn't make profits, we'd generally expect to see good revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

In the last five years MTQ saw its revenue shrink by 25% per year. That's definitely a weaker result than most pre-profit companies report. So it's not altogether surprising to see the share price down 35% per year in the same time period. We don't think this is a particularly promising picture. Ironically, that behavior could create an opportunity for the contrarian investor - but only if there are good reasons to predict a brighter future.

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

What about the Total Shareholder Return (TSR)?

Investors should note that there's a difference between MTQ's total shareholder return (TSR) and its share price change, which we've covered above. The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Dividends have been really beneficial for MTQ shareholders, and that cash payout explains why its total shareholder loss of 86%, over the last 5 years, isn't as bad as the share price return.

A Different Perspective

We're pleased to report that MTQ shareholders have received a total shareholder return of 7.9% over one year. There's no doubt those recent returns are much better than the TSR loss of 33% per year over five years. The long term loss makes us cautious, but the short term TSR gain certainly hints at a brighter future. Shareholders might want to examine this detailed historical graph of past earnings, revenue and cash flow.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on SG exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SGX:M05

MTQ

Provides engineering solutions for oilfield equipment in Singapore, the Kingdom of Bahrain, Australia, United Arab Emirates, and the United Kingdom.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor