Advertisement

- Singapore

- /

- Energy Services

- /

- SGX:BTP

Baker Technology (SGX:BTP) Has Debt But No Earnings; Should You Worry?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Baker Technology Limited (SGX:BTP) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Baker Technology

What Is Baker Technology's Net Debt?

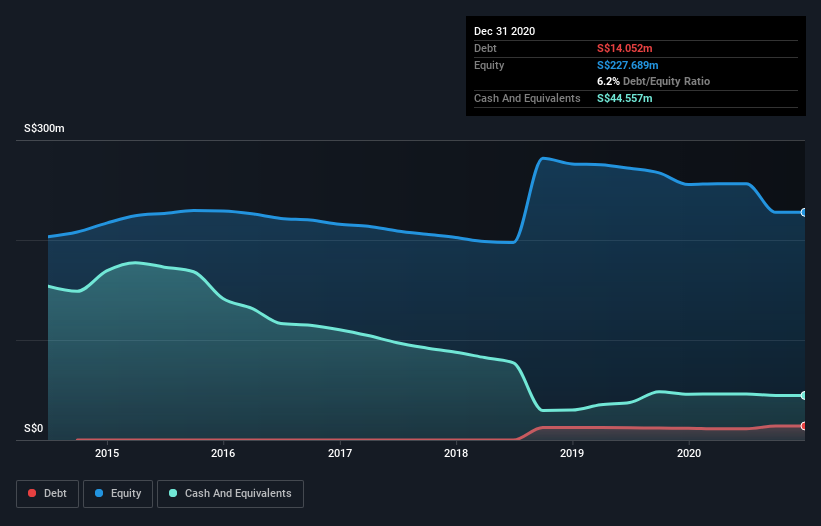

The image below, which you can click on for greater detail, shows that at December 2020 Baker Technology had debt of S$14.1m, up from S$11.8m in one year. But it also has S$44.6m in cash to offset that, meaning it has S$30.5m net cash.

How Strong Is Baker Technology's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Baker Technology had liabilities of S$22.3m due within 12 months and liabilities of S$13.5m due beyond that. Offsetting this, it had S$44.6m in cash and S$26.2m in receivables that were due within 12 months. So it actually has S$34.9m more liquid assets than total liabilities.

This excess liquidity is a great indication that Baker Technology's balance sheet is almost as strong as Fort Knox. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Succinctly put, Baker Technology boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is Baker Technology's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Baker Technology had a loss before interest and tax, and actually shrunk its revenue by 2.0%, to S$63m. We would much prefer see growth.

So How Risky Is Baker Technology?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year Baker Technology had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through S$4.0m of cash and made a loss of S$14m. Given it only has net cash of S$30.5m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Baker Technology (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you decide to trade Baker Technology, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Baker Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SGX:BTP

Baker Technology

An investment holding company, provides specialized marine offshore equipment and services for the oil and gas industry in the Asia Pacific, Africa, Europe, Singapore, the Middle East, the Americas, and China.

Excellent balance sheet unattractive dividend payer.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor