Advertisement

Despite Its High P/E Ratio, Is Fu Yu Corporation Limited (SGX:F13) Still Undervalued?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

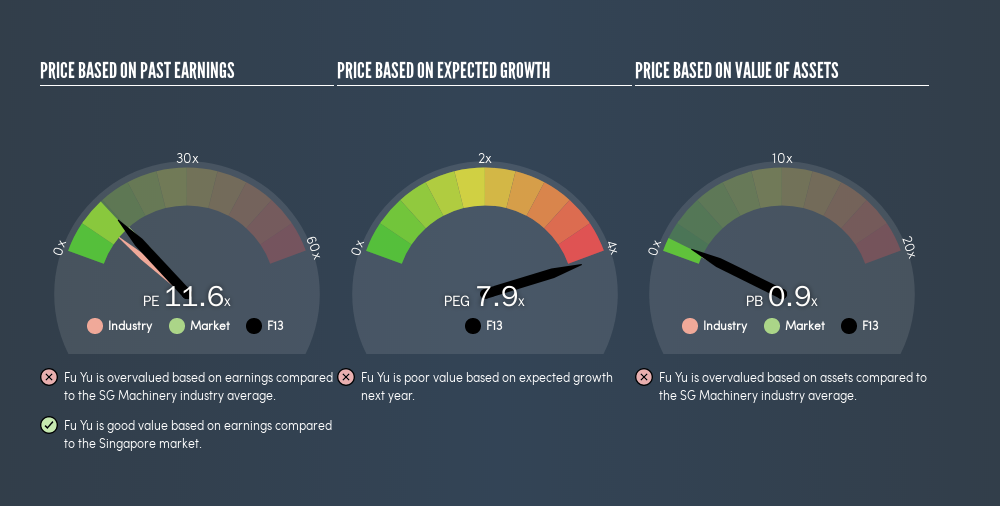

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). We'll show how you can use Fu Yu Corporation Limited's (SGX:F13) P/E ratio to inform your assessment of the investment opportunity. What is Fu Yu's P/E ratio? Well, based on the last twelve months it is 11.59. That corresponds to an earnings yield of approximately 8.6%.

See our latest analysis for Fu Yu

How Do You Calculate A P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Fu Yu:

P/E of 11.59 = SGD0.20 ÷ SGD0.017 (Based on the trailing twelve months to March 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that buyers have to pay a higher price for each SGD1 the company has earned over the last year. All else being equal, it's better to pay a low price -- but as Warren Buffett said, 'It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.'

How Growth Rates Impact P/E Ratios

Earnings growth rates have a big influence on P/E ratios. When earnings grow, the 'E' increases, over time. That means unless the share price increases, the P/E will reduce in a few years. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

In the last year, Fu Yu grew EPS like Taylor Swift grew her fan base back in 2010; the 188% gain was both fast and well deserved. The sweetener is that the annual five year growth rate of 25% is also impressive. With that kind of growth rate we would generally expect a high P/E ratio.

How Does Fu Yu's P/E Ratio Compare To Its Peers?

We can get an indication of market expectations by looking at the P/E ratio. You can see in the image below that the average P/E (8.5) for companies in the machinery industry is lower than Fu Yu's P/E.

That means that the market expects Fu Yu will outperform other companies in its industry. Clearly the market expects growth, but it isn't guaranteed. So investors should delve deeper. I like to check if company insiders have been buying or selling.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

The 'Price' in P/E reflects the market capitalization of the company. Thus, the metric does not reflect cash or debt held by the company. Theoretically, a business can improve its earnings (and produce a lower P/E in the future) by investing in growth. That means taking on debt (or spending its cash).

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

How Does Fu Yu's Debt Impact Its P/E Ratio?

Fu Yu has net cash of S$75m. This is fairly high at 50% of its market capitalization. That might mean balance sheet strength is important to the business, but should also help push the P/E a bit higher than it would otherwise be.

The Verdict On Fu Yu's P/E Ratio

Fu Yu trades on a P/E ratio of 11.6, which is fairly close to the SG market average of 12.3. Its net cash position is the cherry on top of its superb EPS growth. So based on this analysis we'd expect Fu Yu to have a higher P/E ratio.

Investors have an opportunity when market expectations about a stock are wrong. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine.' So this free report on the analyst consensus forecasts could help you make a master move on this stock.

You might be able to find a better buy than Fu Yu. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SGX:F13

Fu Yu

An investment holding company, engages in the manufacture and sub-assembly of precision plastic parts and components in Singapore, Malaysia, and China.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$245.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RA

RacerBVN on iShares Trust - iShares Preferred and Income Securities ETF ·

This one is all about the tax benefits

Fair Value:US$54.5543.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FatPie on SoFi Technologies ·

Estimated Share Price is $79.54 using the Buffett Value Calculation

Fair Value:US$79.5465.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3925.9% undervalued

961 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative