Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies AusGroup Limited (SGX:5GJ) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out the opportunities and risks within the SG Construction industry.

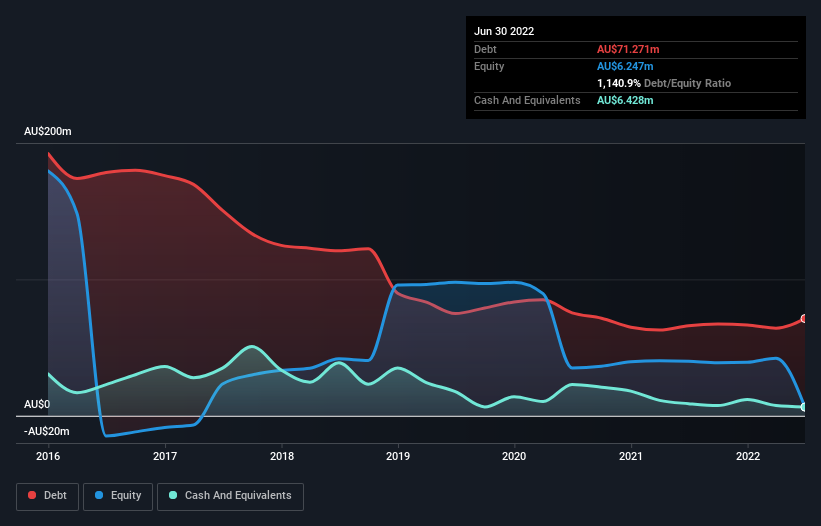

How Much Debt Does AusGroup Carry?

As you can see below, at the end of June 2022, AusGroup had AU$71.3m of debt, up from AU$66.0m a year ago. Click the image for more detail. However, it does have AU$6.43m in cash offsetting this, leading to net debt of about AU$64.8m.

A Look At AusGroup's Liabilities

We can see from the most recent balance sheet that AusGroup had liabilities of AU$94.1m falling due within a year, and liabilities of AU$38.2m due beyond that. Offsetting these obligations, it had cash of AU$6.43m as well as receivables valued at AU$56.1m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by AU$69.7m.

The deficiency here weighs heavily on the AU$34.0m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, AusGroup would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But it is AusGroup's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year AusGroup wasn't profitable at an EBIT level, but managed to grow its revenue by 26%, to AU$245m. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

While we can certainly appreciate AusGroup's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. Its EBIT loss was a whopping AU$15m. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. For example, we would not want to see a repeat of last year's loss of AU$32m. In the meantime, we consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for AusGroup you should be aware of, and 1 of them is a bit unpleasant.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:5GJ

AusGroup

AusGroup Limited, an investment holding company, engages in the provision of integrated service solutions to the energy, resources, industrial, utilities, and port and marine sectors in Australia and Southeast Asia.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor