Advertisement

How UOB's Surge in Credit Provisions Will Impact United Overseas Bank (SGX:U11) Investors

Simply Wall St

Reviewed by Sasha Jovanovic

- In the past week, United Overseas Bank (UOB) reported a 72% decline in third-quarter net profit, primarily due to S$615 million in increased credit provisions set aside to address potential credit risks amid a volatile global economic environment.

- Despite this significant profit decline, management emphasized that these proactive provisions are not a sign of core business weakness and reaffirmed their commitment to maintaining the 2025 final dividend, highlighting confidence in the bank’s capital strength.

- We'll explore how UOB's substantial increase in credit provisions may influence the company's investment narrative and future financial outlook.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

United Overseas Bank Investment Narrative Recap

For investors in United Overseas Bank, the core belief centers on the group's ability to balance growth opportunities in ASEAN with disciplined risk management, even amid rising global volatility. The recent earnings setback, driven by a sharp increase in credit provisions, intensifies focus on UOB’s net interest margin and fee income trajectory, which now face short-term headwinds amid persistent margin pressures. While these provisions do not materially alter UOB’s biggest catalyst, fee income growth, and main risk, margin compression, the situation merits close monitoring.

Among recent announcements, the appointment of UOB as joint lead manager for Wee Hur Holdings' Series 001 Notes highlights the bank’s ongoing engagement in fee-based capital markets activities. This remains relevant in the context of UOB’s outlook for high single- to double-digit fee income growth, which management positions as a key lever to offset stress on lending margins and support short-term business momentum.

Yet, in contrast to management’s reassurance about business stability, investors should be aware of the potential for prolonged net interest margin compression to …

Read the full narrative on United Overseas Bank (it's free!)

United Overseas Bank's narrative projects SGD16.0 billion revenue and SGD6.7 billion earnings by 2028. This requires 6.2% yearly revenue growth and a SGD0.8 billion earnings increase from the current earnings of SGD5.9 billion.

Uncover how United Overseas Bank's forecasts yield a SGD37.66 fair value, a 11% upside to its current price.

Exploring Other Perspectives

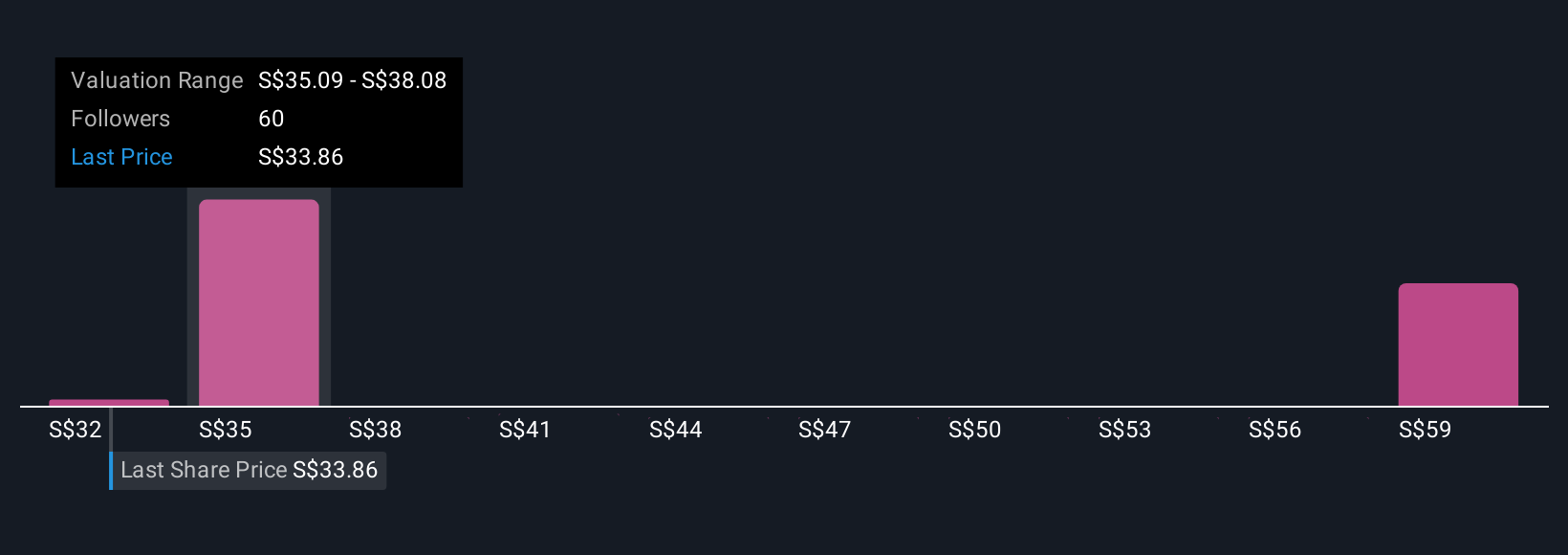

Simply Wall St Community members shared 10 fair value estimates for UOB, ranging from S$32.09 to S$62.06 per share. While views differ, many are watching how ongoing net interest margin pressures might influence future profit growth and capital returns.

Explore 10 other fair value estimates on United Overseas Bank - why the stock might be worth as much as 83% more than the current price!

Build Your Own United Overseas Bank Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your United Overseas Bank research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free United Overseas Bank research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate United Overseas Bank's overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:U11

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor