Advertisement

We Think Vertiseit AB (publ)'s (STO:VERT B) CEO Compensation Looks Fair

Key Insights

- Vertiseit's Annual General Meeting to take place on 2nd of May

- Salary of kr1.29m is part of CEO Johan Lind's total remuneration

- The overall pay is comparable to the industry average

- Vertiseit's total shareholder return over the past three years was 81% while its EPS grew by 40% over the past three years

The performance at Vertiseit AB (publ) (STO:VERT B) has been quite strong recently and CEO Johan Lind has played a role in it. Coming up to the next AGM on 2nd of May, shareholders would be keeping this in mind. It is likely that the focus will be on company strategy going forward as shareholders hear from the board and cast their votes on resolutions such as executive remuneration and other matters. In light of the great performance, we discuss the case why we think CEO compensation is not excessive.

See our latest analysis for Vertiseit

Comparing Vertiseit AB (publ)'s CEO Compensation With The Industry

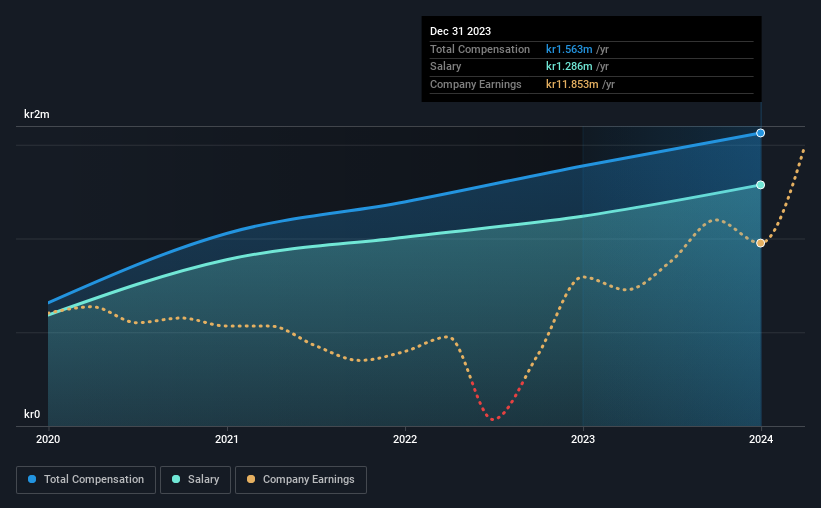

Our data indicates that Vertiseit AB (publ) has a market capitalization of kr851m, and total annual CEO compensation was reported as kr1.6m for the year to December 2023. Notably, that's an increase of 13% over the year before. We note that the salary portion, which stands at kr1.29m constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the Swedish IT industry with market capitalizations under kr2.2b, the reported median total CEO compensation was kr2.1m. So it looks like Vertiseit compensates Johan Lind in line with the median for the industry. What's more, Johan Lind holds kr91m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | kr1.3m | kr1.1m | 82% |

| Other | kr277k | kr268k | 18% |

| Total Compensation | kr1.6m | kr1.4m | 100% |

On an industry level, around 64% of total compensation represents salary and 36% is other remuneration. Vertiseit is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Vertiseit AB (publ)'s Growth Numbers

Vertiseit AB (publ) has seen its earnings per share (EPS) increase by 40% a year over the past three years. It achieved revenue growth of 5.9% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Vertiseit AB (publ) Been A Good Investment?

We think that the total shareholder return of 81%, over three years, would leave most Vertiseit AB (publ) shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Given the company's decent performance, the CEO remuneration policy might not be shareholders' central point of focus in the AGM. However, investors will get the chance to engage on key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 2 warning signs for Vertiseit that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:VERT B

Vertiseit

A retail tech company, operates digital in-store platform in Europe.

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor